So I see today that former Fed Chairman Alan Greenspan says this is the worst crisis he has seen. Bigger than the 1987 Crash? Bigger than Long Term Capital? Bigger than the internet bubble collapse? Bigger than the Lehman (et. al.) collapse? Really?

As humans, we tend to have short memories and (ridiculously) short planning horizons. Greenspan, especially in his apparent dotage, has a shorter memory even than he had previously - maybe this is convenient given his record. I don't want to comment on his planning horizon as that would seem uncharitable.

Why is Brexit bad? The trade arrangements and treaties do not suddenly become invalid simply because the UK has voted to throw off the shackles of her overlords and return to being governed by the same rules they've been governed by basically since the Magna Carta. But Jim Bianco crystallized the issue for me this week. He pointed out that while Brussels could let this be a mostly painless transition, it has every incentive to make it as painful as possible. In Jim's words, "if it isn't painful then hands shoot up all over Europe to be the next to leave." That's an astute political observation, and I think he's right. The EU will work hard to punish Britain for having the temerity to demand sovereignty.

But Britain survived the Blitz; they will survive Brexit.

Indeed, Britain will survive longer than the Euro. The sun is beginning to set on that experiment. The first cracks happened a few years ago with Greece, but the implausibility of a union of political and economic interests when the national interests diverge was a problem from the first Maastricht vote. Who is next? Will it be Greece, Spain, Italy, or maybe France where the anti-EU sentiment is higher even than it is in the UK? The only questions now are the timing of the exits (is it months, or years?) and the order of the exits.

As I said, as humans we not only have short memories but short planning horizons. From a horizon of 5 or 10 years, is it going to turn out that Brexit was a total disaster, leading to a drastically different standard of living in the UK? I can't imagine that is the case - the 2008 crisis has had an effect on lifestyles, but only because of the scale and scope of central bank policy errors. In Iceland, which addressed the imbalances head-on, life recovered surprisingly quickly.

These are all political questions. The financial questions are in some sense more fascinating, and moreover feed our tendency to focus on the short term.

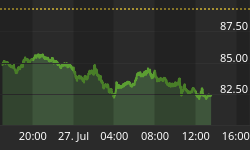

A lot of money was wagered over the last few weeks on what was a 52-48 proposition the whole way. The betting markets were skewed because of assumptions about how undecideds would break, but it was never far from a tossup in actual polling (and now perhaps we will return to taking polling with the grain of salt it is usually served with). Markets are reacting modestly violently today - at this writing, the US stock market is only -2.5% or so, which is hardly a calamity, but bourses in Europe are in considerably worse shape of course - and this should maybe be surprising with a 52-48 outcome. I like to use the Kelly Criterion framework as a useful way to think about how much to tilt investments given a particular set of circumstances.

Kelly says that your bet size should depend on your edge (the chance of winning) and your odds (the payoff, given success or failure). Going into this vote, betting on Remain had a narrow edge (52-48) and awful odds (if Remain won, the payoff was pretty small since it was mostly priced in). Kelly would say this means you should have a very small bet on, if you want to bet that outcome. If you want to bet the Leave outcome, your edge was negative but your odds were much better, so perhaps somewhat larger of a bet on Brexit than on Bremain was warranted. But that's not the way the money flowed, evidently.

Not to worry: this morning Janet Yellen said (with the market down 2.5%) that the Fed stood ready to add liquidity if needed. After 2.5%? In 1995 she would have had to come out and say that every week or two. A 2.5% decline takes us back to last week's lows. Oh, the humanity!

Just stop. The purpose of markets is to move risk from people who have it to people who want it. If, all of a sudden, lots of people seem to have too much risk and to want less, then perhaps it is because they were encouraged into taking too much risk, or encouraged to think of the risk as being less than it was. I wonder how that happened? Oh, right: that's what the Fed called the "portfolio balance channel" - by removing less-risky assets, they forced investors to hold more-risky assets since those assets now constitute a larger portion of the float. In my opinion (and this will not happen soon), central banks might consider letting markets allocate risk between the people who want it and the people who don't want it, at fair prices. Just a suggestion.

One final point to be made today. I have seen people draw comparisons between this episode and other historical episodes. This is refreshing, since it reflects at least some thoughtful attempt to remember history. Not all of these are apt or useful comparisons; I saw one that this is the "Archduke Ferdinand" moment of this generation and that's just nuts. Europe is not a military powderkeg at the moment and war in Europe is not about to begin. But, to the extent that trade barriers begin to rise again, the idea that this may be a "Smoot-Hawley" moment is worth consideration. The Smoot-Hawley tariff is generally thought to have added the "Great" to the phrase "Great Depression." I think that's probably overstating the importance of this event - especially if everybody decides to respect Britons' decision and try to continue trade as usual - but it's the right idea. What I want to point out is that while rising tariffs tend to produce lower growth and lower potential growth, they also tend to produce higher inflation. The fall of the Berlin Wall and the opening of Eastern Europe is one big reason that inflation outcomes over the last few decades have been lower than we would have expected for the amount of money growth we have had. The US has gone from producing all of its own apparel to producing almost none, for example, and this is a disinflationary influence. What would happen to apparel prices if the US changed its mind and started producing it all domestically again? Give that some thought, and realize that's the protectionist part of the Brexit argument.

We can cheer for a victory for independence and freedom, while continuing to fight against any tendency towards economic isolationism. But I worry about the latter. It will mean higher inflation going forward, even if the doomsayers are right and we also get lower growth from Brexit and the knock-on effects of Brexit.

P.S. Don't forget to buy my book! What's Wrong with Money: The Biggest Bubble of All. Thanks!

You can follow me @inflation_guy!

Enduring Investments is a registered investment adviser that specializes in solving inflation-related problems. Fill out the contact form at http://www.EnduringInvestments.com/contact and we will send you our latest Quarterly Inflation Outlook. And if you make sure to put your physical mailing address in the "comment" section of the contact form, we will also send you a copy of Michael Ashton's book "Maestro, My Ass!"