So you lost big on crypto this year … but what you might not know—according to Credit Karma—is that you could claim a tax deduction for those losses. That should come as a bit of a relief to those bitcoin investors who lost a total of $1.7 billion in 2018.

And that $1.7 billion just covers those who sold and ran. Unrealized losses in bitcoin for those who didn’t sell reached a whopping $5.7 billion.

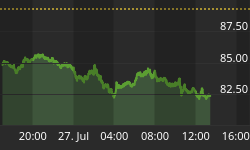

No, not a great year for being cryptic with investment cash. Not even great over the past 24 hours, which have seen the crypto market as a whole lose another $2 billion, falling to $121 billion. Bitcoin prices have now fallen below $3,600.

The latest price slump comes in the wake of news of a January 14 hack of the New Zealand-based Cryptopia Altcoin Exchange—the first exchange hacked in the New Year. And since security issues are one of the main things holding crypto back, any news of a hack puts downward pressure on prices.

So, from that perspective, 2019 isn’t getting off to a stellar start.

But we can still fix 2018 from a tax perspective at least—to lessen the blow.

According to Credit Karma, some may not be reporting their bitcoin losses because they don’t anyone to know about their income and this is one of the beautiful things about crypto—anonymity. Related: May Survives No-Confidence Vote Despite Huge Loss On Brexit Deal

However, “underreporting income could lead to an audit and having to pay penalties and interest,” Credit Karma cautions, in addition to “missing out on valuable deductions”.

To that end, Credit Karma recently conducted a survey showing that only 53 percent of American bitcoin investors plan to report their bitcoin gains or losses on their taxes. At the same time, 19 percent remain undecided, while 35 percent who specifically sold at a loss do not plan to report to the tax man. On the other hand, those who actually saw gains from the bitcoin investments were 59 percent more likely to report.

But perhaps most troubling, Credit Karma noted that 58 percent of all bitcoin investors were “not aware they could claim a tax deduction for their realized bitcoin losses”. The lack of knowledge compounds here, with 35 percent falsely believing they aren’t required to report their bitcoin gains or losses, with the majority of those thinking “they didn’t gain or lose enough money to have to report”.

Related: Big Oil Doubles Down On Blockchain Tech

Still, no one would likely blame you for not understanding the rules of this game when the tax authorities are as cryptic as digital currency itself. With that in mind, though, the IRS isn’t generally of the opinion that lack of knowledge is an excuse for misreporting income.

Part of the problem is that the U.S. treats cryptocurrencies as property subject to capital gains tax, the rates for which vary by income level and the classifications of which vary depending on how long the asset has been held by the owner.

The good news is that if you were one of the bitcoin loses of 2018, you could end up claiming up to $3,000 in losses this tax season, and perhaps more if you carry it over to next year. The bad news is that you definitely need to hire an accountant.

By Tom Kool for Safehaven.com

More Top Reads From Safehaven.com