Bitcoin HODLers constantly fret over the specter of crypto whales suddenly dumping their holdings en masse leading to a spectacular crash. Now they have one more reason to worry—mining farms who pay nothing for the colossal amounts of power they consume. Police in China’s eastern city of Zhenjiang have busted a giant mining operation that stole nearly $3 million worth of electricity for bitcoin mining in the largest crackdown ever of its kind.

Acting on a tipoff by a local power company that noticed an abnormal surge in power usage, the police nabbed nearly 4,000 power rigs from the giant farm and arrested more than 20 people involved in the illegal operation.

Well, $3 million worth of electricity might not sound like much—new tech such as data centers are notoriously power hungry and can guzzle more than that in a month. But read on and find why this latest heist should worry bitcoin bulls especially if it turns out that this is a widespread trend.

(Click to enlarge)

Source: CoinRate

Distorting the market

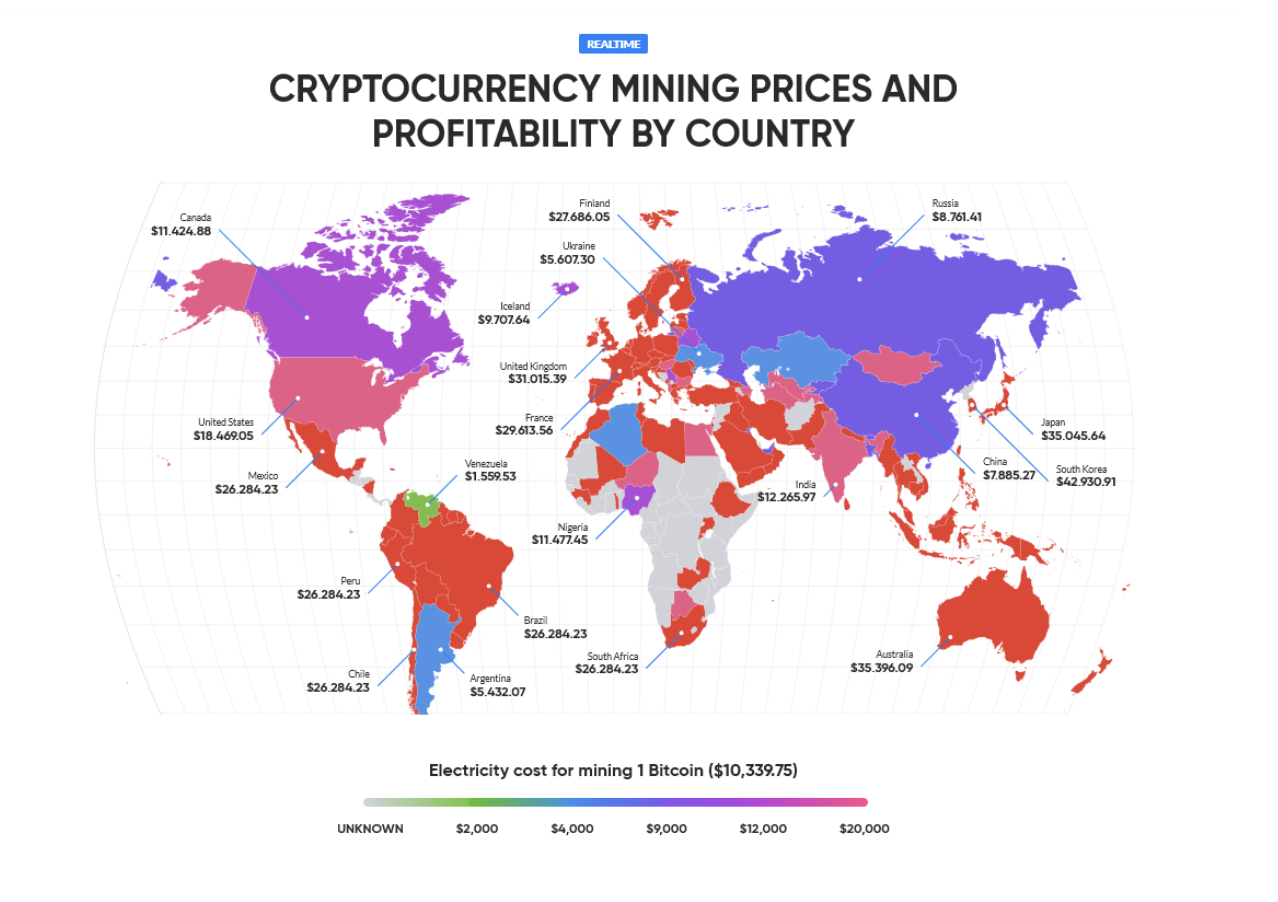

China is the world’s largest bitcoin mining venue with an estimated 80 percent of new coins coming from the market. That primarily has to do with an overabundance of cheap coal power making the country one of the cheapest places to mine digital coins.

According to CoinRate, it currently costs $7,885.27 to mine a single bitcoin in China at average power costs of 4.5 cents /kWh. That makes China the 7th cheapest mining location in the world. In contrast, average power costs in the U.S. clock in at around 12 cents per kWh, a considerable handicap for stateside miners compared to their eastern brethren.

Related: Welcome To The World’s Biggest Free Trade Area

Bitcoin prices have been on a rollercoaster lately—yet, even the current rate of $10,300-a-pop still leaves Chinese miners with handsome profit margins. Take away power costs and all a miner has to worry about are minor capital costs and overheads such as mining rigs, personnel and rent. Electricity is about 90 percent of the cost to mine bitcoin—take it off the equation and the equilibrium shifts dramatically.

Without paying for electricity, a miner’s break-even point drops so low that they are incentivized to sell their proceeds at almost any price point. Sure, the more adventurous ones will also play the HODL game in the hope of reaping maximum profits.

But still, the urge to sell at the earliest signs of trouble (read:market selloff) will be great since there’s little danger of booking losses.

Done on a large enough scale, this can lead to excessive volatility and keep prices permanently depressed.

Whales remain a bigger threat

You could argue that this is likely a worst-case scenario and bitcoin whales remain a bigger threat—and you probably would be right.

After all, we’ve heard of alarming reports of 40 percent of the world’s supply of bitcoin being in the hands of just 1,000 investors. More than a few bitcoin selloffs in the past have been blamed on coordinated action by these so-called whales.

In contrast, Digiconomist estimates that annualized global mining revenues are ~$7.8 billion, which is actually less than bitcoin’s $24.5 billion daily average volume as per CoinMarketCap. In other words, the total amount of bitcoin in circulation is much larger than what miners add to the pool every year thus potentially nullifying their actions.

However, if claims that only five percent of bitcoin transactions reported by CoinMarketCap are genuine are actually true, then price distortion by miners who pay nothing for their electricity becomes a significant threat.

By Alex Kimani for SafeHaven.com

More Top Reads From Safehaven.com: