A rivalry is brewing in the financial space, and it looks set to transform how cross-border payments and trade are handled for decades to come.

In the blue corner is Ripple, a California-based blockchain company created in 2012 that promises to make payments faster. At a market cap of $19.3 billion, Ripple is the third-largest crypto company behind only bitcoin and ethereum.

In the red corner is SWIFT, the 40-year old giant electronic interbank money transfer platform that Ripple hopes to replace.

Sleeker Than Ripple

But now Ripple is about to be face another even more formidable challenger—a nimbler blockchain upstart created by banks themselves.

A consortium of nine of Europe’s largest financial providers—namely, HSBC, Deutsche Bank, Santander, Nordea, Natixis, Société Générale, KBC, UniCredit, and Rabobank--has teamed up and launched We.Trade, a blockchain-based cross-border money transfer platform that aims to improve the speed and efficiency of cross-border financial transactions.

The platform is built atop IBM’s blockchain, widely regarded as the leading enterprise blockchain, and is already available in 11 countries. Related: Cash Is King Once Again For Wealthy Investors

Unlike Ripple, which is strictly a money transfer platform, we.trade is designed to handle the entire order-to-payment trade process including placing orders, selecting banking products and payment terms, executing smart contracts and handling the actual payments and money transfer.

In other words, it’s a more complete product from an international trade perspective.

According to the banks, 10 companies have already used the platform to execute several cross-border financial trades.

Cold Shoulder

Although Ripple claims to have signed up more than 100 banks on its network, banks have hardly been using RippleNet for money transfers.

To-date, only Stockholm-based Skandinaviska Enskilda Banken AB is on record as having used the platform to transfer money. Even Ripple investors, Santander and Standard Chartered, have only been said to be testing it. That’s not a very good record for a company that’s been around for seven odd years.

And maybe that could be part of Ripple’s undoing.

We.Trade has been focusing on small and medium-sized businesses (SMBs), something the banks claim has been helping it scale rapidly. Ripple, on the other hand, focuses exclusively on banks.

Ripple, though, does seem to have a solid business case.

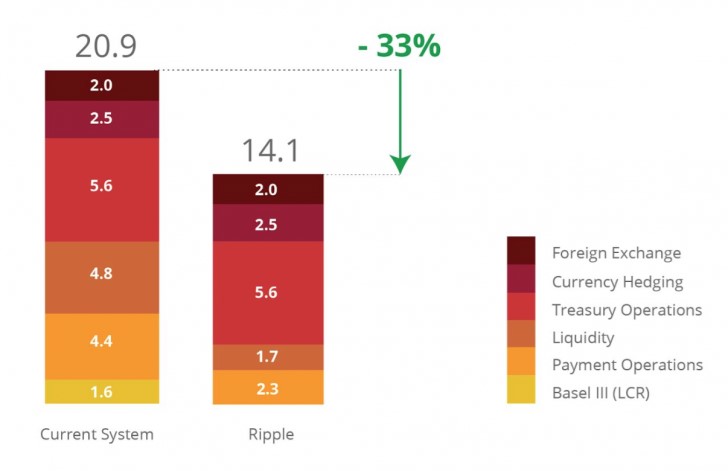

The Ripple Network has been touted as a cheaper and more efficient way for banks to move money by reducing or eliminating the need to settle transactions manually. In fact, Ripple estimates that banks using its XRP crypto for cross-border payments can save up to 42 percent, while those that use RippleNet without XRP can still save 33 percent. Further, XRP transactions are settled in just 3.6 seconds compared to days for some SWIFT payments.

(Click to enlarge)

Source: CoinDesk

But that’s just part of Ripple’s value proposition. Banks can use the XRP token as a currency bridge and a lingua franca that helps them avoid tying up money in varying currencies held in foreign accounts.

Related: Venezuela Gets A $5 Billion Lifeline

In other words, it can help banks improve their liquidity.

Still, banks are some of the biggest and oldest financial institutions around, and these massive vessels take ages to turn around.

Further, the banks would probably have to negotiate mountains of regulatory hurdles in order to use Ripple.

But these banks can be grateful that Ripple has provided them with a blueprint on how to use blockchain to get their systems up to speed in today’s world where business moves at the speed of thought.

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com: