It fascinates me how bear markets all feel alike in some ways. What I remember very clearly from the equity bear markets of 2000-2002 and 2007-2009 is that bulls wanted to bottom-tick the market at every imagined opportunity. Every "support level," for the first half of each decline at least, saw bulls pile in as if the train were about to leave the station without them on it. Of course, the train was about to leave the station, but it was backing up.

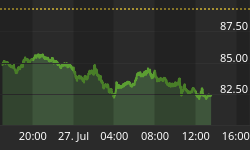

Today, the S&P didn't quite touch 1810 on the downside, basically matching the 1812 low from January. Bulls love double-bottoms. Of course, many of those turn out not to be double-bottoms after all, but the ones that are look very nice on the charts. So stocks rocketed off the lows, rising 25 S&P points in a matter of minutes after briefly being down 51. The rally was helped ostensibly by comments from the UAE oil minister, who claimed OPEC is ready to cooperate on a production cut. But that isn't really why stocks rallied so dramatically; after all the news only pushed crude oil itself up about a buck. The real reason is that bulls are crazy maniacs.

They're that way for a reason. If you are benchmarked against an equity index, it is very hard for an unlevered fund manager to beat that index in an up market. Once you subtract fees, and a drag from whatever cash holding you must have, you're doing well to match the index since your limitation is (by definition of 'unlevered') 100% long.[1] Where a fund manager must beat his index is in a down market, by participating less than 100% in a selloff. But being an outperformer in a down market is less valuable since customer outflows are likely to outweigh the inflows if there is a serious bear market. Therefore, fund managers naturally fall into a pattern of scalping small selloffs for outperformance. But since they can't really afford to miss being long in a bull market, there is a serious tendency to dive back in at any hint that the decline may be over.

So we get these entertaining, furious bear market rallies, which tend not to last very long. Of course, my entire premise is that this is an equity bear market, and I could be completely wrong on that. If I am, then ignore the prior paragraphs.

Where I am more confident that I am right is on the monetary policy side. Get this: since the Fed hiked rates, year-over-year M2 money growth has gone from 5.7% to...5.7%. Lest you think this anomaly (because tightening is supposed to involve a deceleration in money growth, right?!?), the 26-week growth rate in M2 has gone from 5.3% to 6.8%, and the 13-week growth rate from 2.9% to 7.3%. The annualized growth rate of M2 from mid-December to February 1st (the figure that was released today) is 11.2%. In other words, money supply growth is clearly not decelerating.

Now, in a traditional tightening, the Fed would restrict reserves and this would have the effect of reducing, or at least causing a deceleration in the growth rate of, M2 through the money multiplier. As a side effect, interest rates would rise but the point of tightening is to reduce the growth rate of money. Or, at least, it used to be.

With the Fed's current operating framework, in which interest rates are moved around like magnets on a refrigerator to the desired level, there should be no meaningful effect on money supply growth. That's not to say that money growth rates should accelerate (as they evidently have), merely that the growth rates should be stochastic with respect to authoritarian interest-rate manipulation. They may fall, or they may rise, but it should not be related to the Fed's "tightening." I've been saying this for a long, long time and the first evidence is in. The Fed's rate hike has done nothing to reduce the growth rate of money, and therefore ought to do nothing to restrain inflation. Indeed, if higher interest rates follow from a series of Fed hikes - which they haven't, but mainly because no one believes the Fed is going to hike again while their precious stocks are only 35% above fair value rather than 50% - then the expected effect would be for monetary velocity to rise and inflation to accelerate.

At this point, the Fed can thank the market that their moves haven't accelerated the already-established trend towards higher inflation. But the clock is ticking. If the Fed does indeed hike rates next month, the bond market may start taking it seriously and start the rates-inflation spiral.

[1] Unless, of course, you're adding alpha. But the universe of fund managers adds approximately zero alpha - slightly positive, and negative net of fees. Except whoever your manager is, of course. I'm sure he's the best. Good job finding him!

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"