Cryptocurrency traders thought they could make a fortune and evade taxes, but the IRS is now patrolling the ether, and a Coinbase data dump of high-end users is imminent next month.

On Friday, Coinbase announced that it would give the IRS the names, addresses and transaction data of more than 13,000 users who did more than $20,000 in Bitcoin business between 2013 and 2015.

And it will all happen within the next 22 days.

Coinbase didn’t go down without a bit of a fight, though. It was ordered to hand over users in late 2016, and then fought it in court. They lost, for the most part, but the IRS succeeded only in demanding the data from highest-transaction users.

Symbolically, it’s a major blow for the entire sub-culture of crypto traders who were hoping to operate indefinitely without government scrutiny. But only symbolically at this point.

Those 13,000 users of Coinbase represent only a tiny fraction of its overall users, so many will be asking if the IRS really won this battle. Related: Global Cobalt Supply Is In Jeopardy

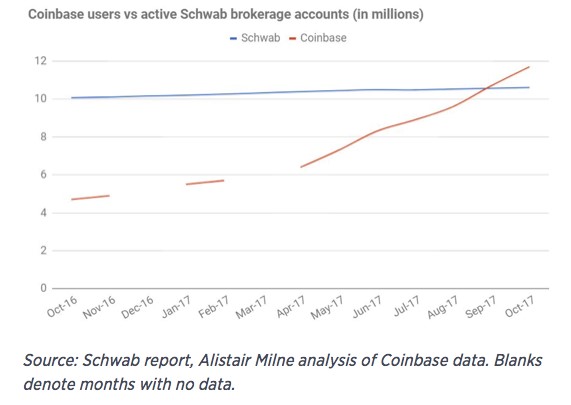

As of December 2017, Coinbase had over 13 million users. That’s more than major online brokerage firm Charles Schwab has.

(Click to enlarge)

In one week alone in November, Coinbase added 300,000 new users.

If the IRS is getting the user data from only 13,000, it’s not putting a dent in taxable crypto profits.

But it’s not just about evading taxes for some crypto traders.

Confusion rules this roost, and the IRS isn’t helping. Tax returns are cryptic enough without adding digital currencies, and there aren’t any new guidelines to follow.

IRS ‘guidance’ issued in March 2014 was vague at best, and there hasn’t been anything new since.

Compliance is tricky when there aren’t any clear rules, and the Coinbase defeat that targets only high-transaction users doesn’t mean the tax man won’t come after others.

Further complicating matters is the fact that crypto exchanges are not broker-regulated by the IRS. That means no 1099 forms and no one calculating gains for you.

The IRS is playing catch-up here, and it’s still got a long way to go in detecting who’s making money in the ether.

Cryptocurrency media report that early data from an online tax service shows that only 0.04 percent of U.S. taxpayers have filed any crypto gains or losses. It’s pretty sparse when you consider that an estimated 7 percent of Americans own cryptocurrency and probably owe taxes on these investments.

In a January survey conducted by Credit Karma, 57 percent of a pool of 2,000 American cryptocurrency owners said they had crypto profits, while 59 percent of those said they never reported those gains to the IRS.

Whether it’s a matter of tax confusion or purposeful evasion, the situation is not likely to change in favor of the IRS in time for taxes this year. If only a tiny fraction of Coinbase users are being outed, most know they’re still safe from scrutiny. But shelter from Uncle Sam is elusive: Once the IRS figures out how to really net crypto gainers, the retroactive penalties will be stiff.

By Fred Dunkley for Safehaven.com

More Top Reads From Safehaven.com: