For months we've been warning that precious metals would continue their price increases, but not too fast or else they would be brought back in line with more gradual long term trendlines. The multi-year charts we presented here last week show how far the metals could still fall and still preserve their bull market. But, due in part to the market-outperforming gains in both gold and silver for 2006, we said:

"From here then, we would expect metals to remain within a wide range near current levels, possibly with more immediate downside than up."

For at least a month now, we've been steadily articulating our bias against any cut in interest rates by the Federal Reserve and, if anything, toward eventual higher interest rates. This despite broad expectation of an '07 rate cut or two in both the stock and bond markets. This week, the markets continued to vindicate our outlook after stocks tumbled on Wednesday's FOMC minutes reinforced the Fed's hawkish stance even in the face of slowing growth and after bonds rallied back despite Friday's strong jobs numbers, indicating that a near-term interest rate cut is increasingly unlikely, though not so robust as to signal an actual rate hike. Last week we had said:

"The adequate, if not excess, liquidity evidenced by the equities markets, and now the ECB's M3 data, signal that only a dramatic tailspin into recession could possibly force the Fed to lower interest rates with the dollar under pressure as its recently seen. Of course this means that bond buyers looking for a rate cut next year are probably still too optimistic."

Most relevant for precious metals, though, was that stronger economic data and shrinking odds of an interest rate cut lifted pressure off the dollar and put it squarely on gold and silver. Combined with weakness in oil and base metals, dollar strength led to a precious metals selloff through recent support levels despite a strong opening to the week.

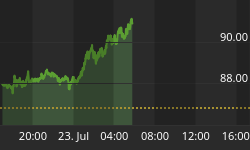

Last week's daily charts showed GLD and SLV closing the year at the top of nice upward runs and near resistance levels. After this week's decline, the weekly charts have both ETFs at possible support with closes near their 50-day moving averages. Both gold and silver, bounced off key psychological support levels at $600 and $12 before going into the close, at least suggesting a possible buying opportunity.

Our position continues to be that Wall Street, and indeed the entire globe, is flush with liquidity despite tougher reserve requirements in China, and that upside to the dollar is limited in this monetary environment. Inflation concerns, which tend to buoy metals, did not get the anticipated boost from the high payrolls data, but will remain a concern for the Fed, since it's more concerned with increases in wages and unemployment than with the price of gold or silver.

We also maintain that, glut of copper notwithstanding, the fundamental picture for precious metals and many base metals remains bullish. Though global growth may be slowing somewhat, development continues at an impressive rate in China and other countries. All of these factors will eventually slow the descent in precious metals and should keep the longterm bull market in tact. However, unless bulls from here are banking on stronger growth rather than greater liquidity, earnings and economic data could cause a recurrence of this week's trading theme and bring further damage to precious metals if they continue to indefinitely delay interest rate cuts. The increase of reserve requirements in China is a responsible move that may avoid a spectacular crash in that super-heated, fledgling capitalist economy, and could put the breaks on the recent dollar rally for at least the time being.

Tighter lending in China may skim off some of the froth in global manufacturing, but analysts claiming the decline in commodities could be a signal of a coming slowdown in the American economy are at best lazy and at worst completely clueless. First, this week's selloff in precious metals occurred after a significant bull run and was catalyzed by dollar strength on positive economic data. The loss of American manufacturing jobs is hardly bearish for metals, which are subject to global supply and demand, nor the decline in metals necessarily indicative of further manufacturing weakness. Second, the sharp decline in copper, at least, comes as global growth rates remain high and supply increased by new mining activity. If anything, cheaper commodities are a boon to American housing and auto manufacturing, the two sectors dragging most heavily on the U.S. economy! Clearly the exact opposite of what these misguided pundits are saying is true, but, if they persist in their folly, further strengthening of the U.S. economy may become another catalyst for metals and make them wise.

Perhaps more important though, this selloff reveals the double-edged sword of investor dollars which can quickly bid up metals or just as quickly fade them. Commodities are increasingly subject to investing trends as a result of new ETFs, futures funds, and other commodity-based investment vehicles and derivatives. For all of the above reasons, the sector is simply not perceived as the place for hot money at the moment. Commodities are fundamentally driven by economic conditions, but the exaggerated volatility of recent years is a function of large, frequently speculative, investment dollars. As earnings season begins next week, the health of the overall economy will continue to be the message sought in the data, a message that will dictate the direction of fast money, the dollar and precious metals.