The following is an excerpt from commentary that originally appeared at Treasure Chests for the benefit of subscribers on Wednesday, April 2nd, 2008.

The joke this April Fool's Day was on the short sellers with yet another squeeze higher in stocks. Of course this has not been a problem since last summer as stocks have been (and remain) in a bear market. Unfortunately for short sellers this time around however, this bounce will likely be more robust than previous occurrences in that important cyclical influences have now gone positive, which will act as a tail wind for the bulls in fits and starts (choppy price action) right into the second quarter of next year. In this regard yesterday's violent rise was fuelled by hedge funds officially reversing the sell stocks / dollar and buy commodities / precious metals trade for the new quarter, implying they will endeavor to maintain these positions until June. And it just so happens this is when we are looking for a recovery high in stocks this year, sometime in and around mid-June in a possible double top test after an initial spike here in April, normally a seasonally strong month even in weak years. Of course May should provide some excitement to the downside however, which would bring gold / commodities back to life as the dollar ($) is sold once again.

In terms of Decennial Patten precedents, yesterday was the strongest start to a second quarter since 1938, opening the possibility of a 50-percent retracement of losses into summer, putting the S&P 500 (SPX) in the 1450 area, followed by volatility afterwards. Moving onward in terms of other years ending in '8' witnessing a bottom in the first quarter, a more robust outcome was experienced in 1948 (see Figure 3), with a top in mid-June (this is our outside timing target), however such an outcome is unlikely structurally (see Figure 4). What's more, yesterday's big gain was a characteristic 'jam job' (short squeeze) in a bear market, not a fundamentally based advance in the stock market fuelled by Doe Boys returning home with a pocket full of savings in war pay. In this respect it should be noted short sales are at record highs along with absolute put / call ratios on the rise, suggestive more gains should be anticipated on this basis.

As alluded to above however, this (meaning market internals), combined with the 'full nine yards' attitude on the part of master planners to revive the economy, where it's now apparent to all no amount of liquidity related measures will be spared, should also hold back any rally in the $, which is of course the constraint that will also keep a lid on the stock market's recovery moving forward. And this will bring gold back more quickly than technicals would have a 'reasonable man' believe, as was the case in the 1978 (see Figure 3) patterning, yet another year ending in '8' marking increasingly stressed conditions characterized by financial market(s) volatility and increasing central intervention. Here, gold should bottom ahead of a final top in the $ / stocks in June, with a repeat of the 1978 pattern suggestive this should be expected no later than the end of April. [i.e. or thereabouts (meaning extending into May) considering lags / greater extremes are apparent in the present sequence.]

Speaking of increasing central intervention, someone asked us to comment on the regulatory changes now proposed by the Treasury giving the central bank new and widened powers / authority / intervention capabilities. Ah - there's the rub - the Fed would have new intervention capabilities, which for gold bugs, is an increasing worry for fear of a precious metals confiscation. Of course the irony of such an outcome would be that with their new powers, the Fed is sure to accelerate bailout efforts associated with collapsing credit markets, which in turn will undoubtedly cause more inflation, and demand for gold. And in this regard, by way of the measures already proposed and instituted; again, they have proven beyond a shadow of a doubt they (the Fed) will go the 'full nine yards' to save their financial system, which to me, suggests they would not stop at an attempted confiscation of your gold and silver bullion. (This is why it's not a bad idea to buy some well-priced [low] 'collectible' and / or currency designated coins in your portfolio.)

So, the understanding is the Fed will inflate to infinity, which of course means one needs to own precious metals to preserve wealth, and are the same perpetrators who will bring down the financial system, then proposing confiscation of your gold as being necessary for the rebuilding of a new system, one based on grounded exchange principals. As the saying goes, if this were not so serious it would be funny. But nobody will be laughing in the end no matter what happens to your gold; of this one can be sure. In the meantime however, the Fed is inflating, and they will continue to inflate whether they are given these new powers or not, so continue to accumulate precious metals in this correction because it should be relatively short lived. Increasing monetization efforts to continue bailing out a stressed banking system will assure this outcome, make no mistake about it.

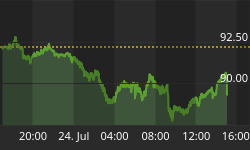

And make no mistake about the ulterior motives behind proposed regulatory changes giving the Fed these new powers. On the surface, while it may be true greater oversight on institutions it's backstopping may give the Fed a pre-emptive advantage, this will not prevent process from unfolding in the full measure of time. Of course in the meantime undoubtedly US authorities are hoping this will bring a bid back into the $ and re-instill confidence in US markets, which will help keep a lid on precious metals and commodities. Sure enough, based on the violent reversal in the sell stocks / dollar and buy commodities / precious metals trade yesterday, it appears they will see some success in this regard, fleeting as any near-term victories may prove as summer matures. And who knows, if the head and shoulders pattern in the 6-month TED spread pictured below traces out, we may all be quite surprised about how things turn out by summer with all the liquidity floating around these days. (See Figure 1)

Figure 1

Source: The Chart Store

One thing is for sure, you do not want to be short equities right now given this backdrop; not even those tagged for takedowns (oil, gold, grains) by master planners. In this respect, I am not suggesting precious metals / commodities will not continue to be sold, however with strength in the larger equity complex, relative weakness can be expected to be lessened. For example, routine corrective scenarios for gold and precious metals shares would involve only meager loses from current levels, with lasting support in both cases normally encountered at the 21-month exponential moving average. For gold, this would involve a test of last year's intermediate-term degree top in the $750 area, while for the Amex Gold Bugs Index (HUI), we are talking about a possible spike below 400 into the 380 vicinity in shaking out nervous investors. These are the worst-case targets we can see at this point.

Any way you measure it then, if these worst-case correction targets are hit later this month, then the majority of losses have already been endured, meaning thoughts of accumulation should increasingly entertained as April comes to a close. And again, if the economy / banking system continues to worsen, which is not a stretch by any means, interventions will need to get more robust in response, supporting the view pressure in the precious metals pipe should remain strong. Certainly the chart below showing a history of the 20 -Year T-Bond to 3 - Month T-Bill Spread points to this likelihood if the current sequence is only as severe as the 2000 - 2002 episode, which of course is not the case. (i.e. the need for speed in currency debasement rates is greater today, suggestive corrections in precious metals should be increasingly short lived until the larger sequence is completed.) (See Figure 2)

Figure 2

Source: The Chart Store

What's more, if the $ carry trade (replacing the yen carry trade) is to be maintained by speculators, this basically guarantees that the $ rally should be both meager and fleeting, matched by the opposite in terms of hard assets. The only way this would be proven wrong is if the Western led banking cartel has lost control of it's influence in the markets in that if they wish to continue attempting to bailout the system by issuing increasing credit, with the $ being central in the carry trade now, it must continue to fall on a secular basis. This is because of a necessity to continue bailing out the US consumer at the expense of inflation, which will invariably continue as money supply growth rates in emerging markets react by ballooning in compensation for the additional $'s they receive for their commodities. This in turn should keep general price levels rising, which would eventually feed into the Consumer Price Index (CPI), and this will breakdown real rates. (See Figure 3)

Figure 3

Source: The Chart Store

So, the hypothesis here is inflation will beget inflation on a global basis until credit mechanisms still governed by international bond markets are stifled, making sovereign debt markets the 800-pound gorilla in the room. Of course as money comes out of US bonds, in addition to looking for a home elsewhere (outside of the States), asset wise it will invariably be attracted to increasingly tight commodity markets given the inflation backdrop, of which precious metals qualify. (i.e. especially silver right now.)

It's as simple as that in my view when it comes to precious metals at present, where a little further patience by those wishing to accumulate should prove wise if history is a good guide. Remember, this is just the beginning of the quarter, where hedge funds will have a propensity to buy stocks / the $ and sell precious metals / commodities until June. And although they may have only limited success in this regard due to liquidity provided by buoyant stock markets, lower prices for precious metals will still likely be the result; so again, patience Prudence.

Good investing all.