Is this a critical time in the bond market or are we simply back to where we were a few months ago before the recent madness? If it was temporary insanity, what caused it? Why is the dollar rising? Why have the Japanese sold more foreign bonds in the past few weeks than in the past few years? Who is buying those bonds? If the money supply is growing at breath-taking rates, why is gold languishing? If the economic data is so dismal then why are stocks rising, setting higher highs with each run-up?

This week we will explore these and a few other paradoxes, plus a quick lesson in poker, bond market style. It's once again time to move back from looking at the financial data trees and see if we can figure out what kind of investment forest we are in.

(Yes, I can still hear you asking, "So what are interest rates going to do? Should I lock in today's mortgage rates? Will rates ever go back down?" The answer is complex. But since you are holding a gun to my head, I will give you my guess in this letter.)

Let's Pay the Piper Tomorrow

Last week's letter brought more than a few readers to question my analysis of the economy. How can I suggest Muddle Through* (even with an asterisk) given the terrible imbalance in our trade deficit, an over-valued dollar, debt at record levels, a huge government deficit, rising unemployment, rising rates which will kill the mortgage and housing markets and so forth? Aren't we at least close to the End of The World As we Know It?

Of course, a few wrote to point out the rising leading indicators, improving (albeit modestly) areas of capital spending, a tax cut getting ready to kick in, record Federal Reserve stimulus, low rates which are helping consumers, and increased consumer confidence. Plus, isn't the stock market telling us that the economy is getting ready to grow at 3-4% once again, just like the Blue Chip economists predict?

Aah, the loneliness of being stuck in the Muddle Through middle with you, dear reader.

Before we get into the meat of the letter this week, let me discuss the curious notion that the market is telling us anything. Barry Ritholtz of the Maxim Group sent me a recent summary of the bear market rallies. The S&P has rallied over 21% five times since its high in March of 2000, averaging almost 25% on each of those gains. Four of those times it has fallen back. The fifth time is the current mini-bull.

The NASDAQ has had 5 rallies of over 37%, with the average being 42%. Four have failed. We are close to the top of the 5th.

Was the market telling us anything in the last four rallies? Was the market telling us the economy was getting better as it topped out in May of 2001? The economy entered a recession only a few months later (I predicted in August of 2000 that we would see a third quarter 2001 recession). I seem to remember pundits telling us (and getting a few letters from readers) that the markets were forecasting that a return to a growing economy was just around the corner. "Look at all the stimulus the Fed was applying (in the form of rate cuts)," we were told. "Don't fight the Fed." The market assured us we were going to avoid a recession.

Each of the previous bear market rallies was touted as the "return of the bull." This one will fail as did the previous rallies. No secular bull has ever started from such high valuation levels. I will write more on this topic in Part Three of our series on markets next week.

I am highly suspect of the ability of the market to predict the economy, or much else for that matter. Eventually, the market will rise from some future bottom, most likely after (or during) a recession, and a new long term bull cycle will begin. Pundits in that future world will breathlessly report to us that the market is telling us the economy is on the mend. When it happens, they will talk about the wisdom of the market.

Until that time, which I believe is not in our near future, the optimistic market moves are merely bear market rallies, to be enjoyed while they last, and are not signs of the incipient wisdom of a stock index. They are to be appreciated, as they keep the market from sinking too fast and bringing on a serious recession. It is a blessing that these cycles take so long. I, for one, am grateful to the optimists who work so hard to avoid a truly devastating bear market, sacrificing their money in the process. It is a strange paradox that we should avoid their advice during secular bear markets, but hope that not everyone else does.

Poker at the Federal Reserve

But where can we find wisdom? Let's turn to the poker game called Texas Hold'Em, which seems to me might hold some insights into the markets and the economy.

Texas Hold'Em is a popular poker game. For the uninitiated, this is a game where every player is dealt two cards, then three cards (called the flop) are played face up which every player can see. These cards are part of every player's hand. Then two more cards are dealt face up one at a time (These cards are called the turn and the river, respectively). The situation is that every player gets to use the five cards on the table and combine them into the best possible five card poker hand using the two cards in his hand. After each deal, there is a round a betting. Ultimately, the difference is of course the "hole" cards in your hand. The betting hinges on how good you think your hand is compared to the other players. When you bet you are saying either 1) "I have the best hand and I'll risk my money on that belief" or 2) "You have a poor hand, and you will fold if you are forced to put money on the table."

The current game between the Fed and the bond market is similar. This spring, as "the flop" came down, everyone in the market, including the Fed, could read all the data in the cards. The Fed told the bond market that their "hole cards" were their ability to fight deflation by physically lowering long bond rates if they needed to.

The bond market response was to believe the Fed and start the process of lowering long-term rates without the Fed actually having to do anything. The Fed bluffed the market into doing their work. Like the walls of Jericho, mortgage rates came tumbling down, mortgage re-financings went through the roof and deflation was dealt a blow, with nothing more than a little jaw-boning. (I will resist the comparison with Sampson and the jawbone of an ass. It would be much too easy.)

Then the turn card (the fourth "up" card) was dealt. That would be at the last Fed meeting. The bond market, ever an astute observer of gambler behavior, thought it read some ambivalence in the Fed posture. Was this the last rate cut? If so, that meant interest rates had no where to go but up. While the Fed still promised to hold short rates down, would they really back up their bluff and actively target long rates? If not, then why would you buy bonds at what would obviously prove to be the lowest interest rates of the last 50 years? The statement they released did nothing to make the bond vigilantes think that the Fed was ready to work the long end of the yield curve.

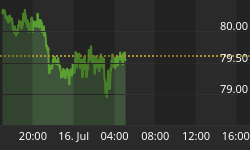

The response of the bond market was to "call and raise." And raise they did, by taking interest rates up on the ten year bond by more than one half percent in just a few weeks.

This rise in interest rates is more than of just academic interest. The next rise in interest rates is seen as a potential pre-cursor to market and economic turmoil.

Martin Barnes is one of my favorite analysts. He has certainly been as right as anyone for over two decades. His work at the Canadian based Bank Credit Analyst has been the soul of calm and thoughtful analysis. He sees a period of economic growth in the 3-4% range for the next 12-18 months. (He is somewhat more optimistic than my Muddle Through prognostication.) Thus it caught many of us by surprise to read the following from his June letter:

"The Federal Reserve has implicitly made an extraordinary commitment to hold short rates at current extremely low levels for an extended period, in order to hold down long-term rates. This gives a green light for hedge funds and speculators, but it will be hard to avoid major market turmoil when the Fed decides it is time to tighten. A long period of low short rates will feed mini-bubbles in a range of assets, is bearish for the dollar and bullish for gold and financial sector shares.... Policymakers will be successful in boosting the economy in the short run, but are creating even bigger problems down the road in terms of increased leverage, greater financial excesses and a larger current account deficit. Eventually, there will be enormous pressure to try and devalue accumulated debts through increased inflation.

"The U.S. policy environment has never been more stimulative. All of the policy levers are at maximum thrust and, unusually, are working in the same direction. The sheer force of this reflation should pull the U.S. economy out of its recent doldrums, rewarding those investors who have added some risk to their portfolio. However, markets could be very turbulent when the Federal Reserve is eventually forced to start raising interest rates to more normal levels. Moreover, while aggressive reflation will help the near-term economic outlook, problems are being stored up for the future via increased consumer leverage, a rapidly deteriorating fiscal outlook, and a widening trade gap.

"....The dark side of current reflationary efforts is that they are leading to increased financial imbalances that will cause problems down the road. Consumers are taking on more leverage, government finances are deteriorating dramatically and the bloated current account deficit is continuing to increase. None of these trends are sustainable over the long term." (The Bank Credit Analyst, June 2003, www.bcaresearch.com)

For our purposes today, the key sentence in those words were: "However, markets could be very turbulent when the Federal Reserve is eventually forced to start raising interest rates to more normal levels."

If long term interest rates rise beyond a certain point (more later), that will create a different set of issues, but it will be very problematic nonetheless. If capital spending has not rebounded from its current doldrums and if the economy is not producing net new jobs when the interest rate rise begins, as it inevitably will, the turbulence will be more than merely "very."

Today, the interest rate rise has merely taken us back to where we were a few months ago. I do not think this will affect the housing market all that much in the near future, as rates this low were good for the markets only a few months ago, and they did not dip into the 5% mortgage rate range for more than a few weeks.

If rates were to rise to much higher levels, this would change. The lower the mortgage rate, the higher the loan you can qualify for. Since the tendency of much of the US market is to buy as much house (in terms of dollars) as you can afford, the lowering of rates over the years has helped push the rise in home values.

When rates go back up, the pressure is in the opposite direction. Since home values are the Wealth Effect that is most closely tied with consumer confidence and spending, there is some point at which increasing mortgage rates become a serious drag on the economy if business spending and job growth are not on a roll to offset this.

Mortgage re-financing dropped 21% last week as rates rose. That sounds bad. But when you look at a long term chart of mortgage re-financings, we are still at very high levels. I know that borrowers take out a lot of money when they re-finance and that has been a big part of consumer spending, but rates are not so high today as to preclude continued borrowing. But it is not about today that we should beam concerned. It is the future about which we all obsess.

The only seeming agreement among observers is this: there is a point at which if mortgage rates were to rise in the current economic climate that the higher rates would precipitate a recession.

At what point do rates get too high and begin to pull down the economy? No one seems to know. There are just too many variables to factor in. There is a lot of disagreement or scratching of the head. Is it 6% mortgage rates? 6.5%? Can we go back to 7% in today's economy without any problems?

Bonds hate uncertainty. And right now they are not certain as to what the Fed is saying. Have rates been cut for the last time? Is deflation no longer a concern? If deflation is not a concern, then should we worry about that ancient enemy of bonds: deflation? Thus rates rise.

Dealing the River Card

And now we come to the river card - the last card to be played before the final round of betting. The river card will be dealt next week as Greenspan speaks. This may be one of his most important speeches of his career. It will certainly be one of the most watched. Every riverboat gambler that calls himself a bond trader will be watching for any signs of perspiration or nervousness as he looks at his cards.

With due regard for Greenspan, he has a tough assignment. It is a delicate game. The Fed has been telling us for some time they will work to hold long rates down to combat deflation if necessary. That "bluff" has helped bring rates down.

If he leads traders to believe that the Fed is no longer worried about deflation then rates will rise as the bond vigilantes will begin to worry about inflation. Why buy long bonds at today's low rates when the Fed is going to allow long rates to rise, thus making your bonds worth less?

If he talks about concerns of deflation, will the market believe him if he does not commit to action? Most observers I read believe the Fed will work to lower long rates if a recession or deflation appears at the front door. It is also widely believed that the Fed is loathe to do anything of that nature unless absolutely forced to. That is a very drastic action, and would be admitting that the economy is in serious shape.

If the Fed can talk rates down without actually having to do anything, it is the best of all worlds. The bond market seems to be calling the bluff. Next week we see what the last card reveals, and how the market reacts.

One or Two More Complications

Let's see if I can cloudy the picture even more. The Japanese bond market is in revolt. Greg Weldon reports that Japanese investors have sold more foreign bonds in the last four weeks than they have in total for years. It seems they are buying the Nikkei (Japanese stocks). This is a huge shift. This has put pressure on US rates. This started just a few days before the recent Fed meeting. Perhaps it precipitated the US rise in rates, but the bond market surely followed the lead.

This should also put pressure on the yen, making it rise. This is something the Japanese government does not want. They have been working to keep the yen from rising during this period, which is what the yen would normally do when investors start selling foreign bonds. (As an aside, Dennis Gartman points out the Chinese are the main buyers of these bonds. But that is for another time and another letter.)

Will the Japanese central bank help out a fellow central banker in need (Dr. Greenspan) by buying long US bonds, which will help the US (their important customer) and also lower the yen? Or will they decide that a rising Nikkei will be enough to offset the problems at home that would result from a rising yen? Will a rising stock market be enough to trigger a reflation in their economy, or will they need to use their last bullet and devalue the yen?

Greg Weldon also did an entire letter on what gold looks like to the rest of the world. (Greg's web site for his outstanding letter is www.macro-strategies.com. You can get a free 30 day subscription.) In country after country, gold is NOT in a bull market. It is signaling deflation. The worldwide wave of deflation has not subsided.

Korea is now in recession. Germany is either in recession or soon will be. German Chancellor Schroeder has called for the European Central Bank to work to bring down the value of the euro. Numerous Asian countries are working to bring their currency down against the dollar, even as we run huge trade deficits.

It is simply not possible for every country to devalue their currency simultaneously. The end result of this much government manipulation of the markets will not be good. Thus, even as gold tells us deflation is possible, gold is the one "currency" which cannot be inflated by a government. I was bearish on gold for all of the 90's and turned bullish in February of 2002. I expect I will be bullish for a long time. As Bill Bonner wrote today in today's Daily Reckoning, "Buy gold when it falls below $340. When it rises above $340, buy some more." A steady accumulation plan for gold is a wise move.

The Gun to My Head

But I can still hear you asking, "So what are interest rates going to do? Should I lock in today's mortgage rates? Will rates ever go back down?"

The answer is complex. But since you are holding a gun to my head, I will give you a simple guess.

If we have a recession within the next 18-24 months, and if inflation has not reared its ugly head, then there is the real chance we will see long bond rates drop. That will be the primary card (perhaps the only real one) the Fed has left to play to try and jump start the economy. A recession is by nature deflationary. I believe if the Fed is forced by either a shock to the market (which will cause a recession) or the rising of rates too high so as to create the probability of a recession, they will work to lower rates.

My guess (and it is only that) is that we will see lower rates one more time during the next recession which is not yet on the horizon. The Fed will work to postpone that day for as long as it can. I expect that will be the final bottom of the bond market.

What should you do today? If it makes sense to refinance your home today and lock in low rates, I would do it. If my guess is right, then you will get another chance to refinance again. If I am wrong, then you will be happy with your rate in the years to come.

Paris, Geneva and Inflating My Book

This time next week I will be with my friend Bill Bonner at his chateau (otherwise known as a money pit) in Ouzilly, France. He has promised good wine and there is always interesting conversation. His book on Japan and its implications will soon be out, and it promises to be good, from the drafts I have seen. He has also asked how I feel about a workout of moving stones, but I think my back is going to somehow not be up to such. I will report to you of our conversations. Sunday back to Paris and then Monday night on to Geneva. It will be a very full schedule, with a few media moments, I am told. I will be back in the office on the next Friday, writing to you of what I learn. With the wonder of the internet, I can stay connected, and hopefully will not find myself to far behind. We will see.

It is now very hot in Texas. In an effort to remain married, I have promised my bride to take her from the Texas heat when I get back. We will go to Halifax for the cool of the Canadian summer, where I intend to finish my book, which keeps inflating on me. It seems there is always one more important idea. It is shaping up nicely, though, and I think it is going to be a very useful tome to help you with your investment decisions.

Have a great weekend, and spend some time with a friend or two.

Your looking for his passport analyst,