So here we are at the beginning of a new week. Last week in this space, I shared my view that machinations in today's financial markets are reminiscent of the lead up to Weimar Germany's hyperinflationary experience in a piece titled, An Ode To the 200-Day Moving Average.

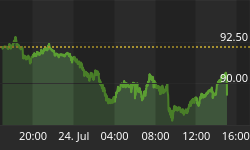

Last week's action in the precious metals was exciting and unusual. COMEX silver futures began last week sub 13 dollars, then rallied in melt-up mode over a period of three days to within a whisker of 15 bucks before being crushed down to an inter day low in the mid 11 dollar range. At one point on Thursday, April 20, 2006 - the price of COMEX silver futures was down more than 20 % with the bulk of the fall in price coming in a 45 minute time span shortly after 10:00 am ET.

I began wondering why or how such a plunge in price could occur. Having worked either in or around financial markets for more than 20 years - I first felt that some unexpected "breaking economic news" item was just released or perhaps some unexpected geopolitical event had occurred. Upon investigation, all that was released at 10:00 am that day was Leading Indicators - published by the Conference Board. With this number being reported [-.1] much as expected along with the fact that 'Leading Indicators' as a number is only credited with an importance of D- on a market-moving-scale of A to C, there had to be another credible reason for the plunge - but what?

Perhaps investors had finally relented and given in to the disinformation in the mainstream financial media that "commodities" are collectively way overdone on the upside and it was time for a rest. Funny thing [if you consider a 20 % massacre of a global financial/commodity market inside 45 minutes funny], on Thursday morning [April 20] the pm. gold fix in London was 644.50 [silver at 14.31] indicating continuing robust demand in the "physical" London market. Cast in this light, the obliteration of the COMEX silver futures price appears to be even odder still. Claims that investor sentiment had simply changed so suddenly - [intra-day] - on no news - ring hollow.

By late afternoon last Thursday [Apr. 20], none other than GATA lieutenant, Mr. Ed Steer had "connected a few dots" and penned an ingenuous piece titled, A Last Desperate Act? In this piece Steer related,

"I heard from a very reliable source yesterday (April 19th) that the COMEX was meeting in emergency session. Knowing the reputation of this organization, I imagined that it certainly had to do with the current goings on in the precious metals market...especially silver."

How Metals Bulls Are Tamed

Steer went on to point out in his piece how COMEX has been repeatedly raising margin requirements for both gold and silver futures contracts since the New Year. There is a wide and growing body of evidence to suggest that Exchange mandated margin increases, in practice, specifically punish speculative longs - much more so than commercial shorts. With 7 margin increases [the last two, Apr. 18th and 20th not shown on graph] since Jan. 10, 2006 [6 prior to the Apr. 20 massacre of silver], the "usual" tonic for bringing unruly high metals prices under control was clearly not working - and for good reason.

You see folks, the precious metals markets have undergone [it's been occurring for some time and greatly accelerated since last August, when GATA held Gold Rush 21] a transformation - in that a new type of investor has entered the game on the "buy side". These new players are better capitalized [some being sovereigns] than former 'bag holders' for COMEX price manipulators - and thus they don't 'shake out' or liquidate their positions quite as easily. So, old tricks weren't fooling the new dogs.

Solution: New Tricks!

Steer speculates [a speculation with which I concur], that to induce metal "longs" to capitulate and sell their positions, the shorts "colluded" and collectively withheld their bids,

"I could just see the dealers in the pits right now...standing there with their arms folded as the longs (including the tech funds) sold into a vacuum. Since there were no buyers...the price fell off a cliff immediately."

Steer goes on to add,

"When the sellers did catch a bid, it was the desperate dealer shorts standing there with buckets to collect the equally desperate long positions that were being dumped. This is the engineered sell-off that Ted Butler had been waiting for - for so long. This is brazen market manipulation at its worst...engineered by the very people are supposed to be preventing this sort of thing."

The whole thought of this 45 minute "licking" to which silver had been treated got me thinking even further. I decided to look up another mathematical genius whose name should be familiar to many of you - Mr. Michael Bolser of Interventionalanalysis.com. I sought Mr. Bolser's input to determine whether he had statistically calculated the odds of Thursday's sell off in silver. What I got was little bit more than I had bargained for, with Mike sharing his thought that volatility and standard deviation in silver run high, making last Thursday's big move very unusual but not unprecedented;

The huge $2.81 move in one day is very unusual but not unprecedented. THAT it was due to dealer collusion (To cease bidding) is beyond question. Is this unethical? Yes. Does Congress approve? Yes. Just as Congress and the president approve of absurd lumber tariffs, cotton subsidies to create an oversupply (Hence low prices) and tobacco subsidies NOT to grow to maximize state tax revenues. It is ALL a free-market-wrecking scam.

Then he went on to add:

We are in agreement that the silver intervention was an artificial event. Indeed, IMO all strategic commodities are under artificial management 24/7.

However I see the high oil price as wholly a voluntary event by the admin as the SPR is overfilled to such a degree that (1) they can't find any where else to put oil (2) OPEC themselves say the fundamentals don't warrant the price today and (3) Iran is a long way from fissile materials according to John Negroponte's last statement this weekend.

Thus, geopolitics were chosen to create high oil prices as a perk to big oil before a takedown. My view in this regard is as controversial is it can possibly be. On my side is the up-tick oil took on Friday out of my DIVO tracking channel this is similar to the up-tick gold took just before last week. TA shows strategic commodities as way over bought.

There is no doubt that fundamentals, interdependent economies and derivatives are at precarious levels. However, so is the determination of the cartel's members to apply even more pressure to assert their presence. They won't break ranks in the central bank area as some think. Indeed they can sell back and forth to one another behind the scenes.

Beware the mistakes of Nelson Bunker Hunt who stood on the trading floors thinking he had cornered the silver market at a time when the Defense Department Stockpile possessed nearly 15 [million?] tonnes of the stuff. What was he thinking? That the US government would go down to financial defeat and ignominy without selling that massive stockpile? To kill Hunt they didn't even need to touch the hoard. All they needed was a few rules changes once they had positioned him is an inescapable place. This is the tenet of Bigger and Badder.

I know they have control of oil and are still in control of gold as they carefully retreat. In the case of gold they carefully constructed a third, fourth and are now in the fifth of five TA waves.

I don't agree that the silver move was a desperate act. On the contrary I see it as another move to place longs in places where they can't escape.

So there you have it folks, three market commentator's assessments of the current situation. We mutually agree that prices of strategic commodities are under artificial management 24/7. We arrive at this broad conclusion from both a fundamental and technical approach. Our few differences stem from how long we think this charade can continue while being in complete agreement that the end, whenever it comes - will most assuredly be a train wreck of Hollywood epic sized proportions.

Technically Speaking

On a closing note, because I forgot last week, I would like to share with everyone just how the price of silver and gold escalated in German Mark terms, through the Weimar experience:

Technical Analysts believe that the historical performance of stocks and markets are indications of future performance.

Hyperinflation: Wiemar, Germany January 1919 to November 1923

[Expressed in German Marks needed to by an oz. of ag. or au.]

Jan. 1919 Silver 12 Gold 170

May. 1919 Silver 17 Gold 267

Sept. 1919 Silver 31 Gold 499

Jan. 1920 Silver 84 Gold 1,340

May 1920 Silver 60 Gold 966

Sept. 1921 Silver 80 Gold 2,175

Jan. 1922 Silver 249 Gold 3,976

May. 1922 Silver 375 Gold 6,012

Sept. 1922 Silver 1899 Gold 30,381

Jan. 1923 Silver 23,277 Gold 372,447

May. 1923 Silver 44,397 Gold 710,355

June 5, 1923 Silver 80,953 Gold 1,295,256

July 3, 1923 Silver 207,239 Gold 3,315,831

Aug. 7, 1923 Silver 4,273,874 Gold 68,382,000

Sept. 4, 1923 Silver 16,839,937 Gold 269,429,000

Oct. 2, 1923 Silver 414,484,000 Gold 6,631,749,000

Oct. 9, 1923 Silver 1,554,309,000 Gold 24,868,950,000

Oct. 16, 1923 Silver 5,319,567,000 Gold 84,969,072,000

Oct. 23, 1923 Silver 7,253,460,000 Gold 1,160,552,662,000

Oct. 30, 1923 Silver 8,419,200,000 Gold 1,347,070,000,000

Nov. 5, 1923 Silver 54,375,000,000 Gold 8,700,000,000,000

Nov. 13, 1923 Silver 108,750,000,000 Gold 17,400,000,000,000

Nov. 30, 1923 Silver 543,750,000,000 Gold 87,000,000,000,000