"Silent Dollar Crash" Becoming Louder

The "silent dollar crash" that I wrote about in my last article link, is getting too large to ignore by the mainstream, including the ongoing disparity between the skyrocketing price of gold and financial markets continuing euphoria.

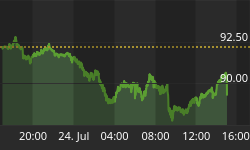

Gold is up around 40% this year, touching $728 today, with the Fed funds rate at 5%, reported inflation still low, and the MSCI World equity index setting a record this week, surpassing its March 2000 high at the end of the TMT bubble. This is the highest gold price since 1980, a year in which the consumer price index rose 13.5% and the Fed funds rate touched 19%, and two years before the end of a secular bear equity market that lasted more than a decade (inflation adjusted).

What Does Gold's Rise Signify?

At the moment, equity markets are reacting negatively to the belief that Fed tightening might not have ended, while the dollar has been under pressure recently partly from the opposite belief, i.e. that yield differentials in its favor will be less supportive if the Fed stops tightening.

FT market columnist Philip Coggan asks Thursday: "is bullion's rise a signal that investors are worried about inflationary pressures and a dollar collapse or is it simply a symptom of speculative enthusiasm? The answer has enormous implications for investors." Energy, geopolitical and other issues also strongly factor into interpreting the significance of gold's rise.

Also in Thursday's FT, Helmut Eschwey, the chief executive of Heraeus, a family-owned German group that is the world's largest precious metals trader, "said it was "impossible to predict" when the bubble would burst for silver and gold but that it would take place," certainly sufficiently vague but still worth noting.

With hedge funds and other hot money crowding into smaller asset classes such as precious metals, emerging markets and anything else going up, liquidity issues are important, in both directions.

In Parallel Investment Universes, Wall Street Remains Optimistic

As I mentioned in my last article, the strong divergences of price action and differences of expert market opinions right now almost makes it feel as if there are parallel investment universes.

On Wall Street, with investor euphoria remaining at 20-year highs, a couple of the perennially cautious voices have become more positive in recent weeks, e.g. economist Roach at Morgan whom I mentioned in my last article and now strategist Bernstein at Merrill, who has upped his equity weighting from 40% to 50% and joins the already long-running party preferring the lower-quality stocks.

While Others Express Rising Concern about a Possible Dollar Crisis

On the other hand, away from the sell side, some respectable mainstream voices are expressing more concern about a possible dollar crisis. E.g., an article by Peter Brimelow in MarketWatch today link quotes the May 10 Daily Letter headlined "The Tremors Before the Big One" from Bridgewater Associates, a well-regarded firm, "We believe the odds of a dollar/ U.S. debt crisis in the next twelve months are elevated (say 50 percent)."

In an earlier Letter Bridgewater said: "Today's imbalances are much larger and global in scale." ... "bigger imbalances that have taken longer to build, have been sewn deeper into the economic fabric, and will take much longer to unwind, with dramatically larger financial consequences." "...Now you've got a new, academic, waffling Fed chairman, a falling dollar, a falling bond market, rising gold and commodities prices, and an underperforming stock market all with a giant current account deficit ..." Bridgewater concludes, "Bernanke is rapidly losing control."

Edwin Truman (of the D.C. think-tank Institute for International Economics, who directed the Fed's Division of International Finance from 1977 to 1998 and was on the staff of the Fed's Open Market Committee from 1983 to 1998 under Volcker and Greenspan before serving as assistant Treasury secretary for International Affairs to 2001), according to a May 8 article in the WSJ link, "isn't among the doomsayers; he predicts that there's just a 10% or 15% probability of a "catastrophic collapse of the financial system." "But I wouldn't rule it out," he says. "The possibility of somebody doing something foolish or stupid has gone up, and there's no doubt about that.""

And the Risks of Unwinding Carry Trades

Concerns about the effects of rising rates, especially in Japan, on carry trades that are helping to fund the continuing huge run-up in emerging markets, among other things, are voiced in a report by GaveKal posted at "InvestorsInsight" link: "The leverage in the system has continued to grow in the face of rising interest rates from most central banks ... the overall leverage in the system today is probably more prevalent, and widespread than most realize ... a fair amount of the leverage has taken place in Yen ... if the central banks are serious about taming the global inflationary pressures, then the tightening now has to happen in Japan. In a sense, this tightening has already begun."

Similar remarks about carry trades were also recently made by Dr. Kurt Richebächer at "The Daily Reckoning" link: "Due to the gigantic leverage implicit to carry trade, a modest rise of the yen, euro and Swiss franc against the dollar by just 2-3 percentage points is enough to abruptly torpedo the whole carry trade in these currencies, triggering a fire sale of unimaginable proportions of both dollars and U.S. bonds. In our view, this is plainly written on the wall, and a true miracle is needed to avoid this debacle. ... There is no way to know the depth and pervasiveness of the U.S. carry trade funded in foreign currencies. In our view, it must be immense, simply because there exist no domestic savings to fund the rampant credit expansion. The whole U.S. financial system is built on carry trade, borrowing short and lending long."

A "Silent Accord" to Deal with Global Economic Imbalances?

One hypothesis on how to deal with these problems was floated in an FT story on May 10: "David Bloom, currency analyst at HSBC, lent his weight to the intriguing theory that the G7, at its recent summit of foreign ministers, might have hatched a tacit plan to allow the dollar to weaken across the board as a way to ameliorate global imbalances without one country or region having to take a disproportionate share of the pain ... "There is this idea of burden sharing, that some sort of silent accord has been done," he said. "If the decision is not to name China and the dollar/renminbi starts trading below Rmb8, then some sort of agreement may have been made behind the scenes. If we see 7 as the big number [i.e. the Rmb trading below 8] the market will catch fire."

If all this talk of possible dollar crisis, carry trades, leverage and secret deals seems too far-fetched, consider the potential size of the problem. Morgan Stanley's chief Asian economist, Andy Xie, tossed out this number link: "The global asset overvaluation (property, stocks, bonds, antiques, arts, gold, etc.) to GDP ratio is probably 50% above its norm, which puts this bubble at around US$20 trillion, by far the biggest to date in absolute and relative terms."

Marginal Record Highs in a Secular Bear Market?

In my intro I noted the seeming disparity of gold making highs along with record highs in the MSCI world equity index, when compared with gold's record highs in 1980 during a long secular bear equity market. But what if the new equity record is simply a rally in another secular bear market that began in 2000? Recent articles on volatility and valuation by serious analysts would seem to support that view, including two at PrudentBear by Easterling and Solow and Kitces.

Not Just Commentators, Nations Becoming Increasingly Concerned about Dollar

Of course it's one thing if just the "usual suspects" commentators seem concerned. But real nations in the real world also seem to be getting increasingly agitated.

Martin Wolf, the FT's main economics columnist, wrote on May 10: "Last week, I had the pleasure of moderating a governors' seminar on global payments imbalances at the annual meeting of the Asian Development Bank in Hyderabad. The discussion made even clearer than before how far the irresistible force of US desire for exchange-rate movement - well expressed by US Treasury undersecretary Timothy Adams - meets the immoveable object of Asian resistance. As a result, I fear, the chances of a row even worse than the one accompanying the end of the Bretton Woods exchange-rate system in the early 1970s grow ever bigger."

Commenting on the same ADB conference, Andy Mukherjee of Bloomberg wrote link: "Li Yong, China's deputy finance minister, said he had heard a "rumor" that the U.S. dollar was headed for a 25 percent drop. If the gossip was true, the consequences would be "shocking," he said. Li's comment, which he made at a discussion on global financial imbalances last week at the annual meeting of the Asian Development Bank in the Indian city of Hyderabad, was aimed directly at fellow panelist Tim Adams, the under secretary of international affairs at the Treasury Department."

Asian Currency Unit (ACU) Initiative of Asean +3 and ADB

This article then goes on to talk about a revival of interest in an Asian Currency Unit, ACU, which will be studied by Asean + 3 (China, Japan, S. Korea).

"Asia may be getting ready to fix its currencies to a local anchor, dumping the region's unofficial dollar peg. Even as they continue to pile up U.S. debt in their foreign- exchange reserves to keep their currencies stable against the dollar, Asian nations, China among them, are preparing for a scenario where the dollar does indeed collapse under the weight of a record U.S. current-account deficit." Also see link.

At this time I don't put too much weight on the ACU initiative for various reasons, one being the jockeying between Japan and China for regional leadership (India is currently left out of the ACU study), another being the many years, even decades, for such a project compared with a possible impending crisis link and link. But the effort at least is indicative of increased concern, as more practically was a pledge to enhance the Chiang Mai Initiative of Central Bank swaps and work on the development of the Asian Bond Market Initiative link.

According to a WSJ article, Adams of the U.S. Treasury said "I worry about mission creep in this institution," referring to the ADB. According to a NYT story link, "From the Americans there was an outcry [re the ACU], seeing it as a danger to the dollar," Volker Ducklau, the Asian Development Bank's executive director for Germany and Britain, told Emerging Markets, a newsletter published during bank meetings ... "We don't oppose it,"' said Timothy D. Adams, the Treasury under secretary for international affairs. "I have no concerns about this issue.""

Btw, during the so-called "Asian Financial Crisis" of 1997-98, then Treasury Secretary Rubin and his deputy Summers shot down Japan's briefly tabled proposal for an Asian Monetary Fund.

(For those interested in discussions of Asian monetary/financial integration by leading academic international economists, in the next day or two I will post brief excerpts from four very recent papers in an appendix to this article on my blog link.)

Weakened U.S. Leaders a Liability if Dollar Unravels

While a potential dollar crisis may be slowly building, with the U.S. deeply in debt to foreign creditors, Bush's rating and the standing of the U.S. abroad at very low levels (see new book based on Pew Research Center polls link), the actions of the Bush administration do not appear to be helping global confidence.

In particular, Cheney's recent negative remarks about Russia has not only brought a response from Putin, whose co-operation, along with that of China, is critical on Iran, but probably got China's attention also, especially since the leading Democrats are also trying to outdo Cheney on Iran.

China watched as Russia collapsed during its free market "shock therapy" in the 1990s; then as the Asian "tigers" were forced by the U.S. Treasury to submit to IMF austerity; and finally as Putin played ball with Bush following 9/11, with his reward being U.S.-funded "color revolutions" and NATO on his borders.

What lessons do you think China has drawn from all this? China has immense internal development issues that it must focus on, and it needs economic and geopolitical stability to do so. It prefers to take a low-key role in foreign affairs, while focusing on trade, resource and other deals. I mentioned in my April 20 post increased activity in The Shanghai Cooperation Organization of China, Russia and others link.

But at Least the Wealthy Get Their Investment Tax Cuts Extended

The Republicans in the Senate just passed today an extension of the large tax cuts for "investors," which often seems to be all that really matters to the Bush administration, even though these tax cuts have not produced the promised strong corporate investment, which has been sub-par in this business cycle.

Correction: In my 5/1 article: "The IMF's April "World Economic Outlook" raised its global growth forecast for 2006 0.6% to 4.9%, which would be the fourth straight year above 4%," rather than 0.5% to 4.8%, my apology.