On the week, the prices of the metals didn't move all that much. However, the move around 6am (Arizona time) on Thursday is notable. The price of silver spiked up from around $15.12 to $15.64 -- 3.4% -- by around 8am. Twelve hours later, the price touched $15.73 before sliding off. We are always interested in the fundamentals, as we watch price moves. The question is always: is this speculators, betting with leverage on the silver price using futures? Or is it industrial or stacker demand for real metal?

One coincidence that may suggest the answer to the question for Thursday's move is that the euro began a move of its own at the same time. From a low of $1.082, the euro hit $1.122 around four hours later -- 3.7%.

During the same exact time of this move in the euro, S&P futures had a large move of their own. First, the index fell from 2009 to 1968, a drop of 2%. By the end of Friday, it had surged to 2022 -- 2.7%.

Also at the same time on Thursday, crude oil futures (West Texas Intermediate) dropped 3.3%. Then over the rest of the day, it ran up 4.4%.

Of course, this is just the collateral damage from ECB President Mario Draghi's announcement. He promised an even deeper negative deposit rate plus an increase in the quantitative easing program. He also hinted that further interest rate cuts may not be forthcoming (we don't believe that Draghi, or Yellen for that matter, has ended or can end the megatrend of falling interest). Draghi actually felt obliged to say, "We have shown we are not short on ammunition."

What a confidence-squandering announcement from the central bank. Perhaps it precipitated a lack of confidence in paper currency? And perhaps that in turn caused silver monetary reservation demand to swell?

Maybe. Read on for the only true picture of the gold and silver supply and demand fundamentals...

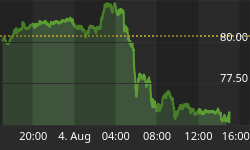

But first, here's the graph of the metals' prices.

The Prices of Gold and Silver

We are interested in the changing equilibrium created when some market participants are accumulating hoards and others are dishoarding. Of course, what makes it exciting is that speculators can (temporarily) exaggerate or fight against the trend. The speculators are often acting on rumors, technical analysis, or partial data about flows into or out of one corner of the market. That kind of information can't tell them whether the globe, on net, is hoarding or dishoarding.

One could point out that gold does not, on net, go into or out of anything. Yes, that is true. But it can come out of hoards and into carry trades. That is what we study. The gold basis tells us about this dynamic.

Conventional techniques for analyzing supply and demand are inapplicable to gold and silver, because the monetary metals have such high inventories. In normal commodities, inventories divided by annual production (stocks to flows) can be measured in months. The world just does not keep much inventory in wheat or oil.

With gold and silver, stocks to flows is measured in decades. Every ounce of those massive stockpiles is potential supply. Everyone on the planet is potential demand. At the right price, and under the right conditions. Looking at incremental changes in mine output or electronic manufacturing is not helpful to predict the future prices of the metals. For an introduction and guide to our concepts and theory, click here.

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio was down.

The Ratio of the Gold Price to the Silver Price

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

The green line is the price of the dollar, measured in gold terms (i.e. the inverse of the price of gold). As it falls (i.e. the gold price rises) gold becomes less scarce. The red line is the gold basis, our measure of scarcity of the metal. From last week:

Gold is becoming less scarce as its price is rising.

It's almost eerie how well the gold scarcity tracks the dollar price, as they both descend. Almost as if there was a connection. Or something. ;)

Our calculated fundamental price of gold fell a few bucks, but it's still well over $1,400.

Now let's look at silver.

The Silver Basis and Cobasis and the Dollar Price

Silver did firm up a bit, as the cobasis ended the week where it was last Thursday but the market price is a fair bit higher.

That said, we still read the big price move as speculation. Our fundamental price is up 55 cents from last week, but that still puts it more than 80 cents below the current market price (an improvement, as the market price was $1.40 above).

The gold-silver ratio moved down a bit this week. This fits with our comments these last few weeks:

...we suspect some of these speculators are precious metals fans, who feel that an 80:1 gold-silver ratio is excessive. It's just about touched the 2008 high (but nowhere near the level hit in 1991). Is time for the ratio to reverse and move back towards the low set in 2011?

Obviously, one can play this in the futures market with leverage. One can also express a preference for silver at a coin shop, buying silver instead of gold. Can any readers confirm that coin dealers are recommending silver as the "obvious" better buy at this ratio of over 80:1?

Monetary Metals will be in Hong for Mines and Money, and in Singapore for Mining Investment Asia. If you will be in town for either conference, and would like to meet, please drop us a line.