The dollar rebound of the past 3 days has emerged on a powerful combination of escalating evidence of weakness in the Eurozone and the UK, signs of a change in rhetorical tack in the ECB vis-à-vis euro strength and a much needed decline in gold. On the US front, the striking deterioration in new home sales, existing home sales and pending home sales has not yet spilled over to the US consumer. Both of the manufacturing and services ISM reports showed declines but remained well within the expansion phase.

Finally, one cannot ignore the current retreat in gold prices, which was the biggest drop since the market slide of August 16. We continue to expect further pullback in gold, eyeing as low as $710 per ounce. The dollar upside of such occurrence could emerge on the heels of a stronger than expected rebound in non-farm payrolls and/or strong language from Europe vis-à-vis the strengthening of the euro. A dollar rebound could also take place on the heels of a sell-off in equities as has been the fact this year. A decline in the high yielding sterling is also expected to comprise a vital part of a short-term dollar rebound as the Bank of England is forced to shift towards a dovish stance.

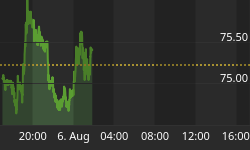

USDX Rebound Eyes 79.30

EURUSD Temporary Pullback to Breach $1.40

We expect the ECB president Trichet to mention the term "vigilance" in expressing the bank's inflation stance, but he may also acknowledge the recent signs of slowdown in the region which could retain the euro's negative bias of the past 4 days.

We do not anticipate next week's G7 to specifically address dollar weakness/euro strength because G7 meetings have constantly called for an "orderly adjustment of global imbalances", of which a dollar decline is an unspoken but required development. The communiqué is expected to reiterate calls for greater flexibility in China 's currency regime, while adding the generic remark that "exchange rates should reflect economic fundamentals" and that it continues "to monitor exchange markets and cooperate as appropriate" . When all said and done, we expect the final outcome to temporarily stem the dollar's decline and/or cap the euro's appreciation.

Having broken the $1.41 figure, EURUSD sees interim support at the 4-month trend of $1.4080, while a breach below 1.4060 sees support at 1.40010. Key foundation stands at 1.3950. Upside capped at 1.4150.

GBPUSD to Test $2.0000

Sterling finally weakens to our projected $2.0020 target and is set for further losses as we approach the Bank of England announcement and the US payrolls report. Weakness in services PMI follows similar weakness in the manufacturing and construction and surveys. Increasing calls from British business lobbies such as the CBI and BCC for the Bank of England to cut interest rates must be taken into account as they fall in line with increasingly gloomy surveys of business conditions. Signs of a pullback in mortgage loans and in the RICS price index are also serving as the latest empirical evidence against further rate hikes. More importantly, with inflation at 1.8% -- well below the 2.0% mandated target -- a rate cut should is the next policy move, which we expect to take place as early as November once the BoE has prepared its quarterly inflation report due for release one week after the November 6 MPC announcement.

Cable traders will watch the BoE statement at 7 am EST tomorrow for the bank's stance on inflation and pull back in business activity. A hawkish statement may send cable back above $2.0350 but resistance to stand at $2.0380. Pre-payrolls dollar strength to push the pair back towards $2.03, with support targeting 2.0270. A surprise BoE cut could call up 1.9850.

AUDEUR Sees Further Advances Ahead

One week after telling clients of an upmove to 0.6245 from 0.6205, AUDEUR is now hovering at 0.6260 after having tested 0.6290. Despite the 400-point rally of the past 6 weeks, we expect the pair to retain further moves ahead towards 0.6330. Wednesday's release of stronger than expected 0.7% increase in Australian retail sales in August from July's 0.7% is likely to preserve the RBA's cautiously hawkish stance. Upside momentum in the cross pair is seen reemerging on the heels of a broadening but temporary euro retreat. A corrective retreat may be limited at 0.6160. The pair should remain a viable play in the medium term as long as gold prices remain above $705 per ounce.