On Monday, Wells Fargo & Co (WFC) shares closed up nearly 3 percent, even though it reported a weak Q2 on July 13 and has been caught doing everything from illegal car repossession and fraudulent credit card cross-selling to—most recently—tricking customers into a slew of services lacking in transparency.

(Click to enlarge)

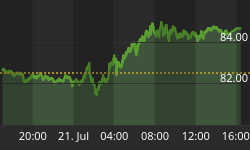

But the past year has been a bumpy one for share prices:

(Click to enlarge)

We knew about the opaque products last year, when Wells Fargo disclosed it in a regulatory filing. The bank is now reviewing the products and the remediation efforts are so far resulting in some nice refunds.

But while Wells is doing its own review, Federal regulators are reportedly investigating as well in an effort to determine whether customers were deceived into purchasing these add-ons, which include everything from pet insurance to identity theft products.

And refunding hundreds of millions of dollars to add-on customers comes right after Wells Fargo took a $619-million Q2 2018 charge to refund customers over another scandal: overcharging in multiple units: foreign-exchange, wealth management, auto-lending and mortgage-lending.

Tracing it back it further, the bills get even bigger.

In April, the CFPB won a $1-billion settlement from Wells Fargo over its failure to manage risk. Related: Americans Grow Weary Of U.S. Trade Policy

Back in 2013, Wells Fargo launched a new policy for locking in interest rates on mortgage loans, charging fees to customers if it was deemed that a rate-lock extension was necessary due to some vague fault of their own. The fee typically came into play when the bank said borrowers didn’t get them documentation on time, or an appraisal for a new home purchase didn’t come through as expected, causing a deal-closing delay. If the fault was the banks, then no fee would be charged. But the fees got out of hand, according to regulators. As it turns out, bank employees didn’t really know all the rules here, and borrowers were being charged these fees arbitrarily—and extensively all the way up to March 2017.

As ZeroHedge puts it, the mounting problems for Wells Fargo are an indication that Trump CFPB appointee, Mick Mulvaney, “is keeping the pressure on” the bank.

In the meantime, the bottom line is hurting. Earlier this month, Wells announced that its operating losses had spiked 77 percent last quarter, while profits took a 12-percent dive.

Share prices will likely catch up to this misfortune.

So, Wells Fargo is looking for some good PR right now—in the form of charity. This week, it revealed plans to get more philanthropic with a pledge to give away $400 million to non-profits, schools and other ‘good causes’ this year. That would be a 40-percent uptick in charitable giving for the bank at a time when its bottom line is being questioned.

By Michael Kern for Safehaven.com

More Top Reads From Safehaven.com