Tokyo’s Bitpoint Japan Exchange has just been hacked to the tune of $32 million in various digital currencies held in a connected hot wallet, forcing it to suspend all services. Some two-thirds of the losses went to exchange customers, while the rest is shouldered by the exchange’s management company, Remixpoint.

No one knows, yet, how the massive hack went down, and an investigation is underway.

It’s not the first Japan-targeted crypto heist, either. Nor is it the biggest.

In January 2018, a record $534 million of NEM was stolen from the Japan’s Coincheck exchange, from a low-security hot wallet connected to the internet.

Four years earlier, Tokyo-based MtGox exchange was shut down after some half a billion dollars in bitcoin disappeared from its virtual vaults.

Elsewhere, in May this year, Binance saw a $40-million hack, as well, and the first half of this year has seen at least eight major crypto thefts.

In 2017, South Korea’s YouBit exchange was shut down and ended up filing for bankruptcy after a double hack.

In June this year, hackers stole over $4 million from Singapore’s Bitrue crypto exchange.

This latest hack comes amid a general pullback for Bitcoin prices, which suffered another $1,000 sell-off earlier this week but bounced back as of this morning, renewing bull optimism that it could regain recent highs above $13,000.

Another hack, of course, won’t help.

Nor will Trump tweets--though so far they haven’t dented crypto.

On Thursday, Trump decided to chime in on Bitcoin--an area he has traditionally avoided--attacking it and branding the digital currency world at large “unregulated crypto assets” that can “facilitate unlawful behavior, including drug trade and other illegal activity”.

In other words, he’s not a fan.

In one tweet, Trump noted that crypto currencies “are not money” and their “value is highly volatile and based on thin air”.

In another, he attacked Facebook’s Libra, which he declared “will have little standing or dependability”.

“If Facebook and other companies want to become a bank, they must seek a new Banking Charter …”

The final Trump verdict was this:

“We have only one real currency in the USA, and it is stronger than ever, both dependable and reliable. It is by far the most dominant urrency anywhere in the World, and it will always stay that way. It is called the United States Dollar!”

Related: The Problem With Modern Monetary Theory

Bitcoin, as of this morning, doesn’t seem to be responding dramatically to Trump’s Twitter barrage.

(Click to enlarge)

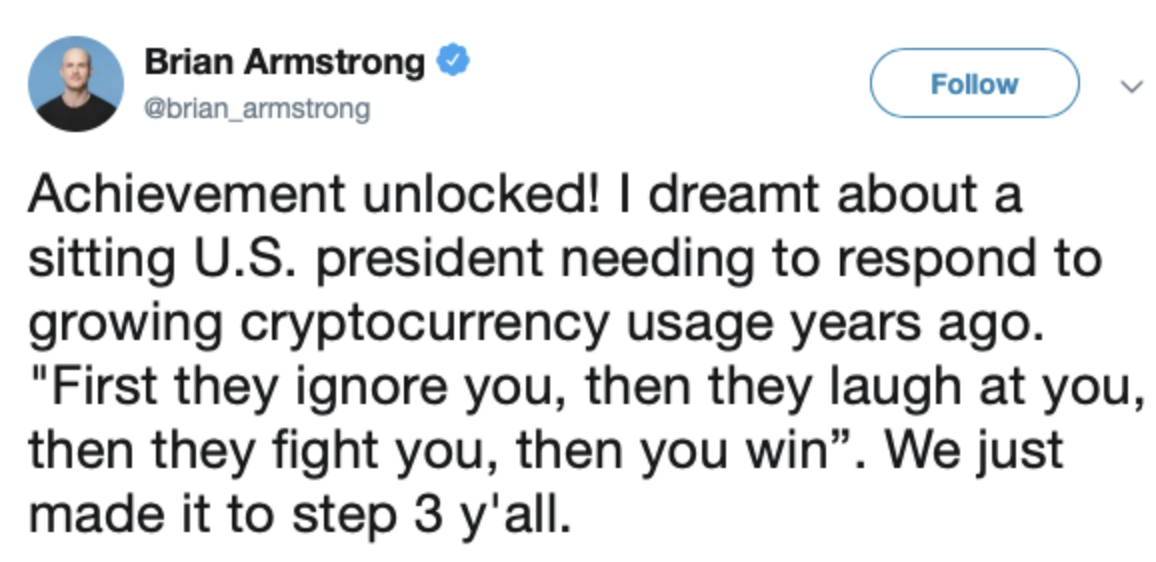

While the CEO of Coinbase, Brian Armstrong, conceded that Trump’s a major psychological event for bitcoin after all this time, he also claimed it as a victory of sorts.

(Click to enlarge)

Japanese crypto exchanges are supposed to be beefing up security, but it’s clearly not working. Last year, the Japanese Financial Services Agency (FSA) refrained from issuing any new crypto licenses, and ordered everyone to take measures to improve security.

But for crypto at large--and particularly for Facebook’s Libra--which was the real target of Trump’s tweets, it could be a harbinger of new regulations to come.

Trump isn’t the only one who’s gone after Libra this week. Even Fed chair Jerome Powell is on the same page as Trump with this one. He warned this week that existing rules do not suit digital currencies.

“Libra raises many serious concerns regarding privacy, money laundering, consumer protection, and financial stability,” he said, damning Libra to purgatory until these questions are addressed.

By Charles Benavidez for Safehaven.com

More Top Reads From Safehaven.com:

Yes, a lot of exchange platforms actually hold most of their coins in hot wallets. Most of them don't even bother to tell their users what percentage is stored in online and more dangerous wallets. That is why I always appreciate when exchangers make statements about it, for example, https://coindeal.com/security - CoinDeal states that 90% of the cryptos are held in cold wallets. More platforms should follow its steps to ensure higher security.