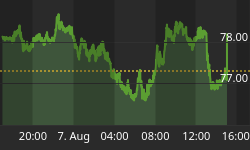

The Fed's decision to cut its overnight discount rate before the market opened on Friday might've wiped out quite of few traders and investors, who were betting against the market. Based on my "8% rule", I thought it was a little late in the game trying to short the market anyway. This may be nothing more than just blind faith, but the Fed's liquidity injection that limited the fall, from the Aug. 8 intraday high of 1503.89 to the Aug. 16 low of 1370.60, to 8.86% should've served as a precursor (see Chart 1). In fact, I thought this 8.86% fall might've gone a little father out of the comfort zone. As I've referenced before, repetitive patterns from the past indicate this 8% range is, for whatever the reason, perhaps a manageable threshold (see my 8/12/2007 Market Bulimia).

Chart 1

In any case, as much as these "tardy" short traders, particularly option traders, have been hurt, and as much as the bulls have returned to proclaim their Dow 15000 target, Friday's peculiar intraday action didn't seem to share similar bullish sentiment. For one thing, the put option continue to outpace the call option.

The thick black curve on Chart 2 below shows that, after the initial shock, the CPC (CBOE total Put-to-Call options ratio) rose above the neutral level of 1 at around 10:30 a.m. and maintained above this level throughout the rest of the session, despite the rebound of the S&P 500 Index (gray curve). As the market rallied, investors felt more compelled to buy protections. It's interesting to see, for example, the premium paid on the QQQQ (Nasdaq 100 powershare) September under $40 put options even though the Q's currently trading at above $46.

Chart 2

The massive technical overhead resistance may have a lot to do with the sentiment. The overhead resistance represents the "surplus" of buyers, who were trapped in a price range where the selling took place abruptly. In all likelihood, if the price should rise near this level again, these buyers would then become sellers. This is the fundamental psychology behind any price resistance.

The sum of all the up and down volume of the S&P 500 Index over the past 20 trading sessions (7/13/2007 - 8/17/2007) shows that most buyers came into the game when the price moved from approx. 1470 to 1480 (see the longest LIGHT-gray horizontal bar on Chart 3 below. This was where the biggest buying took place. And, if you'd go back to Chart 1 above, you'd see that this happened on the last leg of the 3-day fearless rally (Aug. 6 - Aug. 8) before the major selloff began (red horizontal line on Chart 1). This 1480 is therefore the primary short-term resistance that the market will have to overcome in order to restore higher level of investor confidence.

The secondary resistances, or the second longest LIGHT gray bars on Chart 3, can be identified at approx. 1455 and 1468. The LIGHT gray bar at 1455 is not only at the lowest price level, but it's also accompanied by the largest selling volume - the longest DARK gray bar. This makes it the S&P's first line of resistance.

Chart 3

So, the dynamics of the action of the buyers trapped in these price ranges and the price movement of the market in the coming week will tell us whether this so-called correction is indeed over. Of Course, we know better not to fight the Fed, but any celebration or heroic act prior to any sign of having these tough resistance levels removed may be pre-mature, to say the least.