Market Summary

The major stock indices settled at all-time highs this week as the so call Trump rally continues unabated. The upward move may seem a tad overextended but there is still room to extend higher into the historically strong December holiday season. For the week, the S&P 500 Index and the Blue Chip-heavy Dow Jones Industrial Average both rallied 1.4%. The Nasdaq gained 1.2% while the small cap Russell 2000 led equities again finishing the week up 2.3%. All four of the major indices closed the week at or near all-time highs and momentum is still pointing higher.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the overall stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. A few weeks ago we said "...many traders who took short positions ahead of the presidential election got chased out of those trades last week after the market started a recovery bounce...the overall market has bottomed out ahead of the December Fed meeting. November is normally a strong month for stocks which are setting up to move higher off of the recent lows..." The updated chart below confirms our analysis as the market follows through on the recovery bounce and will probably finish November near record highs.

Market Outlook

Are reported by Jeff Hirsch in the Almanac Trader, December is the best performing month for the S&P 500 and the second best month for the Dow Jones Industrials since 1950, averaging gains of 1.6% on each index. It's also the top month for Russell 2000 and third best for Russell 1000. December is NASDAQ's second best month. Rarely does the market fall precipitously in December. When it does it is usually a turning point in the market—near a top or bottom. In the updated chart below you can see the smaller cap indexes like the Russell 2000 and Midcap 400 have been leading the major indexes higher since the market bottom in the middle of August. This trend will probably continue as these smaller cap indexes are overrepresented with businesses that are expected benefit from Republican control of the White House and Congress (e.g. energy, financial, construction etc.)

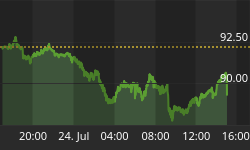

The CBOE Volatility Index (VIX) is known as the market's "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. The Volatility Index reversed course and started crashing hard a few weeks ago. As confirmed in the updated chart below, in response to the unexpected Donald Trump election victory traders immediately started bidding up equity prices. Conversely, the VIX has fallen to extremely low levels as investors expect that a Republican congress and executive branch will be pushing more business-friendly economic policy initiatives. Our analysis a few weeks ago came to fruition as we said "... Most probably the VIX will pullback and stabilize around the October 24th support level..."

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 11/23/2016. The 49.9% bullish percentage is the highest in over a year and well above the historical average of 38.5%. Conversely the 22.1% bearish percent is the lowest since the spring and well below the 30.5% historical average. At 28% the neutral percentage is under the 31.0% historical average and lowest in over a year.

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers' responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 11/23/2016. Third-quarter NAAIM exposure index averaged 80.32%. Last week the NAAIM exposure index was 83.42%, and the current week's exposure is 86.56%. Our recent comments are playing out as advertised when we opined "...The NAAIM Exposure Index will probably trend higher leading up to the December FMOC meeting..." The Trump rally continues unabated as investors rotate money out of bonds and other defensive sectors into shares of companies that are expected to benefit under a Trump administration.

Trading Strategy

It is hard to bet against the current bullish move. Short sellers got squeezed following the presidential election and were forced to chase stock prices higher. The past few weeks investors having been selling off bonds, gold, utilities and other defensive sectors. As evidenced in the updated chart below, investors are rolling into financial, industrials and other sectors expected to benefit from Republican control of the presidency and both houses of Congress. Also, historically, November begins the best consecutive six-months for the stock market. There is still plenty of cash sitting on the sidelines and any price pullback should be considered a buying opportunity for stocks on your watch list.

Feel free to contact me with questions,