Starting in mid December 2007, the Fed began introducing new facilities through which depository institutions and primary securities dealers could obtain fed funds or U.S. Treasury securities collateral. The purpose of these new facilities is to relieve liquidity pressures in the money and capital markets, augmenting the reductions in the fed funds rate implemented by the Fed.

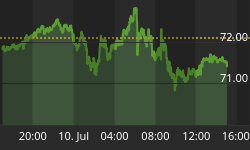

In mid December 2007, the Fed introduced the Term Auction Facility (TAF), effectively a term repo facility that allows all U.S. depository institutions that are required to hold reserves at the Fed and are in good financial standing to bid for term fed funds from the Fed. Any collateral that is eligible to be presented at the Fed's discount window, which runs the gamut from U.S. Treasury securities to commercial/industrial loans, also is eligible to be posted by depository institutions. Despite reductions in the fed funds rate, other unsecured interbank lending interest rates, such as LIBOR, were not declining in tandem, suggesting liquidity and/or counterparty-risk issues. Chart 3 shows that after the establishment of the TAF, money market conditions have returned to more normal relationships.

Chart 1

Although liquidity issues with regard to short-term unsecured interbank lending appear to have been resolved by TAF, liquidity and/or credit-quality issues with regard to mortgage-related securities remain. This is demonstrated in Charts 4 and 5 in which the yields on long-term mortgage-related securities are compared with the yield on the 10-year Treasury security. Whereas in the spring of 2007, the yield spread between direct FNMA 10-year debt and U.S. Treasury 10-year debt was about 40 basis points. In recent days, that yield spread has widened out to around 110 basis points. Similarly, in the spring of 2007, the yield spread between the rate on 15-year home mortgages and the rate on the 10-year Treasury security was in the range of 70 to 80 basis points. Early last week, the spread skyrocketed to 150 basis points, only to return to Earth yesterday.

Chart 2

Chart 3

In order to address these liquidity and credit-quality issues in the market for investment-grade mortgage-related debt, the Fed established two new facilities for primary securities dealers in recent days - the Term Securities Lending Facility (TSLC) and the Primary Dealer Credit Facility (PDCF). The TSLC allows dealers to bid for U.S. Treasury securities on loan from the Fed in exchange for high-quality mortgage-related securities. The TSLC does not inject new reserves (fed funds) into the financial system, but does allow primary dealers to exchange less liquid securities for the most liquid, U.S. Treasury securities. In turn, the primary dealers can easily borrow using these Treasury securities as collateral.

The PDCF is, in effect, a discount window for primary dealers. Dealers can borrow fed funds from the Fed at a penalty over the fed funds rate target. That penalty currently is 25 basis points. Primary dealers can post as collateral against their borrowing of fed funds from the PDCF in addition to Treasury and agency securities, investment grade corporate, municipal, mortgage-backed and asset-backed securities.

The TSLC and the PDCF would be expected to increase the liquidity in securities markets related to mortgages inasmuch as dealers know that they can easily borrow against this collateral from the Fed. With added liquidity in the markets for mortgage-related securities, mortgage interest rates would be expected to move lower now relative to comparable maturity Treasury yields. Moreover, with the establishment of PDCF, the likelihood that liquidity issues would morph into solvency issues for dealer/brokers would be diminished.