On September 2nd, at the 2004 Republican National Convention, President Bush's remarked:

"Thanks to our policies, homeownership in America is at an all-time high. (Applause) Tonight we set a new goal: seven million more affordable homes in the next 10 years so more American families will be able to open the door and say: Welcome to my home. (Applause)" [Italics Mine]

On August 31st of 2007, while discussing homeownership financing, President Bush stated:

"One area that has shown particular strain is the mortgage market, especially what's known as the sub-prime sector of the mortgage market. This market has seen tremendous innovation in recent years, as new lending products make credit available to more people. For the most part, this has been a positive development, and the reason why is millions of families have taken out mortgages to buy their homes, and American homeownership is at a near all-time high.

Unfortunately, there have also been some excesses in the lending industry. One of the most troubling developments has been the increase in adjustable rate mortgages that start out with a very low interest rate and then reset to a higher rate after a few years. This has led some homeowners to take out loans larger than they could afford based on overly-optimistic assumptions about the future performance of the housing market. Others may have been confused by the terms of their loan, or misled by irresponsible lenders. Whatever the reason they chose this kind of mortgage, some borrowers are now unable to make their monthly payments, or facing foreclosure." [Italics Mine]

Or, we could look at the words of Paulsen or Bernanke or a Democrat or Republican or a conservative or a liberal from any time in history, past or current... Anyone who takes the time to look at the littered trail of political leaders' speeches will find comments from both parties' leaders espousing whatever words Americans want or wanted to hear. Rarely does the public hear what it true. The truth is ugly, and as such it is socially and politically unpalatable.

The truth is most of us, at one time or another, have benefited from our fiat money system. It has promised us whatever we need, delivered by truckloads of increasingly worthless dollars. As Dr. Larry Parks notes, when prices go up, no one talks about the source of inflation, only the effects and the need to, "manage inflation expectations."

Why not deal with the root cause - the expansion of the money supply. Why not tell the public that after so many years of depending on inflation and bailing out the ever-present "current liquidity crisis," we've now reached the point where it's too painful to continue and will be too painful to stop. Is it any wonder that most would rather have someone in leadership "manage it," rather than honestly tell us what takes place in our financial system?

And, this is not just an American phenomenon. In its 2007 Outlook, The Asian Development Bank reported the following money supply annual rates or growth for the People's Republic of China and India since 2002.

| Country | 2002 | 2003 | 2004 | 2005 | 2006 |

| China | 16.9 | 19.6 | 14.5 | 16.7 | 16.9 |

| India | 14.7 | 16.7 | 12.3 | 21.2 | 20.0 |

And, the story is much the same around the globe. As we listen to the media discuss our political and financial leaders' latest fixes to the problem, let us remind ourselves that over time fiat currency systems create the greatest hazards - be they moral, economic, or financial.

Never mind that the Yen, Euro, and most other currencies are gaining against the U.S. dollar or that many countries are loosening their ties, via reserve purchases, to the same. The Yen carry trade serves as a great proxy for a heavily leveraged trade, moving against the investor, "coming unwound," and placing pressure on other markets. This could just as easily be the CDO market, the junk bond market, commercial paper, repos or any market that has benefited from loose credit and liquidity over the last several years.

For those who are experiencing confusion as to how to invest in this market, contrasting the Fed's August 7th and August 17th statements lets us know we're not alone. On August 7th, we read:

"Economic growth was moderate during the first half of the year. Financial markets have been volatile in recent weeks, credit conditions have become tighter for some households and businesses, and the housing correction is ongoing. Nevertheless, the economy seems likely to continue to expand at a moderate pace over coming quarters, supported by solid growth in employment and incomes and a robust global economy."

But, a little over a week later, on August 17th, we read:

"Financial market conditions have deteriorated, and tighter credit conditions and increased uncertainty have the potential to restrain economic growth going forward. In these circumstances, although recent data suggest that the economy has continued to expand at a moderate pace, the Federal Open Market Committee judges that the downside risks to growth have increased appreciably. The Committee is monitoring the situation and is prepared to act as needed to mitigate the adverse effects on the economy arising from the disruptions in financial markets."

So what happened? Basically, we found out the sub-prime mess wasn't a sub-prime mess after all. It wasn't contained to sub-prime, America, or hedge funds. Rather, the problems are as numerous and far reaching as the liquidity which created them. When contracting liquidity resulted in a money market fund suspending customer redemptions, we began to realize the problems could lie anywhere. By reshuffling residential mortgage backed securities through CDOs enough times, it began to show up in asset backed commercial paper and money markets. For fear that they would not be repaid, lenders have become less inclined to lend. So, credit contracts. John Williams notes:

"In the weeks ended August 15th, 22nd and 29th, respectively, seasonally-adjusted (unadjusted is little different) commercial paper outstanding plunged by $91 billion, $90 billion and $63 billion." John Williams, Shadow Government Statistics, Flash Update, September 2, 2007.

To counter this contraction the Fed, indeed many central banks around the world, went to great lengths to add liquidity back to the system. Consider the following media reports. On August 9th, we read:

"The European Central Bank scrambled to head off a potential financial crisis on Thursday by pumping an emergency €94.8bn ($131bn) into the region's banking system after liquidity in the interbank market started to dry up, threatening banks' access to short-term funds.

The cash injection was the biggest in the ECB's history, exceeding the €69bn provided the day after the terrorist attacks of September 11, 2001. The ECB also made an unprecedented one-day pledge to meet 100 per cent of all funding requests from financial institutions." [Italics mine] ECB Injects € 95bn to Help Markets

And, on August 11th:

"The Federal Reserve pumped 38 billion dollars into the banking system Friday, marking its biggest operation since the week of the 9/11 terror attacks, as it vied to shore up the US financial system." [Italics mine] Fed pumps 35 billion into market in biggest move since 9/11

And, on August 17th:

"The Federal Reserve approved a half-percentage point cut in its discount rate on loans to banks Friday, a dramatic move designed to stabilize financial markets roiled by a widening credit crisis.

The action had an immediate positive impact on Wall Street after days of losses." Feds Cut Discount Rate in Surprise Move

And finally, on August 30th:

"Banks increased their borrowing from the Federal Reserve for a second straight week as the central bank worked to deal with a credit crunch that has roiled global financial markets." Banks Boost Fed Borrowing for Second Straight Week

Again, Williams' notes:

"Seasonally-unadjusted discount window borrowings by banks, following the Fed's heavily touted discount window actions, jumped from a daily average of $6 million in the two weeks ended August 15th, to $1.301 billion in the two weeks ended August 29th. M2 [a money supply measurement] jumped a seasonally-adjusted $43.6 billion in first reporting of the week ended August 20th, up at an annualized growth rate of 36.4%." [Comments mine] John Williams, Shadow Government Statistics, Flash Update, September 2, 2007

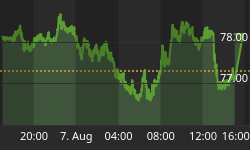

Since perspective is lost with each additional zero it's worth noting that, per the numbers above, average daily borrowing from the discount window is up more than 216 times. And, as evidenced by the prior chart, since August 17th, the markets have been propped up by these unprecedented amounts of liquidity. But, will it last? There was a time when the markets were thought to be a reflection of the economic viability of a nation. If that is still the case, it does not bode well for the markets.

| Symbol | Index | 12/29/06 | 9/5/07 | % Gain/Loss |

| $INDU | Dow Jones Industrial | 12,463 | 13,305 | 6.76% |

| $SPX | S&P 500 | 1,418 | 1,472 | 3.81% |

| $WLSH | Wilshire 5000 | 14,257 | 14,846 | 4.13% |

| $RUT | Russell 2000 | 786 | 790 | 0.51% |

| $NDX | NASDAQ 100 | 1,756 | 1,994 | 13.55% |

| Sectors | ||||

| $RLX | S&P Retail Index | 499 | 479 | -4.01% |

| $HGX | Philadelphia Housing Index | 235 | 166 | -29.36% |

| $XBD | AMEX Broker/Dealer Index | 241 | 221 | -8.30% |

| $BKX | Philadelphia Banking Index | 117 | 104 | -11.11% |

| $HCX | S&P HealthCare Index | 388 | 400 | 3.09% |

| Brokerage Houses | ||||

| GS | Goldman Sachs | 198.34 | 177.81 | -10.35% |

| BSC | Bear Sterns | 161.75 | 108.95 | -32.64% |

| MER | Merrill Lynch | 91.97 | 74 | -19.54% |

| LEH | Lehman Brothers | 77.63 | 54.35 | -29.99% |

| MS | Morgan Stanley | 66.89 | 62.56 | -6.47% |

| Banks | ||||

| JPM | JP Morgan | 47.25 | 44.17 | -6.52% |

| C | Citigroup | 53.98 | 46 | -14.78% |

| BAC | Bank of America | 52.22 | 49.95 | -4.35% |

As you can see, while most of the broad indexes are up for the year, most sectors, banks and brokerage houses are showing losses.

Clearly, since they have proven to be neither objective nor knowledgeable, we cannot look to our political or financial leaders to forewarn us of market declines. If we are to safeguard our investments, we must also look beneath the prices of the broad indexes. If you want to do a preparedness check, look at how your investments performed during our first hint of a liquidity crisis - from mid-July to mid-August.

If you're with the Fed (or not?) perhaps you should consider looking at what various experts, from a variety of disciplines, have to say about finance. Perhaps you should consider becoming a part of The Investor's Mind and benefiting from the research and views of some of the most experienced individuals in the world of money. To get a feel for the educational material we've presented to our readers since January of 2006, click here. We continue to gain recognition for our 154-page industry paper on short selling, Riders on the Storm: Short Selling in Contrary Winds, which can be obtained with a subscription to The Investor's Mind. To learn more about our mission, as well as our educational and advisory services, visit our website. Above all, don't panic, be flexible, and use your mind!