Dear Subscribers,

Here is an interesting fact: It is generally well-known that if Wal-Mart was a sovereign country, it would be the 8th largest trading partner with China. Given this fact, there is a misconception that aside from groceries, virtually everything that Wal-Mart sells is imported from China - and thus any further revaluation of the Chinese currency (the Renminbi) would significant hurt Wal-Mart's bottom line. Nothing could be further from the truth. As a matter of fact, Wal-Mart only imported (directly and indirectly) $15 billion worth of goods from China in 2004 - which amounts to less than 15% of what it buys from its suppliers.

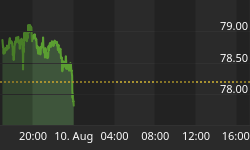

We switched from a 25% short position in our DJIA Timing System on the morning of October 21st at DJIA 10,265 - giving us a gain of 351 points from our DJIA short on July 14th. On a 25% basis, this equates to a gain of 87.75 points. We switched to a 25% short position in our DJIA Timing System shortly after noon on Wednesday at DJIA 10,840. We then switched to a 50% short position (our maximum allowable short position in order to control for volatility in our DJIA Timing System) on Thursday afternoon at DJIA 10,900 - thus giving us an average entry of DJIA 10,870. As of the close on Friday (10,907.21), our position is 37.21 points in the red - but at this point, we believe that the correction in the stock market is not over yet.

The big news last week was the shocking preliminary GDP report last Friday - which reported a staggeringly low 1.1% real GDP growth for the fourth quarter of 2005. Most of this surprisingly slow growth was blamed on a huge drop in durable good sales (especially auto sales), a tepid growth in business investments, as well as "one-time related" special events such as an increase in oil imports due to Hurricane Katrina and Rita. The consensus reaction among economists is that this was such a temporary blip (some went further and stated that the GDP number will be revised back to the 3% level in the next release) - and that GDP growth will recover back to the 3% to 4% level for the entire 2006 year.

Given our mid-cycle slowdown scenario, this author is skeptical. I have previously gone over our reasons for this skepticism - but let's briefly recap these reasons. First off is declining global liquidity - given that the ECB should hike its ST rates two to three times for 2006 and given that the BoJ should also start raising rates sometime this year. Second off is the deflation of the U.S. housing bubble. Given the subsequent decline in mortgage equity withdrawal (MEW), consumer spending should be expected to decline 1.5% to 2% in the upcoming 12 months. Please keep in mind that this estimates ignores "multiplier effects" - such as the loss of real estate related jobs due to a softening market as well as the negative "wealth effects" caused by a slowing housing market. A third reason involves some circular logic: Unless the U.S. and China economies slow down significantly starting in the next few months, there is a good chance that commodity prices will continue to rise - thus further squeezing corporate profits and decreasing consumer spending going forward. In other words, this author believes that there is "no way out" of this mid-cycle slowdown scenario - although I am not yet willing (unlike George Soros) to declare that the U.S. will experience a recession in 2007. Globalization and "offshoring" can only take you so far. Many Americans like to believe that labor in both China and India are limitless and interchangeable. Logic will dictate that this is not the case. Given that corporate profits as a percentage of GDP in the third quarter of 2005 was the highest since 1997 (and prior to that, 1969), my question is: How much further can cost-cutting go? In fact - while I have discussed the virtues and continuing trend of globalization in many of our past commentaries - there is a good chance that U.S. labor costs will start to enjoy a sustainable rise sometime this year. The whipping of the pilots' and auto workers' unions may have marked the high point of the power of capitalists and shareholders for this cycle.

Let's now get on with our commentary. Anyone that has read a book on stock market history should know that small caps have historically outperformed large caps in the U.S. stock market. This "size effect" has also been observed in many international markets - even when adjusted for risk. That being said, subscribers should know that such out-performance by the small caps is not consistent every year. In fact, history has shown that relative out-performance or under-performance of small caps relative to large caps have been relatively cyclical. That is, just like the stock market or bonds, over-performance of small caps relative to large caps also tend to experience sustained bull and bear markets.

Before I go into further details, please keep in mind that all of the following data are courtesy of Ibbotson Associates. Their datasets (which are updated once a year and published in the "SBBI Yearbook") contain the most comprehensive history of the U.S. domestic stock market - and its reliability is second to none. While the SBBI Yearbook does contain large company stocks data prior to 1926, there does not seem to be any reliable data for small companies prior to that year. Therefore - for the purpose of this commentary - let's begin our observation of small caps vs. large caps starting from the year 1926 and ending in 2004. Note that the 2006 SBBI Yearbook will be released later this March - and once this author gets his hands on a copy, I will be sure to update this study for our readers as soon as possible.

Without further ado, following is the annual chart showing the cumulative returns (for $1 invested, and with dividends reinvested) of large caps and small caps from 1926 to 2004, courtesy of Ibbotson Associates:

Looking at the above chart, there are two immediate implications:

-

First of all, small caps have outperformed large caps by a greater than 5-to-1 ratio since 1926 - and have performed especially well relative to large caps over the last 40 years. This "size effect" is significant, in that not all of the excess returns of small caps over large caps can be simply explained away by the fact that investors are incurring more risk by buying shares of small cap companies.

-

The second implication is much less obvious - and may be difficult for the uninitiated to observe this on the above chart. From 1926 and up until 1957, small caps have actually underperformed large caps on a relatively consistent basis! Why has this been the case? Throughout the 1920s and up until the Fall of 1929, many U.S. investors were willing to buy shares of small and mid-sized companies believing that they can perform or sustain themselves as well as large-sized companies during economic recessions. The huge bear market and subsequent Depression of September 1929 to July 1932 totally dispelled that belief, and for the next 30 years, investors simply refused to buy shares of small cap companies unless they were trading at significant discounts to shares of large cap companies. Moreover, more stringent reporting requirements as required by the SEC after the 1929 to 1932 debacle have also done much to improve the quality of smaller companies listed on the NYSE - thus enabling better potential returns in shares of small companies going forward.

Going forward, it may be reasonable to believe that an "intelligent investor" can simply put all his money in small cap index funds and then simply forget about them until the day he retires. But such a strategy may not be such a wise one - at least for the next few years - as small cap out-performance has also been mired in bull and bear markets ever since 1926. For example, large caps outperformed small caps in every year from 1926 to 1931. They will go on to beat small caps again in every year from 1946 to 1948, and again (with the exception of 1954) from 1951 to 1957. Just like the fact that stocks have outperformed bonds on a long-term basis but underperformed for significant periods of time, it is definitely not a given that small caps will out-perform large caps during each and every year. Following is an illustration of historical periods where small caps have outperformed large caps on a consistent basis. Note that the prerequisite is a period of out-performance of at least two consecutive years:

While final statistics have still not been published by Ibbotson Associates, it is interesting to note that Russell Investment Group (keeper of the Russell stock market indices) have already issued a statement claiming that large caps did indeed outperform small caps during 2005. If this is indeed the case, then the 1999 to 2004 period of small caps out-performance would have officially ended.

More follows for subscribers...