The week just ended was the most mentally challenging and draining investment and trading exercise in recent memory leaving Yours' Truly with a feeling of being out of sync with the majority. Long gold stocks/short the Dow, my investment stance (with other diversification and defensive measures built-in), did not work out so well. As for trading, the results were spotty. Fortunately, this is all short-term noise and this past week did serve a purpose; it sharpened the picture of the current macroeconomic landscape.

In recent articles and on the blog http://biiwii.blogspot.com, I have targeted a 4.6% to 4.8% range for the US Treasury 10 year yield (almost there). I have also chronicled the Fed's desperate situation and the gamesmanship employed to get the players aligned properly on the field. Anything more than a cursory look behind the curtain shows a Fed speaking out of every side of its mouth; Richard Fisher's recent admonishment on inflation was particularly notable. This coming after the Fed had totally wimped out (in my opinion - I thought Ben Bernanke might become his "own man" by hiking against the market's wishes. See Quickie II) by pausing at the last meeting. These guys would be on the verge of losing control if they did not have massive legions of sheep eating those little food-like pellets right out of their hand. Of course I am talking about the bond market; former inflation vigilantes and current chasers of return at all cost. They are lapping up the Fed as inflation fighter story just as we speculators and investors who prefer dealing in reality need them to. We need that counter-party; someone to hold the bag of bonds while the Fed regains its credibility in the short-term as an inflation-fighting force. Others who think for themselves will use this opportunity to position for the next big move in the inflation as economic driver system currently in place.

Which of course brings us to gold. The gold bugs have been drubbed, humiliated and forgotten. All that inflation hype is so early 2006, after all. This is the perfect situation if you step back a bit and let the picture develop. The commodity/China story bulls are getting cleaned out, which means some hedge funds and large momo specs are sweating (take a look at the series of higher highs that has been broken on the CRB per the chart posted on the blog on Thursday, 8/17) and doing what they do, namely, selling first and asking questions later. I have felt all along that first the Fed needs to get inflation expectations under control (check) and then we need a spin toward uncomfortable "disinflation" (a sanitized way of saying deflationary pressure that will challenge the grotesquely debt-levered economy) which comes later and serves as the reason for future inflationary policy. Gold rose with economically sensitive commodities and the stock market itself and did not do anything to distinguish itself for what it really is; a sound value asset in all modern fiat-based environments. What I did not foresee is Goldilox dancing on my head for the last week where the order of the day was "soft Fed and weak economic indicators?.......BUY STOCKS!". At least I did not foresee gold going in the opposite direction in the face of such silliness. By the end of the week I just laughed and said "dat's show biz".

Over the last week I got my first real feeling of being stomped on, chewed up and spit out as an investor in the precious metals complex. That's a good sign! The barbarous relic is no longer in lock-step with the stock market hyperbole machine. I was actually forced to question myself and my investment orientations for the first time in a long while. My answer, which may be much different from yours, is that gold nuggets are going to be shooting higher as if launched from sling shots. The Fed is in control, the bond market buys it and there is no inflation problem. It's perfect. If and when the counterparty realizes it has bought the long term debt of an entity that inflates money supply for a living, the fireworks could be amazing and gold could decouple itself from the vanilla commodity complex inflation trade that ran until recently.

Either the above scenario is in the works or perhaps illusions can sustain for longer than sound money advocates and market bears can hold out. In that obnoxious scenario the dollar gains traction, gold continues to decline with the commodity complex and a new era of deflationary pressure actually helps enough sectors that the stock market and US paper scale another bull market leg before they blow out. The US is a debt-for-consumption machine detached from all traditional concepts of productivity and economics after all. But even I, a fairly conservative guy with an American manufacturing business and a website that seeks to tell it like it is (gloomy stuff and all) have to admit that I harbor an affection for technology and all that it enables. What I mean is - and this will be like pouring acid into the bears' ears - I would not be hugely surprised to see a 1999 style New Economy echo bubble.

That is not the scenario my odds favor, however. More likely is the picture of a precious metals complex consolidating and leading up to a flat-out hysteria to erupt sometime well before the end of the decade, with another major up-leg in the offing on this Fed rate cycle, pending the current bond market games playing out of course. Without further delay, some charts that help illustrate the case for the relic:

Admittedly there would have been little likelihood of gold dropping while economically sensitive commodities rallied, so gold did nothing notable to this point in the context of a rising commodity tide in a sea of liquidity. Gold has dropped with the commodity complex during this adjustment period since a large amount of gold bulls were simply general inflation-story bulls; "if it's not the dollar, buy it!". It is now (meaning this general time period of months, not days) or never for gold to decouple from the commodity "plays", to get itself contrary to the stock market and to show the terror/war hedge label it gets stuck with as a red herring. This is about treasuries, the dollar and global fiat currencies. It is a time for focus, not hype.

Speaking of the dollar, here is the chart:

Here lies the crux of why the Fed has got to be feeling desperation. The yield spread has been jammed into inversion. Inflation has been whipped, the bond market says so. But if the Fed does not begin to ease in the face of declining long rates, there well could be a deflation issue on the horizon. People are beginning to look for that. This is all part of the unnatural cycle on which the modern economic system runs. The problem is, a strong(er) dollar is what the Fed needs at this point in the cycle, not the basket case pictured above. The dollar is the Fed's stock in trade; the paper note that reflects the Fed's credibility and global confidence in the institution. So, like gold, the dollar is at a critical juncture to say the least.

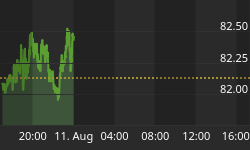

Finally, a closer look at the relic:

It's time has not yet come and it will not come until a majority of the public learns how to look beyond the headlines and hype and figures out that 1+1 does not equal 10 trillion. Until then, wise people attend to their debt situations, align investments with the major macroeconomic themes and live life to the fullest. While the market gyrations of the last week were decidedly unfavorable to my investment and trading stance, the major theme is still intact. For now the plan is to fade the galling display that took place on Wall Street last week (with always present risk management of course). It is more comfortable running with the herd, but long-term success if preferable to short-term comfort.