"A corrective dollar rally, as short-lived as it might be, could become a hurdle for metals going forward ... When support finally kicks in, as it may have on Friday, there could be some correction and consolidation in metals." ~ Precious Points: Got Discipline?, April 14, 2007

Everywhere you turn, economists and commentators are talking up the benefit of the weak dollar - how it's good for exports, how it will boost the profit margins of multinational corporations. What you don't hear quite as much of is how it makes your cash savings worth less and less and how your wealth would be more than keeping pace with inflation if it was stored in metals.

Gold and silver have surged on a steep decline in the dollar index over recent weeks, but the last update warned that a relief rally might be due. In fact, the dollar did find an ounce of strength last week, causing the metals to briefly stumble. Core CPI was modest, but, even worse, this fed the lingering perception from two weeks ago that inflation in general is moderating. As a result, there was downward pressure on the long end of the yield curve, an overall decrease in TIPS spreads, and some recovery in the greenback.

But though traders might seize on the moment, the Federal Reserve is unlikely to have been soothed much by the single data set, especially considering the forces responsible for the mild inflation figures will probably dissipate by next month. What doesn't seen to be dissipating is the rate of increase in M2, expanding by an additional $18.7 billion last week alone.

Domestic liquidity is a concern for some, but the capital market is still showing no signs of a "credit crunch", even though banks are restricting their home mortgage lending. The balance has been made up in business loans, which is apparent in the drop in corporate paper issuance. Corporate bonds have the requirement of being spent on business purposes, and last week's corporate paper data were consistent with the anemic capital expenditure recently lamented by economic optimists. Instead of investing in new production capacity, companies have preferred to spend their cash on stock buybacks and dividends, probably because they still see weakness for the economy in the short term. The important fact for metals, though, is that domestic liquidity remains intact.

Globally, where economic growth is robust and profound, liquidity is also quite adequate despite the upward trend of interest rates in Europe, the U.K., and Japan, and now the expectation of rate hikes in China. In fact, whereas stock markets responded negatively in February to China's attempts to dampen the pace of its growth, they seem to have now come to the position always held by this update. A bubble-like collapse of China's economy is virtually inevitable if their growth is not managed responsibly. They have the positive example of their neighbors in Tokyo, who through strict regulations on banks, see low inflation even with very low lending rates. The Chinese seem committed to sustaining the viability of their economy, even if only for their own domestic political benefit. And, of course, a growing consumer class in China will only create new demand for all commodities, including precious metals.

Therefore, the long term outlook for metals remains bullish as the tide of liquidity stays high. But it also seems certain volatility will continue as the woes of the domestic housing market continue play out and the structural changes to China's economy are integrated into the global market. New money continues to flow into stock markets, even though economists expect consumers will draw liquidity from stocks as their home equity diminishes. February's shakedown clearly wasn't enough to kickstart new investment in real estate. Another correction, maybe not as sharp, but for longer, could actually mark the bottom for housing, and if it does occur, metals will probably not escape unscathed. In the meanwhile, rising interest rates abroad work to make rates in the U.S. more accommodative, weakening the dollar and seeming to virtually preclude the Fed from lowering interest rates.

Short term, metals will continue to benefit from economic optimism and strong corporate earnings. Essentially, metals are neither at support or resistance and, in the absence of significant economic data early in the week, will be subject to the mood of the markets. Despite a minor struggle last week, the trend continues to be up until it's not. Weaker consumer confidence and existing home data could be the start of that reversal unless earnings keep investors buying at last week's fevered pitch.

Two key pieces of economic data released late next week, GDP and PCE, could also be important factors. GDP is forecast to come in low, but the deflator could reasonably be expected to be cold given the recent data. Gold and silver are either nearing the apex of their respective rallies or are waiting to break out to new highs. The chart below shows gold at vulnerable technical target range and in need of a spike above $720 in order to challenge last Mays highs. Certainly a renewed decline in the dollar could be that catalyst.

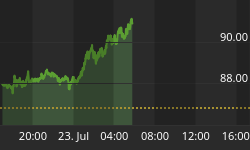

Chart by Dominick

Silver, though recently underperforming, could make back most of its lost ground on a good week. The RSI does not look exhausted yet, and silver closed with more net speculative long positions despite finishing lower for the week. Though earnings could easily overshadow the metals in the early part of the week, a slow creep upward could easily become a higher jumping-off point if the economic data and global events materialize favorably. A member in the forums has also noted the bullish rising triangle pattern in the silver chart, further indication that silver's break should be to the upside.

Metals have been sailing the seas of liquidity and all seas are subject to ups and downs. In 2006, metals jumped more than 30% in three months. After a steep correction they've fought their way back near those levels. Now, with investors inoculated against a falling dollar by all the talk about exports and multinationals, the dollar index could slide below 80 before anyone starts getting nervous again. And if the metals can hang on until the next round of inflation data proves that inflation is not gone, big waves can be on the horizon.