Moneyization: The global financial phenomenon of individuals and businesses moving their funds to monies in which they have the highest confidence, or money in which they have a higher store of faith.

Or, Process of Elimination Leads to Gold

Listening to the popular business media the past few years has been the equivalent of watching a test pattern, always same picture and of little value. A continuous stream of Street gurus have repeatedly offered up the same useless advice. Investors should continue buying technology and financial stocks. That the housing bubble might unwind in a painful matter was deemed to be total fantasy. Gold was, in their view, a ridiculous idea. For nine years this advice has been garbage, and the time has clearly arrived for investors to ignore these ideas. Facts are facts as the first graph shows.

Shown in that graph is the manifestation of the moneyization process. Investors have fled other forms of investments and their national moneys. They are seeking a haven for the enhancement and protection of their wealth and money. They found it in Gold, the only real money, rather than "paper" backed only by fantasies. Global investors have faith in Gold, not government paper.

Intel's intention to lay off of more than 10,000 employees is further confirmation of the end of the old technology investment theme. Dell had already been a strong indicator of the death throes of the old technology stocks. Impartial observers had already recognized this reality. Only fund managers, protected by the Wall Street framework, were in denial. Last Wednesday and Thursday that reality started to be acknowledged by about a 50-point collapse in the NASDAQ Composite Index. That market action spilled over into the Gold and Silver markets, creating an excellent chance to buy.

INTC's announcement means that one of the three investment themes of the Street is flawed. That leaves financial stocks and the housing bubble. Understanding the housing bubble will lead to the answer on financial stocks. Recently released data from the U.S. Office of Federal Housing Finance Enterprise Oversight(OFHFEO) provides some insight into the faltering trend in U.S. housing prices. OFHFEO was created to proved oversight of Fannie Mae, Freddie Mac, and the Federal Home Loan Banks.

In the second graph is plotted the quarterly rate of change annualized for the House Price Index(HPI) from OFHFEO. The HPI, in many ways, is superior to other house price data. Only problem with the series is that it is released just quarterly. This price data uses repeat transactions from Fannie Mae and Freddie Mac. A house must have been sold twice for the price data to be included in the series. This pricing information is more comparable to transaction-based data available for stocks than other measures.

Evidence of a bubble can be found in that graph. In a bubble, price appreciation increases unnaturally in the late stages. When a ball is tossed into the air, the momentum of the ball declines until the ball starts to fall. In a bubble a far different process develops. As the ball is thrown up, the ball starts rising faster and faster. In that graph the rate of price appreciation accelerated, as is the case in a bubble. Housing prices have been attempting to defy "economic gravity" and are now in the process of correcting that excess. A trend line has been added to highlight how the pricing environment has broken down.

Money is what makes prices in a market rise. For housing prices to rise, money must flow into the housing market. Absolutely nothing else, not location, not opinion, not under valuation, not migration, not any of the other reasons put forth will make housing prices rise unless money flows into the housing market. For money to flow into the housing market someone has to apply for a mortgage. Someone has to want a mortgage. The third graph portrays the recent experience of the mortgage market. Plotted in that graph is the index of weekly applications for mortgages to be used to purchase housing. Note that applications have broken below the previous lows. Less money is flowing into housing market, and housing prices are going lower, lower than anyone can imagine.

Who will benefit from these trends? Aside from Gold, clearly those firms involved in the foreclosure business will benefit. marketwatch.com reports that RealtyTrac is an online marketplace for foreclosures. According to the article by Nick Godt on 6 Sep 2006, the firm was recently ranked the 53rd fastest growing private company by Inc. magazine, with a growth rate over the past three years of 1158%. U.S. foreclosures, per the article, are up 25% from a year ago, and one in 425 U.S. households is in foreclosure. Remember that number! When foreclosures become a growth business, one should conclude that the housing market is entering a severely difficult period.

Who will be hurt by these trends, aside from those funds selling/shorting Gold and Silver this past week? Fourth graph gives some insight into the holders of the credit risk for U.S. housing debt. Note that this is holder of the credit risk, which may be different from the owner of a mortgage's cash flow. Biggest holder is Fannie Mae. Ultimately, the government may have to supervise a reorganization of this entity.

Banks have about $1.9 trillion dollars exposed to mortgage credit. For some time analysts and strategists have contended that the banks are in great shape, with good earnings and plenty of capital. Yes, such is the way it is when financial fragility is at a maximum. Financial fragility is the "calm before the storm." It describes a situation where financial institutions increase dramatically their exposure to the "hottest" and most profitable business. When the downturn comes, they find themselves with excessive exposure to the collapsing sector. Banks increased their exposure to housing credit risk in this period by almost $900 billion. Losses could possibly run $100-200 billion. Owning bank stocks is not wise.

The first category in the graph is ABS. That acronym stands for asset backed security. These are securities backed by mortgages that pass along the interest and principal payments to the investor. About $1.3 trillion dollars of privately issued mortgage backed securities were issued in 2001 to 2005. These securities are now owned by individuals directly, or indirectly through various mutual funds or other investment management structures. Quite simply this risk has been dumped on the public, probably with little understanding of the riskiness of such vehicles. Investors might be wise to shy away from mutual funds owning such vehicles.

Much discussion has begun on whether or not the housing industry is approaching a "buying opportunity." Such talk is premature and largely ignores the systemic nature of the problem. The massive housing finance system of the U.S. is only beginning to have its structural integrity attacked. With foreclosures likely to reach levels beyond anyone's guess, the ability of that system to provide financing for home purchases will be seriously constrained. If the fuel injection system on your car fails, it will not heal itself overnight in the garage.

The implosion of the housing bubble should benefit Gold investors. Two responses are likely to this massive economic problem, and both should push the value of Gold higher. First, the Federal Reserve will indeed panic and attempt to lower interest rates. Any attempt by the Federal Reserve to reverse the collapse will fail. Putting gasoline in the tank of a car with a broken fuel injection system will not make the car run. The same is true for the housing situation. As the financial system that connects monetary injections from the Federal Reserve to the housing industry will be in near total disrepair, this easing will be ineffective. The market response to this policy action will be felt on the foreign exchange markets where the dollar's value will fall. $Gold will move nicely higher in such an environment.

Second, we can expect foreign investors to become reluctant to purchase U.S. dollar-based debt. This action will put further pressure on the dollar's value. Something approaching $60 billion a month of dollars could be dumped on the foreign exchange markets. At some point foreign investors will begin to liquidate their holdings of U.S. debt. US$1,375 Gold will not be hard to reach in such an environment.

Recent market action is creating a short-term opportunity for investors within the context of a greater cycle that should carry US$Gold into four digit territory. INTC's announcement is confirmation of end of old technology stock investment theme. Housing is certainly no longer a safe investment. The dollar possesses only price risk. Real assets are what is left after the other choices have been eliminated. Gold is the most liquid of the real asset investment alternatives. Last week under panic selling from funds, Gold was pushed down to levels that should be flashing buy signals in the eyes of investors.

Silver, in the next chart, is helpful in understanding the underlying demand trends for precious metals as it is less vulnerable to mood swings of fund mis-managers. Many analysts remain bogged down with historical price patterns. Recognizing and becoming aware of the emerging structures is more important. In that graph of Silver prices, the new rising structure within the Silver market can be observed. Weak hands have sold. Underlying fundamental demand is continuing to emerge. Silver's positive technical structure should give encouragement to Gold investors.

The GDM, an index of Gold stocks on the Amex associated with the ETF GDX, is plotted in next chart. The question is simple. Does that pattern look like a top or a bottom? That pattern looks like a bottom, and investors in Gold stocks should not disturb their positions based on the panic of the past week. GDX, like Silver, is another indication that the recent turmoil in the Gold market should not cause panic reactions. Low prices are a chance to buy, in order to sell high later.

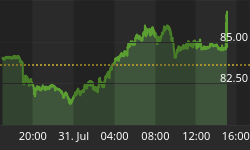

The final chart is on US$Gold. This market has been seriously ravaged by the buying and selling of short-term, panic driven fund mis-managers. However, Silver and GDM are both suggesting that this situation is going to be resolved in a positive manner. The panic selling of the past week is sending the short-term indicator into over sold territory which may lead to buy signal on intermediate indicator, shown in chart. Dollar-based investors, U.S. and Canadian, should be adding to holdings at these panic induced levels. UK investors should be buying Gold with the odds of a $2 pounds now approaching zero. Euro investors simply must decide if Gold is a good idea or a bad idea in a world facing an Iran with nuclear weapons.