"The power of the Fed to literally change the game... cannot be ignored. Anti-gold forces now stand as ready as ever to force a consolidation in precious metals. There's also a rising probability that the dollar will at last see at least a relief rally, which could have metals trading weaker ... so, the game plan continues to be resisting the temptation to short without confirmation and using the 5-week sma in gold and the 5-day sma in silver to signal a major reversal. Curiously, a 38.2% Fibonacci retrace of the move off the summer '06 lows in gold would bring us back to the May '06 highs." ~ Precious Points: Judgments Affirmed! November 11, 2007

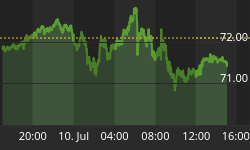

The forces traced for months in this update continued to move the metals markets this week, with softness in gold and silver coming precisely from two factors this update has been warning about for the past few weeks. Weakness in gold began with strength in financials, which bottomed Monday and sparked a huge snapback rally in stocks on Tuesday, a rally that seems to have made rate cuts seem less likely. As expected, cracks in Europe continued showing this week, with the possibility for a cut in London and/or Frankfurt now a distinct possibility. This had dollar bouncing in the last half of the week and, as evident in the chart below, gold trading below the 5-week sma for the first time in a while, but something that's inevitable from time to time.

As posted in the TTC forums, a move to as low as $750 would still be a very healthy pullback in an otherwise rip-roaring bull market. The validity of the bull doesn't even come into question until the 50-week sma, currently about $675 in the front month futures. Silver, which had a similar week, is looking to set up a great entry point with support at the 50-day moving average at about $14. Failing this, there's strong support in the $13.50-$14 range.

So, while it seems the metals bull takes a much deserved rest and offers new sale price entries for buyers, let's quickly examine those forces that triggered the selling this week and see where they lead us. The single biggest headline of the week was the Fed quickly acting on the curious comments in its last statement and announcing the targeting of headline inflation. Recall the following statements from the November 4 'Precious Points' update:

"The balance of risk could have remained tilted towards preventing fallout from impending housing foreclosures, and this would have been consistent with Bernanke's remarks of a few weeks before. That the Fed chose to explicitly cite high energy and commodity costs not only undermines their precious core inflation figure - which now seems to exist only for justifying low interest rates and creating implausible GDP growth figures - it also underscores a long-standing theme of this newsletter, namely that rising metals prices are anathema to a central bank because they tend to erode the credibility of fractional reserve lending and fiat currency.

"But, sometimes those in positions of authority simply have no good options and, when given the choice of igniting a parabolic rise in gold and oil or carefully acknowledging that its core inflation readings are fairly irrelevant to real world consumers, and are ultimately affected by the excluded items anyway, the Fed, it seems, takes the latter course. And whenever power makes hard choices, it's axiomatic that the alternative was even worse!"

So the Fed did a little bit of follow-through and did in fact "change the game" with its new headline inflation targeting. For the short term, at least, they continue to pump liquidity and are still likely to cut at least one more time in December or January, or whenever the credit markets oblige them to do so. In a widely publicized speech, Fed President Krozner is reported to have said, "reductions in the target federal funds rate tend to be associated with decreasing incremental benefits in terms of further mitigating ... risks and with increasing incremental costs in terms of the potential for inflation to increase." What better way to get more bang out your rate cutting buck than to stymie expectations with hawkish rhetoric and a new headline inflation targeting policy?

But it wasn't the Fed that did the most direct damage to the metals this week, it was the rebound in the dollar. The fact that it occurred in an environment of significantly weak economic data and earnings forecasts indicates a technical move or shifts by speculators. Certainly the reduced rate cut expectations played a role, but with 100% odds priced in for at least one cut by January, the more likely culprit was weakness in foreign currencies, particularly against the yen. Given that the Fed is most likely closer to the end of its cutting and the BOE and ECB closer to the start, this could be a trend that establishes some momentum over the coming months. Obviously this would spell short term weakness in metals, but would be planting the seeds for future gains.

Ultimately, it's probably not a good idea to bet against Bernanke's policy goals and it's likely he'll have further tricks up his sleeve over the course of his chairmanship. In the meantime though, the relief rally in the dollar cannot yet be treated as a major threat and, as we've seen, there is strong support beneath this recent rise in the metals as we enter their traditionally strong season. Demand fluctuations are often cited for the seasonality in gold, but the increase in money supply to accommodate withdrawals by holiday shoppers is another important factor, and the Fed has shown no signs of contracting the monetary base so far. We should continue to monitor the repo market for clues and, should gold find renewed strength in the days to come, watch to see if the 5-week sma acts as resistance. Even though $800 didn't hold as a floor, a prolonged sideways period at these levels would still be an important base for future rallies as it's unlikely, even if her gets it under some control, that Bernanke will ever succeed in getting the gold genie back into the bottle.