Index Advisor 028

4/9/2007 8:31:02 AM

Recommended Trades:

Cover all short trades and go to cash.

Open Positions:

The market broke upward last week. This moved against our short positions.

In general, once we have entered a position, we will issue an alert to exit the position. We will note likely target areas for a trade, but we buy and sell on signals, rather than target areas. The same method applies to stops, as we don't use classical stops, but rather rely on the signals generated to reverse or exit our positions.

Symbol | Position | Entry | Current | Dollar | Percent |

DIA | Cash | $122.82 | $125.46 | -$2.64 | -2.11% |

IWM | Cash | $79.00 | $80.44 | -$1.44 | -1.8% |

QQQQ | Cash | $43.53 | $44.56 | -$1.03 | -2.4% |

SPY | Cash | $141.20 | $144.24 | -$3.04 | -2.2% |

Overview:

Breaking out...

The holiday shortened week was about better than expected economic numbers and relief from the release of the British sailors held hostage in Iraq. The market is breaking out of resistance and looks set to challenge six year highs.

Let's review economic reports and other events that transpired during the week.

Monday: The ISM report was issued at 10:00am EDT and resulted in a sell-off for a half hour. Following Friday's Chicago Purchasing Managers report, it was widely believed that it would come in stronger than the consensus expectation of 51.0. Instead, it came in at 50.9 (as expected) and the market reacted negatively before reconsidering. M&A news provided support for the market, after two M&A deals were announced worth more than $37B. A downside tone was also in place due to M&T Bank (NYSE:MBT) took down their Q1 guidance due to problems with Alt-A loans. Alt-A are the loans held by many regional banks that are between sub-prime and prime, in terms of credit worthiness.

Tuesday: Tuesday, three things of note were in focus. First, the price of oil was down about a dollar from Monday's close as it appeared that a diplomatic solution may be possible over Iran's capture of the 15 British sailors, and a possible start of a shooting war. Second, chain store sales last week rose by 4.9%, which indicates the U.S. consumer continues to shop. Finally, and the one most often posited for the rise in the market, was the report that the National Association of Realtors (NAR)'s pending home index rose 0.7%.

This means that inventories of existing homes may fall when the sales are completed in March and April. Existing home sales numbers for those months won't be reported until the end of April and May. The pending sales report is not widely covered, but is now being scrutinized due to concerns over sub-prime and Alt-A loans dragging the entire financial sector down with them.

Wednesday: Three events occurred Wednesday that influenced the market. Iran declared that they would release the fifteen British sailors they had taken hostage on Thursday. A Citigroup analyst raised the Q3 target for Microsoft. Finally, the economic reports were below expectations. The ISM Services Index came in at 52.4 versus an expected 54.7. That is the lowest level seen since 2003. Factory orders rose 1% versus an expected 1.9%.

The diplomatic solution to the Iranian hostage crisis allowed the price of oil to fall slightly, while the economic reports seem to have had little effect. Microsoft gained 2.2% today and since it is on all three major indexes, they all went up today.

Thursday: Initial jobless claims were reported at 321K for the week ending March 31st. This was just higher than the expected 320K.

Friday: Friday's economic reports included:

- Nonfarm Payrolls - 180K versus an expected gain of 135K. January and February were both revised higher by 16K.

- Unemployment Rate - dropped to 4.4% versus 4.6%.

- Hourly Earnings - grew 0.3% as expected

- Average Workweek - 33.9 hours versus an expected 33.8 hours. February was revised upward from 33.7 hours to 33.8 hours.

- Wholesale Inventories - grew 0.5% versus an expected 0.4%. Wholesale sales grew 1.2% leaving the year-over-year Inventory/Sales ratio at 1.15

- Consumer Credit - grew 3% versus an expected 5% growth rate

When taken together, the first four reports show a stronger employment picture than expected. There is a pattern of payrolls being revised upward for a month or two after the number has been reported. The average workweek is at a high and indicates a tight labor market. The unemployment rate echoes these concerns dropping even lower to a 4.4% rate. The biggest surprise was the 56K gain in construction employment following February's fall of 61K. Manufacturing showed its 9th month of consecutive loss of jobs.

Oil dropped for the week but is still above the $64 break-out range, and therefore is still above support. It closed the week at closing at $64.28, down about $1.50 from last week. Natural gas fell a few cents to close at $7.747.

We decided to add a special section to this weeks Index Advisor on a special topic:

Special Topic: Recession:

Most investment professionals accept the definition of a recession as "A period of general economic decline; specifically, a decline in Gross Domestic Product (GDP) for two or more consecutive quarters."

We are certainly not currently in a recession, and the Fed has predicted a slowing, but continually expanding economy. With the Q406 rate of GDP growth being reported at 2.5%, no economist would argue that the United States is currently experiencing a recession. With that said, many economists and market prognosticators argue that a recession is coming. Alan Greenspan, the former Chairman of the Fed, sent the markets into a tizzy when he suggested that there was a one in three chance that the US would enter a recession by late 2007.

If the economy is believe to be entering a recession or enters one, the stock market will react adversely, as the companies represented in it, will, as a whole, show negative growth. Negative growth lowers the valuation of the companies, and likely leads to falling profits. Of course, the companies can take steps to reduce costs, but this also adversely effects people as they are laid off, suppliers, as they are pressured to delay delivery of raw goods, services, etc. The market tends to react quite negatively to the "R" word.

With that said, the housing market is clearly in a recession. Prices are down as inventories of new and existing homes reach levels not seen for decades. There are worries that this could affect the overall economy more than the 1% to 1.5% drag it is already demonstrating. This is why the homebuilders, home improvement industry, and financial industry have been experiencing such difficulties.

Going one step further, we have seen bankruptcy proceedings and fire sale prices for other sub prime lenders as they are collapsing from the default rates on loans that they made and sold off to their bankers. Much of that paper is held by the large investment banks. There are also the Alt-A loans, which are sandwiched between sub prime and prime. Most of these are held by regional banks. There is a concern that the banks holding these loans could face crippling losses as more and more homeowners walk away from their homes and these loans.

What the professional investors and traders watch closely are signs of contagion or unexpected weakness in other areas of the economy. If the consumer slows their spending, this is a clear sign that sentiment has changed or the consumer is in some way getting squeezed. If banks begin reporting a drop in profits, and lowering their guidance for the year, this may be linked back to the mortgage concerns, etc.

Essentially, the professionals are watching for continued demand for consumer goods, continued growth in manufacturing and consumer services, and continued business investment. Without these, the economy will enter a recession.

We'll take a look at the an indicator that is put out monthly by the conference board. It is called the Composite Index of Leading Indicators and includes the following:

- Average weekly hours (manufacturing) - Adjustments to the working hours of existing employees are usually made in advance of new hires or layoffs, which is why the measure of average weekly hours is a leading indicator for changes in unemployment.

- Average weekly jobless claims for unemployment insurance - The conference board reverses the value of this component from positive to negative because a positive reading indicates a loss in jobs. The initial jobless-claims data is more sensitive to business conditions than other measures of unemployment, and as such leads the monthly unemployment data released by the Department of Labor.

- Manufacturer's new orders for consumer goods/materials - This component is considered a leading indicator because increases in new orders for consumer goods and materials usually mean positive changes in actual production.

- Vendor performance (slower deliveries diffusion index) - This component measures the time it takes to deliver orders to industrial companies. This is a leading indicators with slower deliveries suggesting an increase in manufacturing demand.

- Manufacturer's new orders for non-defense capital goods - As stated above, new orders lead the business cycle because increases in orders usually mean positive changes in actual production and perhaps rising demand. This measure is the producer's counterpart of new orders for consumer goods/materials component (#3).

- Building permits for new private housing units - Building permits mean future construction, and construction moves ahead of other types of production, making this a leading indicator.

- The Standard & Poor's 500 stock index - The S&P-500 is considered a leading indicator because changes in stock prices reflect investor's expectations for the future of the economy and interest rates.

- Money Supply (M2) - The money supply measures demand deposits, traveler's checks, savings deposits, currency, money market accounts and small-denomination time deposits. This is adjusted for inflation by the federal governments published deflator. An increase in M2 suggests an outlook for an increase in inflation.

- Interest rate spread (10-year Treasury vs. Federal Funds target) - The interest rate spread is often referred to as the yield curve. This came into focus in the last couple of years as the curve threatened to become inverted and then became inverted, with long term interest rates being lower than short term rates.

- Index of consumer expectations - This is the only component of the leading indicators that is based solely on expectations. It is a leading indicator and comes from the relatively new Michigan consumer survey.

The chart of the composite appears below:

You will note that is shows fourteen months of data. Many economist and market watchers look for three consecutive months of declines as a signal for a recession. Other economists use a cumulative signal below -1% over six months along with the three month cumulative decline to strengthen the signal. However, using all of the above, this has produced a false indication in 1995's soft landing, while correctly predicting the recessions in 1900 and 2001.

As additional input, it is important to note the breadth of the decline across all 10 inputs to the composite index. If we get a third consecutive monthly decline reported for February then many market watchers will scrutinize the breadth of declines. You can see the recent readings from those indicators below:

Do we think that the U.S. economy is headed for a recession? We hope not, but we don't have a crystal ball. We have been concerned about the housing industry problems being larger than expected, and that has, thus far, been proven out. We suggested early on that the mortgage industry was taking on too much risk in lending practices, and this too has come home to roost. We will continue to monitor the critical signs of economic slowdown for you, and provide an early warning should we see cause for even greater concern.

Let's return to our standard discussion of the markets...

Market Climate

Tuesday showed a marked turn in sentiment as Iran announced they would release the British sailors they had detained while a narrowly followed housing number provided investors with the belief that things may not be as bad as they thought in housing.

While the rise allowed a break above or to resistance for the major indexes, this was accomplished on light volume. The selling from late February has been on heavy volume, so that lost ground hasn't yet been made up.

A look at the daily chart for the Dow Industrials is represented by the Diamonds ETF (Amex:DIA).

Abbreviations and color key appears below:

Note the following order is Red, Yellow, Green, just like a stop light, so it might be a helpful mnemonic:

Thick Red line represents the 200-day simple Moving Average, (200DMA)

The yellow line represents the 50-day simple Moving Average, (50DMA)

The green line represents the 20-day simple Moving Average, (20DMA)

The light blue line represents the 3-day Moving Average, moved forward three days in time, (3x3MA)

The thick blue line indicates the exponential 13-day Moving Average (13DMA)

Bollinger Bands are abbreviated as BB. There is an upper and a lower Bollinger Band that varies in distance from a central moving average (shown as light red/pink) based on the volatility of stock price movements.

RSI stands for Relative Strength Index. It is an oscillator, which can be used to determine how overbought or oversold a stock may be.

The daily chart shows the DIAmonds shows they broke above the recent high and are currently at resistance. The all time high isn't too far above, so it is likely the bulls will push to challenge that level in the coming week as we approach earnings season.

The S&P 500 ETF, known as the Spyders (AMEX:SPY) is shown in the daily chart below:

The daily chart of the SPYders looks similar to the DIAmonds but the SPYders have not yet closed the open window. They are also above resistance and are likely to challenge their six-year high shortly.

The S&P 500 ETF, known as the Spyders (AMEX:SPY) is shown in the 15-minute chart below:

The 15-minute chart of the SPYders shows that volatility had diminished as the SPYders traded in a narrow range before breaking out on Thursday. They look set to use the 20-period moving average as a springboard to move higher on Monday's open.

This week's NASDAQ 100 ETF (QQQQ) Daily Chart is below:

The chart for the QQQQs shows the 50-day MA crossed below the 100-day moving average, just as price began its move upward. The 20-day moving average is set to cross the 50-day and 100-day moving averages late this week, if the market continues to move higher or trade sideways. This could likely lead to an acceleration to the upside.

We have been tracking the semiconductor index and it has bounced of the bottom of its uptrend channel and is moving higher. We will continue to monitor it and discuss it in terms of its influence on the NASDAQ.

This week's NASDAQ 100 ETF (QQQQ) 15-minute Chart is below:

The chart for the QQQQs shows a break out from around noon on Thursday. The QQQQs closed at the high for the day and were especially strong in the final minutes of trading. The tight trading range gave way to a broader range and the QQQQs are walking up the upper Bollinger Band.

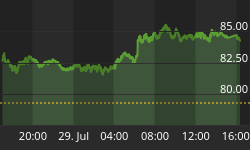

This week's Russell-2000 ETF (Amex:IWM) Daily Chart is below:

The chart for the IWMs shows they were weaker, last week, relative to the other major indexes. Could this be a move away from risk, even as the markets move higher and appear to be poised to challenge their highs?

The key resistance for the IWMs is around $81.20 which sets them up to challenge their highs a little more than a dollar higher than this level.

Conclusion:

With the resolution of some of the tension caused by Iran's detention of British sailors, and the resultant drop in the price of oil, the markets appear poised to challenge their highs. The housing morass seems to be looked at more favorably due to the pending home sales of existing homes released by the NAR. We are approaching earnings season which will become the focus for investors who are expecting continued growth, albeit not at the torrid double digit pace of the past fourteen quarters.

We expect the markets to make a further correction in the relatively immediate future, whether they are able to break above their February highs or not. There is unfinished business still. Of special note is the closure of many short positions. Without the short covering, there is little catalyst to move the markets higher at this time.

Stay tuned for more.

Regards and Good Trading,