Over the past few weeks, we have been inundated with countless headlines declaring that this is the best start to the year for US stocks 1998, the best start to the year for global stocks since 1991, the best start for BBB bonds since 1995, and so on. But today's Flow Show report from Bank of America's Michael Hartnett takes the prize: according to the bank's Chief Investment Officer, with commodities annualizing a price return of 84.8% YTD, better than 1973 which was the best year ever for commodities, and more importantly, global stocks are annualizing 67.9%, i.e., better than 1933 which - in the depths of the Great Depression - was the best year ever for stocks, it is shaping up as "the best year ever" for markets.

(Click to enlarge)

Another way of putting it: complacency and euphoria abound. Yet while it would only be logical to take profits amid this wholesale (buyback and short squeeze) stampede, Hartnett notes that it is still early to sell as BofA's "Bull & Bear Indicator" remains unchanged at 4.4. And while it remains a mystery who is buying - with equity funds suffering another $7.7BN in outflows in the latest week (more on this below) - according to BofA it is the latest re-emergence of "green shoots" that is boosting asset prices because consensus positioned for "secular stagnation" (via credit, EM debt & tech) not "cyclical recovery" (via stocks, Europe, financials). It is also the reason why most hedge funds have been trampled by the recent surge higher, which - adding insult to underinvested injury - has seen momentum names crushed.

There is another, much simpler reason why everything continues to levitate: as Hartnett writes, "risk assets have soared because central banks went "all-in"; but we say March 28th marked "peak" in liquidity easing (yields troughed 28th, Kudlow called for 50bps Fed cut 29th, China PMI released 30th)." And with this "peak liquidity" now behind us, it means April is the "beginning of end" for the rally, according to the wealth manager. Related: SEC Releases New Token Sale Guidelines

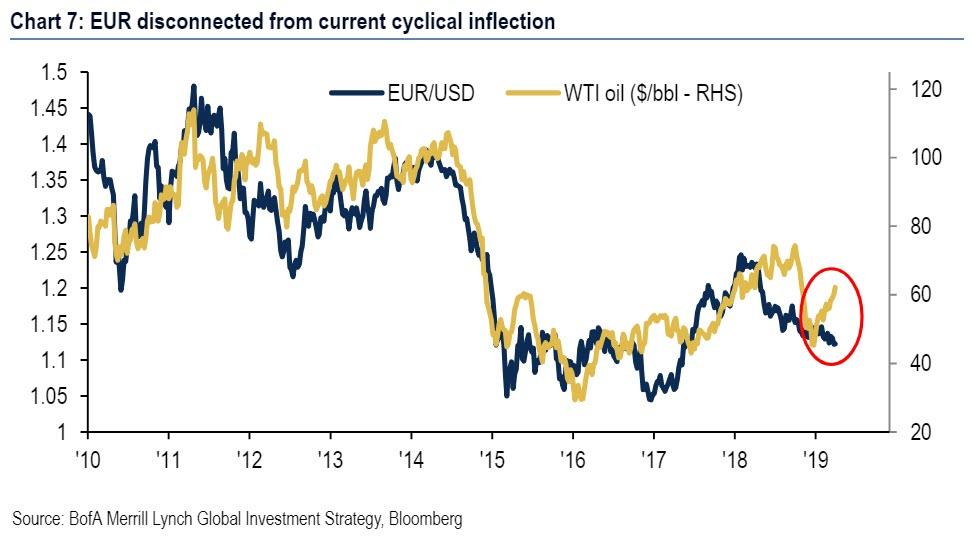

Even so, there is still upside left in stocks, and the bank sees the S&P rising above 3000, driven by oil & banks... although not for long as Hartnett expects the market to top in Q2. Meanwhile, the strategist warns of "secular deflation ghettos", such as Eurozone, "as rent not own as long-term debasement relative to US continues."

And yet, with all that, the paradox we have discussed non-stop for the past 3 months remains: who is buying?

We know who is buying bonds: investors allocated another $7.5BN to IG bonds this week, $1.3bn into HY bonds, $1.3bn into EM debt; we also know who is not buying stocks: investors pulled a total of $7.7 billion from equity funds in the latest week, including $2.6BN out of European equities, and $1.6BN out of US stocks (tech was the only equity sector winner with $1.0BN inflows).

And yet, someone's buying. According to BofA, equity buyers are:

- corporates, also known as "buybacks", which have purchased a record $270BN YTD as of end-March, and

- investors via derivatives (US index delta-adjusted open interest now $446bn vs -$1.2tn at Dec'18 lows, and $916bn at Jan'18 highs). This is the infamous gamma imbalance, where the higher the market rises, the more dealers are forced to buy.

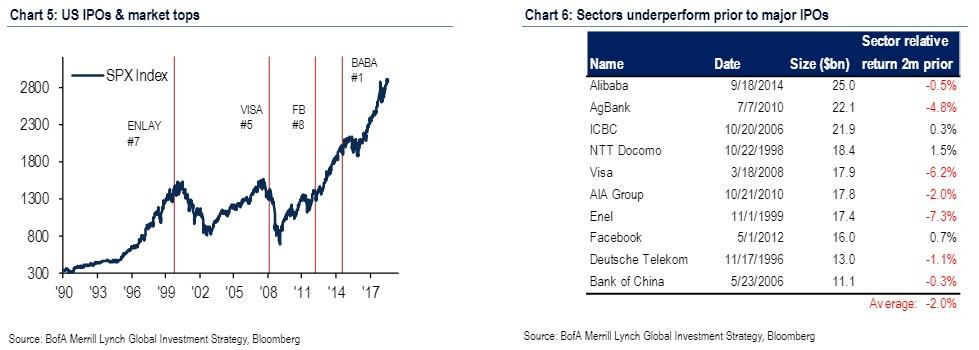

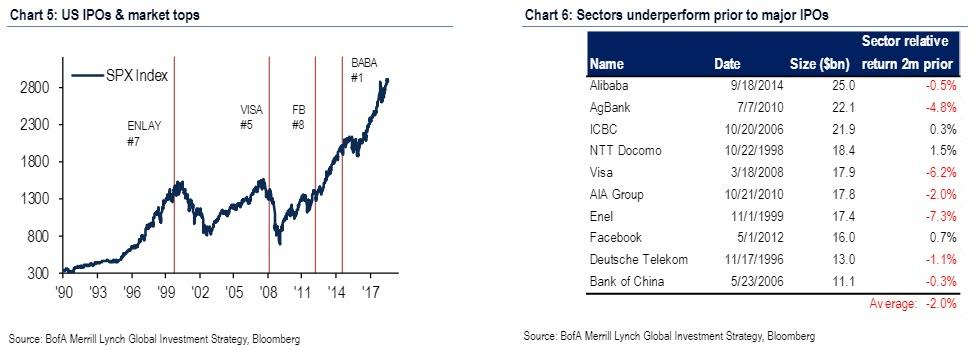

One final observation from BofA, and this time it's on IPOs: the bank notes that there is a "mixed history" with largest IPOs but Alibaba, Visa, Enel, Bank of China, ICBC, NTT Docomo all coincided with volatility and/or market tops; Hartnett also notes 7 of 10 largest IPOs in history also saw their sectors underperform market in 2 months prior as investors raised funds (Charts 5 & 6)

Putting it all together, while stocks may be enjoying the best year in history (annualized), does BofA expect this party to continue? Not at all, and as Hartnett writes in his "Bottom line":

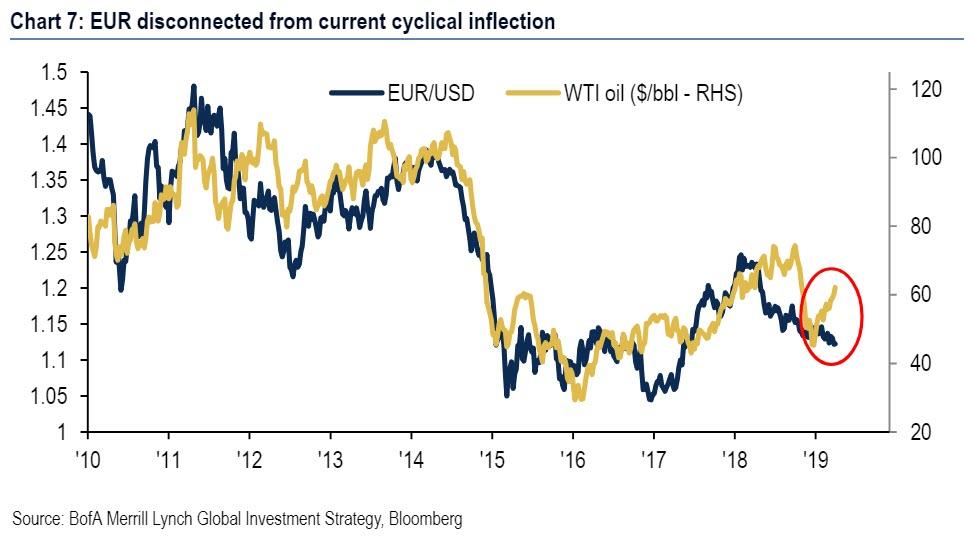

Credit to remain bid, we see SPX >3000 driven by oil & banks, expect "top" in Q2, see secular deflation ghettos such as Eurozone as rent not own as long-term debasement relative to US continues (Chart 7); note EUR now disconnected from positive cyclical signals, such as rising oil prices.

(Click to enlarge)

By Zerohedge

{kind=link}

{kind=link}

{kind=link}