Moneyization: The global financial phenomenon of individuals and businesses moving their funds to monies in which they have the highest confidence, or money in which they have a higher store of faith.

Or, We Have Meltdown

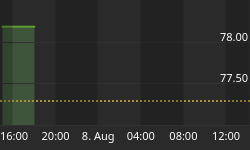

Around the world, investors are shedding their national monies and moving to Gold. Quite simply, they have higher faith in Gold than that money produced by their governments. Gold, neither managed by a central bank nor a liability of a government, has been and continues to be the money in which investors have higher faith. Little wonder with the record of governments and their debt money that Gold is moving toward a new long-term high dollar price as it moves in a greater bull market to more than US$1,300.

So, how do you know when your country's money is not worth much?

A. Moneychanger at airport in small country laughs at you.

B. Restrooms have money changers to convert 20s into 1s.

C. Sign in restaurant says, "Checks only!"

D. When scrap dealers are melting down the coins.

For some time Gold bugs and writers on the merits of Gold have been critical of Federal Reserve policies and the spendthrift ways of the U.S. government. We have written till our fingers hurt that the value of the money would be destroyed. Even US$650 Gold is ignored by the inbred group of economists running Washington. The latest run in Gold to a high was brought about by the testimony of Chairman Bernanke. Global money markets are voting, thumbs down on Federal Reserve policy and thumbs up on Gold

The answer to the big question above is D. The scrap dealers are about to have a new line of business, melting down U.S. pennies, US$0.01 coins. The U.S. government, and most others, debased their national monies many decades ago. The ultimate debasement was when paper money was forced on the citizens. We still have, though, some metal coins to at least preserve some semblance of national dignity. What respectable nation would have all denominations of money in paper form?

Many of us can remember back to when the copper penney became a historical relic. Diligent workers at the U.S. mints conjured up a new mix of copper and zinc for the lowly penney. The purpose of that action was to destroy any remaining intrinsic value of the coin. Such a move would prevent the melting down of the copper pennies for the copper in them. Presumably once done with that deed, they went on to reformulate the consumer price indices. However, global demand for commodities in a world with surplus dollars has caused price relationships to adjust once again.

As Graph One shows, the meltdown value for U.S. pennies is fast approaching. Yes, for simplicity we are ignoring smelting and other costs. More importantly though, we are looking at the intrinsic value of the U.S. one cent piece. Will it be worth more as scrap metal or as money? And is this development an omen of the future value of other denominations of U.S. money?

The U.S. penney is composed of copper and zinc. Exact specifications can be found for all U.S. coins at the Mint's page through the U.S. Treasury website. Prices for these metals are rising around the world in dollars, as most people around the world have more dollars than needed. Those dollars are being spent on oil, on copper, on zinc, on Gold, on just about anything real. The dollar prices of such real assets have been rising because the real value of the U.S. dollar is both imaginary, illusionary, and destined for decimation.

Above was asked if the coming meltdown of the U.S. penney was an omen for the other denominations. The answer to that question is yes. For as the scrap value of the penney rises above US$0.01 converting any denomination of U.S. dollars will be profitable. Just turn them in at the bank for pennies. How the U.S. government will respond to that development is the next issue. The Mint could continue to mint pennies at a loss, or negative seigniorage. Or the U.S. could reformulate again, and validate the view that the dollar's value is doubtful at best.

As a consequence of Moneyization, the move to monies of higher faith, the meltdown value of the U.S. penney is moving higher. The termites start with the foundation of the house, working themselves higher over time. The same is true of the "monetary termites" which are slowly consuming the value, the wood, of the fiat monetary system. You have a choice, be food for the "monetary termites," or move on to Gold, the money of higher faith.

The world is slowly sorting out the hierarchy of money. At the top, Gold has returned to the millenniums old role as the first tier money. In second tier is a narrow group composed of the Euro and the renminbi, which are ascending to new global roles. The third tier is the U.S. dollar which is beginning its era of decline. Fourth tier is composed of Canadian, Australian, Swiss, and similar national monies which either due to history or economic circumstances are destined be become obsolete monetary relics of a former era. Lastly is all the rest, which are to be monetary toast and should not be owned at all.

Gold's return to its historical role as the premier global money is readily observed in the higher price for Gold in nearly every national money. Too many investors have not made the move to Gold, and remain to be convinced. Some are still hoping that paper assets will return to the great days of 1929 and 2000. However, hope has never fed anyone. Others remain overexposed to debt backed by their homes, believing the silly notion that one can never lose money in real estate. Time will crush that view. However, what many do not realize is that over the past 34 years Gold has been a better investment than housing. Home prices are simply a money illusion. See second graph.

In the second graph are plotted the indexed values for quarterly $Gold prices and home price in the U.S. $Gold prices are the triangles and home prices are the solid line. For U.S. home prices the Freddie Mac Conventional Mortgage Home Price Index is used. This measure is published quarterly by Freddie Mac. This index is superior to other measures due to the large data base of the company. They are able to capture repeat trades, or repeat sales of the same property. In measuring stock prices, we use the change in the price of IBM stock, for example, over time. The widely followed median price measures compare, for example, trades in IBM with trades in MSFT, which tends to distort the data.

Astute observers will realize that during these 34 years periods existed when home prices did better than Gold. Yes, that is true. However, selling your house and putting all the money in Gold is not the recommendation. Putting all your eggs in one basket, Gold or a house, would be an error. Gold is a wise addition to the total portfolio of an astute investor. Having all your exposure to real assets represented by speculation in a house is not wise. The third graph presents returns on various periods, and all it proves is that Gold should be included in your total portfolio. Well, maybe it proves also that the real estate bugs don't know what they are talking about.

The first and most important argument being presented here is that Gold should be included in the portfolio of each and every investor. This recommendation is especially true for those with most of their wealth concentrated in paper assets and/or a home. Gold can help you diversify your assets. A second concern is that housing debt and housing prices are a serious threat to the viability of the U.S. economy. That situation creates a derived threat to Canadian investors. This risk is one many continue to ignore as they are lulled into complacency by the Canadian dollar's appreciation against the U.S. dollar.

The widely accepted thesis is that the Mortgage/Housing Bubble in the U.S. is unwinding. Damage to the economy will be considerable as the default level rises on mortgage debt. Spillover impact on Canadian economy will be great due to the exposure to the U.S. economy. Both national monies are at tremendous risk. For that reason we need to monitor the imploding U.S. housing bubble. Hopefully, such an effort will encourage more investors in both countries to reduce their exposure to both dollars.

| U.S. HOUSING BUBBLE BURST TRACKER in Nominal U.S. dollars. | ||

| March 2006 Data | Single Family | Condo |

| Peak Price | Aug 2005 | Jun 2005 |

| Price Decline - Annualized | - 9% | - 4% |

| Sales | - 3% | - 9% |

| Inventory For Sale | +10% | +51% |

| Data: Median Prices from NAR | ||

Two aspects of the unwinding of the housing bubble are relevant. First, what has happened thus far? This view is through the rear view mirror of the car. That information is readily available from the regular reports. Recently for example, the National Association of Realtors reported on existing home sales. Relevant information derived from that report is summarized in the above table. However, a note of caution is important. NAR made revisions to the methodology and the data. That combined with somewhat less than desirable reporting of the data does give the appearance of skewing the report to a positive note. Clearly though prices have peaked, and, secondly, prices are going to get weaker. That latter view is supported by the rising level of unsold inventory.

The information we have considered thus far, as suggested, is looking in the rearview mirror. What is the outlook through the front windshield? Graph four give a fairly clear indication of the future trend. In that graph is plotted the weekly index of applications for mortgages to buy homes released weekly by the Mortgage Bankers Association. The trend has only one interpretation, and the latest data point is a new low. The mortgage broker is slowly becoming the "Maytag repairman" of this decade.

As always, we follow the money. Fewer applications for mortgages mean fewer dollars available to make purchases of homes. The only way transactions can occur in such an environment is through lower prices. Lower prices mean that less equity will be extracted on sale, and in some cases inadequate equity will remain to fully repay any indebtedness. Naturally, some potential sellers will not strike a deal. In these cases all that is being done is the compounding of losses, making the ultimate resolution of the debt more painful.

Chairman Bernanke confirmed again this past week in testimony before a Congressional committee the lack of any plan at the Federal Reserve. In short, he said that at some meetings of the FOMC rates might rise and at some meetings rates might not rise. The duck outside the window could have provided the same insight. Such a response in many ways is what to be expected from a lackluster leader. The monetary policy of the U.S. economy, the survival of the dollar, and integrity of the global economy now rest with a mediocre, politically motivated academic. Think back to all the college professors you might have had. Would you turn over to any of them responsibility for the global financial system?

The U.S. dollar quickly plunged on Bernanke's testimony. Gold moved ahead, seeking out a new cyclical high. With the crumbling U.S. Housing/Mortgage Pyramid scheme as background, we now have a less than inspiring academic running the Federal Reserve. Global holders of dollars knew what to do: Sell! Foreign exchange markets are sending a signal that should not be ignored, and needs to be correctly interpreted. The signal this week was that the U.S. dollar's value is tenuous, and the dollar went down. Do not fall into the trap of interpreting the market signal as that your national money, Canadian dollar for example, will get stronger. Gold's price trumped all.

Gold investors clearly are on the right train. The disastrous economic fundamentals created by the former leader of the Federal Reserve are clearly evident in the housing problem. The selling of dollars in response to Bernanke's testimony is simply confirmation that the path of least resistance for the dollars is down. Investors in the U.S. and Canada that remain complacent in such a situation will clearly be available for yard work in future years.

That Gold's Super Cycle is unfolding is no longer at doubt. The only remaining questions are how much Gold an investor should own and when should it be bought. You must answer the first question. Methods exist to help with the latter, as presented in the last two graphs. Graph for Euro Gold is available.

The closing note is on an amazing financial, or business, characteristic of the past year or so. The Federal Reserve has raised interest rates fifteen times, from 1% to 4.75%. Thus far no serious nor notable failure event has occurred because of this change. That lack of event would seem to be a historical oddity. Somewhere out there is a ticking financial time bomb. Somewhere someone had misjudged their true risk exposure. In June we know the hurricanes will come, just not where and when. A "monetary hurricane" is brewing in this financial environment, only when and where is not known. The time for insurance, Gold, is before the storm hits.