If you think this year has been good for Apple, try next year, says JPMorgan, which predicts the company will get 20-percent more valuable by the end of December 2019.

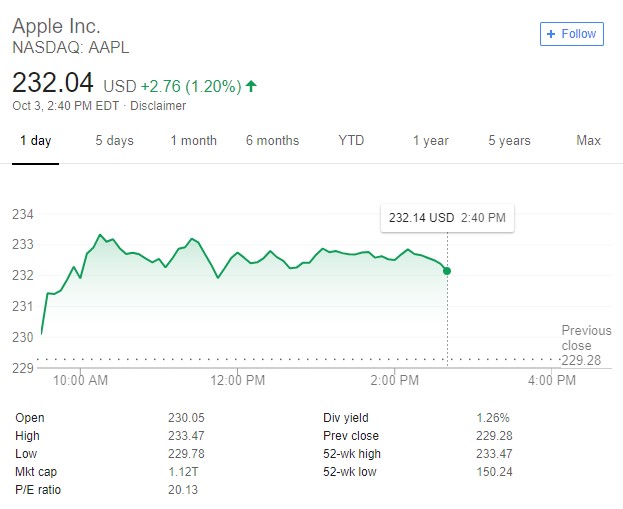

On July 2nd, Apple (NASDAQ:APPL) became the first-ever publicly listed U.S. company to hit $1 trillion. That feat happened when share prices reached $207.05 that morning. And it wasn’t a fleeting moment in the trillion-dollar club. Today, APPL is at $232.04 …

(Click to enlarge)

And JPMorgan thinks it’s got another 20-percent upside to it next year, initiating coverage with an “overweight” rating and price target of $272.

The iPhone has achieved all the greatness it’s going to, but the upside isn’t about the phone—it’s about the services business.

Fewer iPhone users are expected to upgrade to new phones next year because they like the iPhone X so much, so many analysts see a major sales gap looming for next year.

Those analysts might not be able to see how Apple is going to recoup the loss—but JPMorgan does.

In a Thursday note to clients, JPMorgan analyst Samik Chatterjee said that “while Apple’s leadership position in the premium smartphone market is well understood by investors, we still see considerable upside to the stock from current levels”, as reported by Business Insider. Related: Is This The Beginning Of The End For Facebook?

That’s because the shift to services has already begun in earnest.

"Apple has historically been regarded as an IT Hardware company tied to a short product refresh cycle of the iPhone in an extremely competitive smartphone industry," Chatterjee wrote.

"More recently, investors have been proved wrong on the pace of Apple’s transformation to a services company, with revenues in the Services reporting segment increasing from 8% of total in FY12 to an estimated 20% of total in FY21E," he added.

Think: App Store, Apple Music and Apple Pay—not to mention its push into video and print media.

In fact, JPMorgan thinks we could see some new acquisitions by Apple in the near future.

"Apple's interest in entering new end-markets is likely to be evaluated based on the opportunity to offer services on a large installed base," Chatterjee said. "Certain end-markets in our view could be of interest, including gaming services, automotive services, and smart speakers."

The newest edge to the services business that has Apple watchers paying close attention is what Chatterjee calls plans for an “all-encompassing Media subscription”. That would combine video, newspaper and magazine offerings for under $15.

And this is where the next expected acquisition comes into play, too:

"We expect Apple to combine the video and print media offering (through acquisition of Texture) to offer a packaged subscription at $14.99/month relative to $9.99 for Apple Music and drive Apple Music subscribers to upgrade to the packaged subscription, while at the same time growing the subscriber base at a rapid pace," he wrote. "We estimate Apple's incremental media offerings beyond Music to drive an incremental $2.8 billion of revenues by 2025."

And when it comes to Apple’s video service, which will rival Netflix—JPMorgan said earlier this month that it sees the Apple version making more than $4 billion by 2025.

This is no longer a story about a phone, and Apple’s stock shows that there are now plenty of true believers in the upside to come.

By Tom Kool for Safehaven.com

More Top Reads From Safehaven.com: