Market Summary

The Dow Jones Industrial Average logging its seventh straight weekly gain, its longest streak in two years. The market ended the week flat. For the week, the S&P 500 Index and the Blue Chip-heavy Dow Jones Industrial Average were basically flat closing up .2% and .5% respectively. The Nasdaq rose .5% and the MidCap 400 moved up .4%, while the small cap Russell 2000 gained .5%.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the overall stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. Technical signals in the updated chart below confirms a strong uptrend and indicates the stocks still have room to run higher.

You can see in the chart below how the dollar has gained 5.2% since November’s presidential election. Investors expect President-elect Donald Trump to advocate for policies that will both accelerate economic growth and boost inflation. "The dollar strength will continue into the next year, but after the inauguration we will find out if the new administration is willing to tolerate the strong currency," said Simon Derrick, currency strategist at BNY Mellon. Treasury bonds finished the week higher for the first time since the U.S. presidential election amid escalating geopolitical tensions and terror attacks around the world, highlighted by recent news of a foiled plot in Australia. Investors tend to turn to the perceived safety of government bonds during times of uncertainty. Bond yields fall when prices rise. Gold prices suffered its seventh weekly loss, its longest weekly string of losses in more than 12 years. The last time gold had a run of seven weekly losses was back in mid-May 2004, according to Dow Jones data.

Market Outlook

Jeff Hirsh in the Almanac Trader discussed how Small-cap stocks tend to outperform big caps in January. This is frequently referred to as the "January Effect," In a typical year the smaller fry stay on the sidelines while the big boys are on the field. Then, around late October/early November, small stocks begin to stir and in mid-December, they take off. Anticipated year-end dividends, payouts and bonuses could be a factor. Also, it is at this time of year that of tax-loss selling abates and traders often pick up beaten-down, oversold small cap shares. Recently we said "...The current post-election bullish rally looks like it’s got more room to roam and falls in line with November historically being the start of best six consecutive months for the stock market. The updated graph below displays fourth quarter performance for the major asset classes. The biggest underperformers are gold, bonds and real estate which are expected to suffer from higher interest rates..."

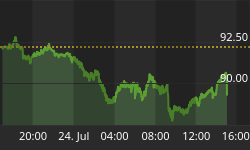

The CBOE Volatility Index (VIX) is known as the market’s "fear gauge" because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. In the weekly chart below the Volatility Index has sank low as it gets as investors became extremely optimistic about future market direction.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 12/21/2016. Neutral sentiment rebounded from last week’s two-year low in the latest AAII Sentiment Survey. Furthermore, pessimism among individual investors declined, while optimism remained nearly unchanged.Bullish sentiment, expectations that stock prices will rise over the next six months, is 44.6%, a very slight decline of 0.1 percentage points. This is the sixth consecutive week optimism is above 40% and the seventh week it is above its historical average of 38.5%. Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, rebounded by 3.2 percentage points to 26.2%. Neutral sentiment remains below its historical average of 31.0% for the third consecutive week and the fifth time in six weeks. Bearish sentiment, expectations that stock prices will fall over the next six months, fell 3.2 percentage points to 29.2%. The drop puts pessimism below its historical average of 30.5% for the sixth time in seven weeks. The Dow Jones industrial average’s proximity to 20,000 hasn't altered optimism in the survey. Since mid-November, bullish sentiment has largely stayed within the mid-40% range. This level of optimism, though above average, is within the typical historical range. (The one exception was the unusually high reading of 49.9% recorded on November 23.) Last week’s interest rate hike announcement hasn't altered sentiment much either, though opinions about it do vary as the responses to this week's special question show.

The National Association of Active Investment Managers (NAAIM) Exposure Index represents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers’ responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 12/21/2016. Third-quarter NAAIM exposure index averaged 80.32%. Last week the NAAIM exposure index was 96.23%, and the current week’s exposure is 101.33%. The NAAIM Exposure Index is at extremely elevated levels as the equity indexes made a series of all-time highs. It is reasonable to expect the exposure index to remain elevated going into the New Year.

Trading Strategy

Recently we said "...There should be another opportunity to bid on stocks from your watch list during the next market pause. Tax selling is about to commence as investors dump underperformers, also next week’s FOMC meeting should be a nonevent, but the current upward move might stall a bit..." The overall market is bouncing up against resistance from all-time highs. Now might be that opportunity to considering bidding on stocks on your watch list because the market will probably need to absorb this overbought condition before ascending higher.