Nowadays as you stroll down the streets of Shanghai, you are likely to encounter a unique sight that has nothing to do with the city's architectural marvels--gaggles of teenagers and millennials hunched over their smartphones messaging, shopping and sending money back and forth on Alipay, WeChat and JDPay.

There's a big fintech revolution going on in the Asian payments industry, with an explosion of digital and mobile payment platforms outside of traditional banks and credit card systems.

The future of consumer payments is being molded not in the traditional financial capitals of London or New York but in Chinese cities such as Shanghai and Beijing.

Suddenly, the average consumer is spoilt for choice

Chinese Banks Losing Out

The scary thing is that banks and credit cards are getting no cut off this action whatsoever. Nada.

Instead, everyday hundreds of millions of yuan flow through a pair of digital ecosystems that are a blend of banking, commerce and social media, and run by the country's internet and ecommerce giants, Alibaba Inc., Tencent Holdings.

That contrasts sharply with the situation back in the U.S. where hundreds of banks and numerous payment intermediaries including Visa, MasterCard, American Express and Global Payments among others feast on the billions generated from processing payments.

Just imagining the Chinese situation happening back home is a nightmare for any western banker or credit card executive who visits the country.

Alipay and WeChat Calling the Shots

Apple Pay, Google Wallet and Amazon Pay might be the most popular digital and mobile wallets in the U.S. Yet, no mobile payment app commands the kind of clout that Alipay and WeChat do in China.

Alibaba created Alipay in 2004 to give millions of customers who lacked credit and debit cards a means to shop in the vast online marketplace.

Similarly, Tencent debuted WeChat in 2005 in a bid to build a wall around its messenger system and keep users around longer. Both platforms have swelled in popularity, with Alipay boasting 520 million users to WeChat's one billion.

According to payments consultancy Aite Group, consumers transacted $2.9 trillion inside the two digital wallets in 2016 alone, equal to about half of all consumer goods sold in the country. In comparison, PayPal processed $131 billion in total payment volume(TPV) in FY 2018, or only about 4.5 percent of Alipay's and WeChat's combined volumes.

Banks and Credit Card Companies Disrupted

The biggest threat to the U.S. financial industry would be if these Chinese juggernauts, or homegrown services such as Apple Pay or Amazon Pay, are able to replicate the success of Alipay and WeChat in the U.S.

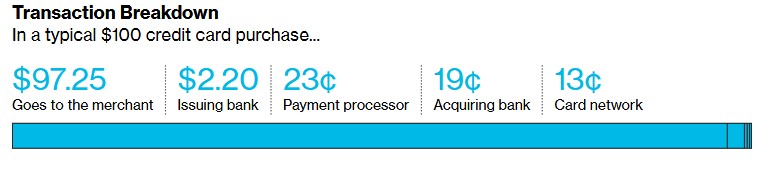

The stakes are certainly huge--U.S. banks and credit card companies skim off 2.75 percent per transaction amount from merchants as mobile payment and credit card processing fees. That works out to about $90 billion in pure income every year.

(Click to enlarge)

Source: Bloomberg

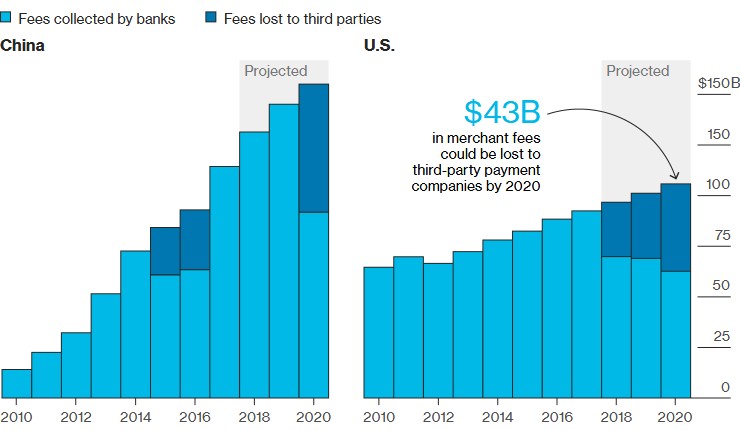

Analysts have predicted that third-party payment services such as Alipay and WeChat will account for a good 40 percent of all merchant fee income in China by 2020. A similar level of success back in the U.S. would result in more than $40 billion being lost by banks and credit card companies to third-party payment processors.

(Click to enlarge)

Source: Bloomberg

And U.S. banks should be scared. Alipay has been inking deals with payment processors that will enable the platform to set up base on American soil. Alipay says the expansion is meant to serve Chinese tourists. But don't expect the ever-ambitious Jack Ma to stop there.

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com