Dear Speculators,

The Dynamic Trading System took profits of +5.1% and +0.2% last week on the S&P 500 and the Nasdaq 100 E-Mini Futures contracts. The System has netted over +450% in position gains since the Index System Service was launched in July '05. The net total return of of the model portfolio is +147% (76% winners). The monthly Sharpe Ratio is 2.9. (The Sharpe Ratio measures volatility-adjusted return. A ratio of 1 is considered good, a ratio of 2 is considered very good, and a ratio of 3 is outstanding.)

If you're interested in reading more about the The Agile Trader Index Futures System click HERE.

Or if you would like a 30-day FREE TRIAL to The Agile Trader click HERE.

TRADING THE MARKETS

There are a couple of factors in trading the markets that are more important than being "right" about what the markets will do. First and foremost is to have a plan for what YOU'RE going to DO. What will you do if you're right and what will you do if you're wrong?

The second factor is being capable of accurately, quickly, and without hubris, assessing when indeed you are wrong...and then IMPLEMENTNG the plan for what to do in that case.

Since early this year I have been laying out the case for a mid-term decline phase, specifically in the S&P 500, as we head toward the 4-Yr Cycle Low, most likely in the September-October '06 time frame. But the SPX has defied gravity and continued to eek out incremental new highs despite a gathering of stormy headwinds (flattening yield curve, rising interest rates, rocketing commodities (esp. Oil) prices).

To put things in perspective, Doug Noland of Prudentbear.com points out the following:

Gold is up 27% y-t-d to the highest price since 1980, with a 52-week gain of 51%. Silver has gained 51% in less than four months to a 23-year high (52-wk gain of 90%). Crude oil is up 18% y-t-d and 38% over the past year, last week trading to an all-time record. Unleaded Gas futures prices are up 40% from a year earlier. The Goldman Sachs Commodities Index is up 34% over the past year, closing last week at a record high.

All this as the Fed has raised the Fed Funds Rate from 1% to 4.75%, on its way 5%, in roughly the last 2 years, with the spread between the 10-Yr Treasury Yield and the Fed Funds rate down from 380 basis points to 28 basis points (ostensibly tightening monetary conditions, diminishing profitability on the carry trade) in the same time frame.

But the financial markets (and I include commodities in that category, for our purposes) can have unexpected and even paradoxical reactions. And the analogue to the current situation--one I can't get out of my head at the moment-- is the Nasdaq Composite of 1999.

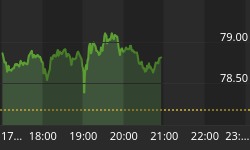

Here's the current SPX chart.

Note the sharp rally off the October low and the creeping, shallow continuation since November.

Now, look at the chart of the Nasdaq Composite from October 1998.

Note the sharp rally off the October '98 low and then the creeping, shallow rally that extended through most of 1999...only to be followed by one of the astonishing upward surge from October '99 through March '00.

What happened to create that rally? Well, among other things, the Fed pumped up money supply as prophylactic action against the much-feared (imagined) Y2K catastrophe. So, while rates were tight, money was plentiful, and much of that money found its way into the speculative frenzy of the Nasdaq Composite.

Today's version? Hedge Funds and Commodities.

In 2003 regulations were changed such that Hedge Funds no longer had to register with the Commodities Futures Trading Commission in order to trade in the Commodities Markets. And look what happened.

Gold, which had been trading down in the mid $200s, suddenly found buyers. (Not that there weren't other dynamics at work, but the fact of broadening the pool of buyers to include virtually all Hedge Funds sure didn't hurt.) Note the sharp trend from $340 to $431 in 2004, followed by the creeping, consolidative uptrend into '05, which finally morphed into a speculative fervor that has persisted into '06.

And the story is not terribly different with Oil.

The exponential ride began at the end of 2003 (the year in which Hedge Funds came full force into the Commodities Markets). This following a drifty upward creeping period that itself had followed the sharp rise from $10 in the latter '90s.

Why do I bring this up? And what does it have to do with our "knitting?" (The stock indices, to which we try to stick?)

Despite our 4-Yr Cycle studies, which suggest that there is something like an 80% probability of the market entering into a decline phase between now and October, it is always possible that the unlikely scenario will obtain (unlikely means unlikely, not impossible), and that the SPX will break to the upside from its shallow, creeping, consolidative uptrend and launch itself into a moon-shot, just as the Nasdaq did in 1999, and as Gold and Oil have done more recently.

And how would we know if/when that was happening? Well, as we've discussed at length in our daily work and in this space, a clear buy signal initiated off broken resistance at SPX 1300 would be the first indication of a more aggressive new uptrend, a signal which COULD happen at any time, but which we do not have at present. (Have a look at the first chart at the top of this article and you'll see that the SPX is tromping back and forth over 1300 (yellow highlight) "flattening down the grass" at that level, and making the chart muddy and difficult to read -- which is one of the market's favorite pastimes.)

And what would cause the launch of such a moonshot? Well, if the Fed, as per Chairman Bernanke's comments last week, decides that rising inflation, surging commodities prices, and tight resource utilization data just don't matter, and that they're just going to pause and let the economy (and the markets) do their thing for a while.

Remember, Bernanke is explicitly in the "we can't know a bubble in real time, we can only clean up after it" camp. And this past week he stated that new data since the last FOMC meeting has not changed his view; new data that includes Crude Oil's rise from $64 to $75+ as well as Gold's rise from the $560s to the $650s.

If the Fed does indeed pause, then the stock market (as well as the commodities markets) may well take that as the "all clear" signal, and the stock market may just decide to skip the 4-Yr Cycle imperative of a decline, and choose instead a "cycle inversion," which could send the SPX skyward in a kind of "meltup."

Would that be healthy for the stock market? No. The only 2 counter-cyclical meltups at this point in the 4-year cycle that we've seen in the last 45 years have been in 1986 and in 1998, both of which were followed by harrowing market declines (in Octobers 1987 and 1998, respectively), both of which, ironically, required immediate Fed rate CUTS!...So, by PAUSING in the near term, the Fed could very well engender a market meltup, which would very likely be followed by a meltdown, which itself would force the Fed to CUT rates. (Twisted, eh?)

But in the meltup scenario, we would very likely see Oil over $80, gas at the pump at $4+ and Gold chasing $800/oz. Possible? Certainly. Appealing...not so much for the economy.

The meltup scenario would put the stock market in a position for a truly nasty crash, just like the Nasdaq meltup of 1999.

EARNINGS AND VALUATION

All of the above said, the trend in earnings projections appears to be healthy.

The consensus for Forward 52-Week EPS on the SPX (blue line above) now stands at a new all-time high of $87.11, with supportive positive trends in both Trailing 52-Week Operating EPS and Reported EPS.

The SPX PE on Forward 52-Week EPS (blue line above) now stands at 15.0.

In a very real sense the stock market has been fairly rational over the past couple of years, with the PE holding fairly constant between 14 and 16.5. Interestingly, the SPX PE has been much less volatile than the analogous statistic on the 10-Yr Treasury, the Price/Dividend Ratio (black line above), which is now at 19.7, down from 25.5 last June.

Put differently, the stock market's valuation has been less volatile than that of the bond market. And as a function of the bond market's volatility, the Equity Risk Premium (ERP, a measure of the stock market's valuation relative to the bond market) has fallen back just about into its "normal" range.

ERP (pink line above) measures the difference between the 10-Yr Treasury Yield (5.07%) and the SPX's Consensus Forward Earnings Yield (the inverse of the PE, now 6.65%). (6.65%-5.07% = 1.58%).

With ERP at 1.58%, the stock market remains cheap relative to the 10-Yr Treasury, but less so than it has been for most of the post-9/11 period. (Median ERP in the post-9/11 period is 1.95%.) If the stock market is returning to a "normal" ERP (near 0%) then the stocks can move much higher. But with Crude and Gold soaring, with the dollar falling, and with the economy levered up with an unprecedented level of systemic debt, our suspicions are that we are NOT returning to a normal period. The systemic risks, in our view, remain elevated. Consequently our RISK ADJUSTED FAIR VALUE (RAFV) target for the SPX is now below the SPX price.

RAFV is derived by the following equation:

RAFV = F52W EPS / (TNX + Med ERP)

Where:

RAFV = Risk Adjusted Fair Value

F52W EPS = $87.11

TNX = 5.07% (10-Yr Treasury Yield)

Med ERP = 1.95% (Median Post 9/11 ERP)

RAFV = $87.11/ (5.07%+ 1.95%)

RAFV = 1243

(Note: RAFV is off by 2 points in this equation as presented, owing to rounding errors for TNX and Med ERP)

To sum up: We continue to view the SPX as likely to enter a mid-term decline phase between now and October. However, we are open to the possibility of the "melt up" scenario should the Fed stick its head in the sand vis-à-vis the commodities bubbles and go into "pause" mode. Our view is that the data-dependent Fed should be depending on the commodities data for guidance on what its policy moves should be. But then again, the Fed isn't asking our opinion on the matter. So, we continue to watch how the market reacts to the SPX 1300 level. And once buyers and sellers are through trampling on that price point, we'll have a clearer indication of the next mid-term trend.

Best regards and good trading!