"Everything depends on proper listening. Of ten people who listen to the same speech or story, each person may well understand it differently; perhaps only one of them will understand it correctly." The Fed's June 29th communiqué on monetary policy was the most anxiously awaited decision this year. And when the dust had settled, the zig-zag Fed fooled traders who bet on a half-point rate hike, and pleased traders who expected a pause and a peak in the fed funds rate.

The Fed's June 29th communiqué was riddled with ambiguity about the future direction of US interest rates, and perhaps the only thing that everyone understands correctly, is that Fed chief Ben Bernanke zig-zagged from its hawkish rhetoric of June 5th. The Fed did leave itself some room for maneuver for hiking rates further, but the growing consensus is the Fed is going on vacation this summer.

At a time when the US capital markets require $3.2 billion every business day to cover the country's external deficits, foreign currency traders who bought the US dollar since Bernanke's hawkish outburst on June 5th, wanted to hear Captain James T. Kirk, preparing his crew for an epic battle against the global inflation dragon. Instead, what traders heard on June 29th, was a two-handed Princeton economist, whose tough rhetoric about fighting inflation, had come down several notches from just 24-days earlier.

One the one hand, "Moderation in the growth of aggregate demand, should help to limit inflation pressures over time. Ongoing productivity gains have held down the rise in unit labor costs, and inflation expectations remain contained." However, on the other hand, "the high levels of resource utilization and prices of energy and other commodities have the potential to sustain inflation pressures," the Fed said.

The June 29th propaganda that "Inflation expectations remained contained," stands in sharp contrast to Bernanke's tough rhetoric on June 5th. The Fed "must continue to resist any tendency for increases in energy and commodity prices to become permanently embedded in core inflation. These are unwelcome developments. The medium term outlook for inflation will receive particular scrutiny. Possible future increases in these prices remain a risk to the inflation outlook," Bernanke said.

Bernanke's balancing act pleased everyone except short sellers betting on a tougher Fed. The Dow Jones Industrials soared 217 points in a knee jerk reaction, its best day in two years, and Treasury note prices rebounded about 1% on short-covering. Faced with a choice of defending the US dollar or defending US home prices, Bernanke dropped the greenback, catapulting gold 7% higher or $40 per ounce, silver soaring 10% or $1 per ounce, and crude oil jumping $2 per to $74 per barrel.

But "Helicopter" Ben Bernanke's reputation as a super-dove on monetary policy, has been impacting the global money markets since his nomination to lead the Fed on October 24th. Since then, the gold market in US$ terms has advanced by 33% to roughly $620 per ounce, while the US Treasury's 10-year note yield has climbed roughly 70 basis points to 5.15%, a four year high.

On May 1st, Bernanke confided to CNBC's Maria Bartiromo, that "it's worrisome that people would look at me as dovish and not necessarily an aggressive inflation-fighter". To shed his dovish feathers and appear more like a wise old owl, Bernanke authorized three quarter-point rate hikes to 5.25% under his watch. But dusting off his dovish reputation won't be so easy, as evidenced by last week's plunge in the US dollar, and surging commodity and gold prices, after Ben's zig-zag on June 29th.

Bernanke's hawkish outburst on June 5th, declaring all-out war against inflation, hammered the Chicago Eurodollar futures contracts to new contract lows. The only question was whether the Fed would go for a half-point rate hike on June 29th, or hint at a second quarter-point hike on August 8th. But now, a second quarter-point rate hike seems remote, as the finely balanced Fed statement of June 29th, suggests that US central bankers could go on extended vacation this summer.

The American public has turned against the Fed's 2-year campaign of interest-rate increases, concerned about rising mortgage payments, and deflating home prices. A Bloomberg/LA Times poll conducted June 24th to June 27th, showed by a 65% to 22% margin, Americans oppose another rate increase by the Fed. High home prices allow US households to keep on spending and not saving. The US personal saving rate, as a percentage of disposable income, slipped to a negative 1.7% in May.

The Fed is not interested in knocking US home prices sharply lower. Instead, it simply seeks to smooth out prices increases, following the blueprints of the Bank of England's "asset targeting" model. The betting is the Bernanke Fed will follow the politically correct course and pause its rate hike campaign on August 8th, to survey the results of the past three rate hikes on second quarter US growth.

"There is, after all, a time lag between monetary policy actions and their ultimate effect on inflation. That is, even though the recently reported inflation numbers have been edging upward, I think that the current 5% level of the federal funds rate is near a point that is consistent with a gradual improvement in the inflation outlook," said Cleveland Fed chief Sandra Pianalto on June 12th.

Bank of Japan to lift overnight loan rate, First in Six years

The Bernanke Fed is sub-contracting the job of fighting inflation to the other two big-central banks, the Bank of Japan and the European Central Bank. Other mid-tier central banks around the globe are also on course to raise rates this year, and the Bank of China, and Bank of India, the largest emerging economies with explosive money supply growth, are vowing to drain liquidity in their local markets.

A pause in the Fed's rate hike campaign in August comes at a critical time when the Bank of Japan is laying the ground work for a quarter-point rate hike to 0.25% on July 14th. The BOJ is set to raise rates for the first time in six years as the Japanese economy is posting 57 months of solid growth, and is finally pulling out of deflation, with core consumer prices rising for seven straight months through May.

"Monetary policy decisions should be made early, and changes should be made in small increments. But at the same time, it should be done in a gradual manner. Changing interest rates will prevent an overheating in the economy, minimize swings in economic cycles, and lead to a long-lasting expansion, said BOJ chief Toshihiko Fukui told the National Press Club on June 20th.

Foreign currency traders knocked the dollar 2-yen lower to 114.50-yen, after the Fed's zig-zagged and signaled it was close to the end of its rope of raising rates. The upcoming week's main event will be US non-farm payrolls data for June, due on July 7th. Also, traders want to see if the BoJ has enough independence to buck the ruling LDP party, which wants rates kept at zero percent.

Japan's government has 774 trillion yen ($6.7 billion) of outstanding debt, or 150% of its GDP, and wants to avoid paying higher interest rates. "Monetary policy is up to the BoJ, but the bank needs to continue working as one with the government to insure that the economy will not go back into deflation," said LDP Chief Cabinet Secretary Shinzo Abe on July 3rd. "The BOJ needs to continue zero interest rates for the time being to support the economy," and to keep the yen weak.

Japanese Economics Minister Kaoru Yosano told the BOJ on July 3rd, to keep the overnight loan rate at zero percent. "Looking at growth data and other economic indicators, it's accurate to say that conditions are not in place for an end to abnormal monetary policy, and that they are just starting to fall into place," he said.

Japan's Nikkei rebounded 10% from a panic bottom low of 14,000 on June 13th, to above 15,500, on ideas the Fed is done raising rates for now. Meanwhile, Japan's jobless rate fell to 4.0% in May, an eight-year low, and consumer core prices were 0.6% higher from a year earlier, reinforcing expectations the BoJ will raise interest rates on July 14th. The number of salaried Japanese employees rose above 55 million for the first time ever last month.

The recent turmoil in the Nikkei-225, which sliced off $864 billion of market value in four weeks, won't deter the BOJ from hiking rates. "Central banks in three major industrial nations have clearly changed course on monetary policy. As the markets realize this, it is natural for traders to be more cautious. There is no indication that falls in share prices have affected the real economy. Recent falls in share prices are within reasonable adjustments to earlier rises that had been prompted by loose monetary conditions," said BOJ chief Fukui on June 20th.

Even under heavy LDP pressure to keep rates at zero percent, the BOJ is still expected to move rates gradually higher, while keeping a close eye on the Nikkei-225 and dollar/ yen exchange rate. "Movements in financial markets could affect overall economic conditions by having an impact on corporate and consumer sentiment, so we need to carefully monitor them," Fukui added. (Tokyo would remain the cheapest source of global liquidity and continue to fuel asset inflation).

Bank of Korea meets on July 7th to discuss Rate hike

Across the Sea of Japan, traders are waiting on the Bank of Korea's July 7th policy meeting, amid speculation that the central bank will authorize another quarter-point rate hike to 4.50%. The BOK shocked the markets on June 8th, and raised its overnight call rate target by a quarter-point to 4.25%, the fourth rise since October. Bank of Korea Governor Lee Seong-tae explained, "The BoK views the economy as continuing to exhibit upward momentum, with exports, private consumption and capital investment all growing."

"Although a strong won and a fall in farm product prices have helped contain inflation, oil prices will likely remain firm and with the recovery in domestic demand lasting more than a year, inflation pressure will grow. We will have to keep watching the trend in real estate prices because they continue to increase despite various efforts by the government to curb them," BoK chief Lee said.

South Korean exports in June jumped to a record $28.27 billion in June, or 19.2% higher from a year earlier, led by increased shipments of flat screens and ships. Imports rose 22.1% in June from a year earlier to $26 billion, thus generating a trade surplus of $2.28 billion, just below a $2.42 billion surplus a year earlier.

BoK chief Lee Seong-tae indicated on June 12th, that the central bank will tighten its monetary policy again to absorb liquidity in the market. "While effectively coping with economic conditions, we are going to run our monetary policy in a way to preemptively react to inflationary pressure," he said. South Korean consumer prices rose 2.6% in June from a year earlier, and the annual core inflation rate of 2.2% was its highest since hitting 2.3% in June 2005.

Following the Fed's zig zag on June 29th, the US dollar plunged 18-won to 944.5 Korean won on July 3rd. Earlier, the dollar has staged a rally from a eight-year low of 925-won, on expectations the Fed would carry the fed funds rate to 5.50 percent. However, another BOK rate hike to 4.50% this summer, would narrow the interest rate gap with the US$, and make the Korean won an attractive Asian alternative.

The Korean won is tracking the Japanese yen /US$ exchange rate, which makes it easier for the BOK to hike its overnight loan rate, without hurting the competitive position of Korean exporters against their Japanese rivals. Beijing allowed the dollar to fall below 8-yuan last week, amid signs of a tighter Chinese monetary policy, and forward traders in Hong Kong, expect the dollar to fall to 7.71 yuan next year.

European Central Bank could surprise with July 6th rate hike

The ECB has raised rates 25 basis points during the last month of each quarter since December 2005, to 2.75%, and is signaling a tighter policy this year. "All the recent data indicate that risks to price stability are on the upside and have increased. We have to look at them next time and see whether we have to move sooner rather than later," said Greece's central banker Nicholas Garganas on June 27th.

"Should the need be for a more aggressive interest-rate adjustment, there is nothing to stop us from taking that decision. I would not rule out a higher adjustment to rates than 25 basis points, nor a faster pace of rate increases than once per quarter," the ECB's Garangas added.

Euro-zone interest rates do not suit the real economy and must rise further, said Bundesbank chief Axel Weber on June 30th. "We have to normalize monetary policy, this no longer fits with the real economy, and normalization is necessary to rein in liquidity dynamics. Markets have understood that the ECB will act when necessary, only under this condition can we anchor inflation expectations."

In his final confession as the ECB chief economist, Otmar Issing admitted on May 28th, that, "very expansive monetary policies led to a strong increase in liquidity globally and in the Euro area. The high liquidity contains an inflationary potential." Issing confessed after the Dow Jones AIG commodity index doubled from its 2001 low, and leaves the ECB far behind the commodity inflation curve.

That opens up the possibility of a surprise ECB quarter-point rate hike on July 6th to 3.00%. Private lending in the Euro zone hit a record high of 11.4% YoY in May, raising pressure for higher interest rates. Euro money growth also kept up its healthy pace, with M3 expanding at an 8.9% year-over-year rate, its highest in just over three years and up from 8.7% in April. Super easy money in Europe, in turn, fuels speculation in commodities and contributes to global inflation.

The ECB is not stuck in a fixed pattern of interest rate rises and a quick change in policy is always an option, warned Luxembourg's central banker Yves Mersch on June 28th. "Vigilance for the Euro system requires keeping all options open, including a quick change in policy of the Euro system if warranted by new incoming information. There is no pattern of historical monetary policy decisions that would simply be repeated mechanically or extrapolated into the future," he warned.

The tough ECB jawboning helped to put a floor under the Euro at $1.25, before the Fed's zig-zag on June 29th launched the Euro towards $.128. Clearly, the ECB is lingering far behind the monetary inflation curve, and could decide to move faster or more aggressively in lifting its repo rate this summer, while the Bernanke Fed goes on vacation, and watches the US Dollar get zapped.

The United Arab Emirates is sticking with plans to convert up to 10% of its $23 billion in foreign currency reserves into Euros. Central bank chief Sultan Nasser al-Suweidi said on July 2nd, the bank could also convert up to 10% of its reserves into gold. "I don't think it's appropriate to buy gold now, it's too expensive. The appropriate time might come very soon. We could go up to 10%," he said.

The central bank controls only part of the foreign exchange reserves of the UAE, an oil-exporting federation of seven emirates. Other major holders include the investment arms of the emirates' governments. Suweidi said the US dollar continued to suffer from pressure due to its twin budget and trade deficits, and the Euro was an attractive currency, because the interest rate level in the Euro has gone up.

Swiss National Bank Tracking higher ECB Rates

The Swiss National Bank will hike interest rates again, if the Swiss economy keeps growing at its above average pace. "If the economic situation continues to develop favorably, further corrections to the level of our benchmark rates will be needed," SNB Chairman Jean-Pierre Roth said on June 20th. "Despite our latest correction, Swiss monetary policy is still not a hurdle for the economy."

The SNB raised its official interest rates by 25 basis points on June 15th, aiming for 1.5%, the mid-point of a 1.0% to 2.0%, 3-month Libor target band. Swiss factory orders soared 15.5% in the first quarter, and Switzerland is enjoying one of the strongest first-quarter growth rates in Europe. Swiss economic output rose 0.9% in the first quarter of 2006, in line with a 3.5% annual expansion rate. The Swiss economy rose just 1.9% last year.

The Swiss jobless rate dipped to 3.3% in May, from 3.5% in April. Unemployment should settle at 3% by December, said SNB chief Roth. But signs of inflation are picking up amid higher capacity utilization. Swiss producer prices rose 2.4% in May from a year earlier, while import prices were 3.7% higher. Roth estimated the country's potential output growth rate, or the maximum speed at which an economy can grow without stoking inflation, at a mere 1.5 percent.

The SNB usually coordinates its monetary policy with the ECB, in order to maintain a stable Euro /Swiss franc exchange rate. Exports make-up about half of Switzerland's economy and two-thirds of its exports are sold to the European Union. Both ECB and SNB lending rates are still hovering near historic lows, providing a cheap source of financing worldwide for hedge fund traders and corporate takeover artists.

The SNB is expected to continue lifting its Libor rate target by 25 basis points at each of its next two meetings, in September and December to 2.00%, and extending into 2007 to match the ECB. That could lift the Swiss franc against the dollar as the US rate rise cycle ends. Unlike other major central banks, the SNB has kept a relatively tight rein on its M3 money supply, expanding at 3.5% annualized rate in May, and could slow towards 1-2% growth as the SNB tightens liquidity further.

SNB vice deputy Niklaus Blattner hinted on June 15th, that the sell-off in the Swiss Market Index won't deter further rate hikes. "We've seen a rapid increase in the last three years in equity markets, which, as we pointed out, couldn't be explained easily from fundamental factors. It's plausible that one day there should be a correction, but that does not mean there should be a fundamental explanation," he added.

South African rand rebounds from 2-½ year low on higher Gold

A broad sell-off across emerging markets, a sharp correction in gold prices, and worries over South Africa's widening current account deficit, all conspired to hammer South Africa's rand to a 2-½ year low of 13.30 US-cents last month. Yields on South Africa's benchmark 10-year bond soared 140 basis points to as high as 8.80%, as the plunging rand generates inflation pressures in the local economy.

South Africa is the world's biggest producer of gold, platinum, and diamonds, and the rand's movements against the US dollar are often influenced by the direction of gold and platinum. In turn, South African miner profits hinge on the metal price and the rand /US$ exchange rate. South Africa's has enormous gold ore reserves, estimated at 40,000 tons, and one of the greatest sources of gold in the world.

The platinum deposits that stretch north of Johannesburg, account for 75% of the world's known reserves, and are enough to last 350-years at current production rates. Mining only accounts for 6% of South Africa's GDP, compared with 16% for manufacturing and 19.5% for finance, real estate and business services. Nevertheless, gold and platinum together account for roughly 25% of South Africa's exports, so they're important for the balance of payments.

South Africa is the world's largest gold miner, and is more exposed than any other country to slumps in the gold price because its deep level mines are the highest cost producers in the world. However, with gold rebounding 10% above its climactic low near $560 /oz, the rand is bounced back into favor, changing hands at 14 US-cents, but still finding resistance at 7-rand per US$.

The rand is one of the most volatile currencies in the world, with average daily trade volume climbing from $3.8 billion in the first quarter of 1998 to $13.8 billion in the third quarter of 2005. The problem is that more than half of the daily trade in the rand takes place offshore and is often driven by foreign portfolio and speculative flows. Japanese investors were large buyers of SA rand bonds last year, and were unwinding the "yen carry" trade as the BOJ tightens liquidity at home.

US Dollar is chronically weak despite Fed rate hikes

As the US Federal Reserve appears to be near the end of its 2-year rate hike campaign, foreign banks are starting to hike their rates, thus making the dollar less attractive. At the same time, the massive US trade deficit channels a huge outflow of dollars to other countries, as well as the need to finance the ever-bigger US deficit. Last year, the US trade deficit in goods and services hit a record $726 billion, as US imports far exceeded exports. The gap reached 6.4% of GDP.

Financing the current US trade deficit requires higher US interest rates. Most of that money comes from foreign central banks, which own large amounts of dollars. Recently however, the central banks of Sweden, Finland, Russia, and the UAE have said they will diversify their FX reserve holdings and reduce their US dollars. Behind the shift may be concern that the dollar will be devalued, making their US bond holdings worth less. Higher Treasury note yields are starting to reflect this risk.

Countries around the world should gradually rely less on the US dollar for trade and their foreign exchange reserves, said Wu Xiaoling, deputy governor of the People's Bank of China on June 27th. "Internationally speaking, the situation of over-reliance on a certain country's currency for international trade, settlements and reserve assets should be gradually changed," Wu said.

While the Fed has restored the fed funds rate to 5.25%, a five year high, the US dollar index remains 24% below it levels of 2001. What has unfolded over the past two years, is the US Treasury forced to offer higher interest rates to foreigners, to prevent the US dollar from falling under its own weight.

The Fed's June 29th zig zag on interest rates is fraught with many risks, such as tilting the balance in favor of a speculative attack against the US dollar, which could invite higher import inflation, or foreign central bank diversification into other currencies and gold. US import prices rose 1.6% in May, and 8.3% higher from a year earlier, far above the 5.8% pace notched in the 12 months to April. Oil import prices rose 5.2% in May and are up 45.7% over the previous 12 months.

Because exchange traded commodities are mostly denominated in US dollars, the Federal Reserve has a special role to play to defend the US dollar, and prevent global commodity inflation from spreading into producer prices. Gold traders have known for a long-time, that the hard dollars and cents flowing through the commodities markets, are a more reliable indicator of real time inflation, rather than inflation statistics fashioned by government apparatchniks.

The biggest threat to the US$ is the possibility that foreign central banks will dump the greenback. Beijing has been gradually diversifying away from US dollar assets in its $925 billion of foreign exchange reserves, the world's largest, but fears of a collapse in the US currency against the yuan, prevents it from making any dramatic shift. Japan is the second largest holder of the US$, and has reduced its holdings of US Treasuries by $50 billion since April 2004.

Yu Yongding, and adviser to the Chinese central bank warned on December 30th, 2005, that the Federal Reserve might stop raising interest rates in 2006 and start guiding the dollar downward, putting upward pressure on the yuan. "More seriously, China's economy would take a big hit if the US dollar weakened sharply due to such factors as a bursting of the US property bubble. The loss for China's foreign exchange reserves would be extremely serious."

Fed Zig-Zag Catapults Gold above $600 per ounce

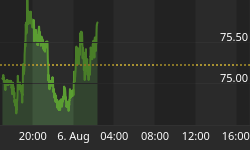

Metals, energy, grains and soft commodities rallied strongly after the Fed's zig-zag on June 29th, laughing at the Fed's observation that "inflation expectations remain contained". Copper surged almost 4% in London and 2% in New York in early trade, after a sizzling US GDP revision to 5.6% growth in the first quarter. Gold sprinted $40 per ounce higher to $623 /oz in London on Jly 23rd, to regain its old footing above $600 an ounce. Silver surged almost $1 per ounce to $11.27 /oz.

The Bernanke Fed is either out of sync with market psychology, or prefers to be reactive, rather than pre-emptive in confronting inflation. But the sophisticated bond and gold vigilantes are not going to be duped by the Fed's brainwashing about "contained inflation expectations," and instead are closely tracking the direction of the global stock markets, for clues about economic growth rates and inflation pressures in the world economy.

Maybe the Fed is not too concerned about a weak US dollar, because the Euro and British pound are under the supervision of inflationist central banks. For instance, the Euro M3 money supply is exploding at an 8.9% annualized rate, while the UK's M4 money supply is 11.8% higher from a year ago. It's only a matter of time until Japan's ministry of finance starts to threaten intervention on behalf of the US dollar, and a half-percent BOJ overnight loan rate would still be abnormally low.

Foreign currency trading is often likened to a reverse beauty contest, where the best currency to own is the least ugly. But the alternative to inflated paper currency is glittering gold, whose supply cannot be manufactured by abusive central bankers. But gold is widely owned by investors around the globe, and big supplies can hit the market at a moment's notice, such as witnessed from 5/11 until June 13th.

However, Yu Yongding, the chief economist at the Chinese central bank said on June 1st, that Beijing should use its $925 billion of foreign-currency reserves, the world's largest, to buy gold and crude oil as a hedge to guard against the risk of a sudden drop in the US dollar. Beijing has only 1% of its reserves in gold, with more than two-thirds of its reserves invested in depreciating US Treasuries.

"China has more than enough foreign-exchange reserves. We don't want to cause dramatic fluctuations in the foreign-exchange and securities markets. But China needs to invest the reserves to seek higher returns and to avoid losses in case of a big depreciation in the US dollar. We need to use some of the reserves to buy other assets such as gold and strategic resources such as oil," said Yongding.

"Commodity Super Cycle" led by Crude Oil

With the zig-zag Bernanke Fed on vacation this summer, the "Commodity Super Cycle" can move higher with less resistance, led by silver, platinum, copper, zinc, and crude oil. While commodities are very volatile, tight supplies for base metals, and geo-political tensions in the Middle East, are lending strong demand. Central bankers can only keep a lid on the "Commodity Super Cycle" by raising their interest rates high enough to knock global stock markets to new low ground.

Higher crude oil prices are a nightmare for G-10 central bankers, because they trigger secondary knock-on inflation effects in oil importing nations. World oil demand should soar 37% from this year's almost 86 million barrels per day to 118 million bpd by 2030, the US government's top energy forecasting agency predicted on June 20th. The United States, China and India together will account for half of the projected increase in world oil use by 2030.

Also supporting oil prices is Iran's threat to unleash the oil weapon in a dispute over its nuclear weapons program. "If the country's interests are attacked, we will use all our capabilities, and oil is one of them," said Iranian Oil Minister Kazem Vaziri-Hamaneh. "The world needs energy and understands the effect on the market of oil sanctions against Iran, and no-one will make such an unreasonable decision," predicting sanctions against Iran could push crude up to $100 dollars a barrel.

In a letter to Rep Brad Sherman on March 21st, Fed chief "zig-zag" Bernanke said "Although US trade deficits cannot continue to widen forever, these deficits need not engender a precipitous decline in the dollar, nor should such a decline, were it to occur, necessarily disrupt financial markets, production or employment." Since then, two Fed rate hikes have put the global stock and commodities markets on a wild roller-coaster ride, but the US dollar remains chronically weak.

Yet in Chicago, despite widespread expectation the Fed will take a vacation this summer, fed funds futures traders are confidently predicting the US central bank will eventually hike its overnight loan rate to 5.50% by year's end. But timing is everything, and a Fed zig-zag in August, might allow the inflation genie to escape from its bottle again, confirming the suspicions of hawkish Chicago futures traders.

To read our analysis, forecasts, and inter-market technical charts for the CRB index, global interest rates, major global stock markets, and their underlying US-listed ETF's, foreign exchange rates, gold, copper, crude oil and other commodity markets, Subscribe to the Global Money Trends magazine. Please click on the hyperlink below to place an order now. http://www.sirchartsalot.com/newsletters.php

This article may be re-printed with links to www.sirchartsalot.com.