So much for fears the banks would drag down Q1 earnings season.

In a big reversal from the sharp slump in Q4 bank earnings, moments ago JPMorgan put bank stocks on the front foot and saw its stock price surge when it reported revenue, earnings and most importantly FICC profits that beat expectations across the board.

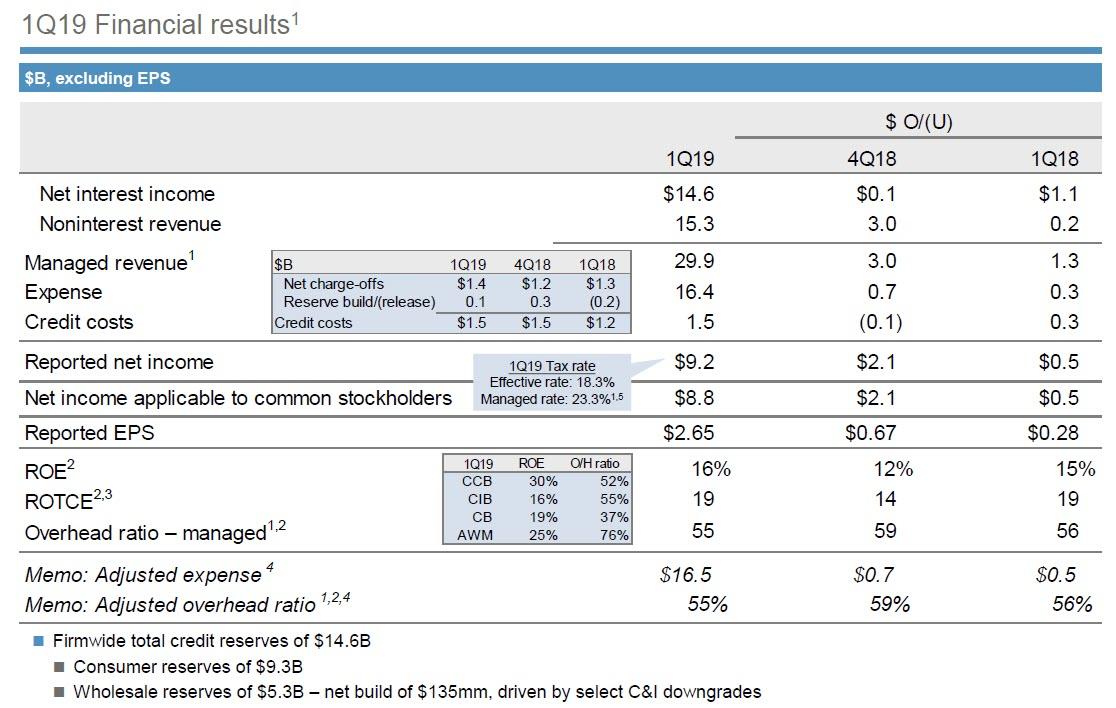

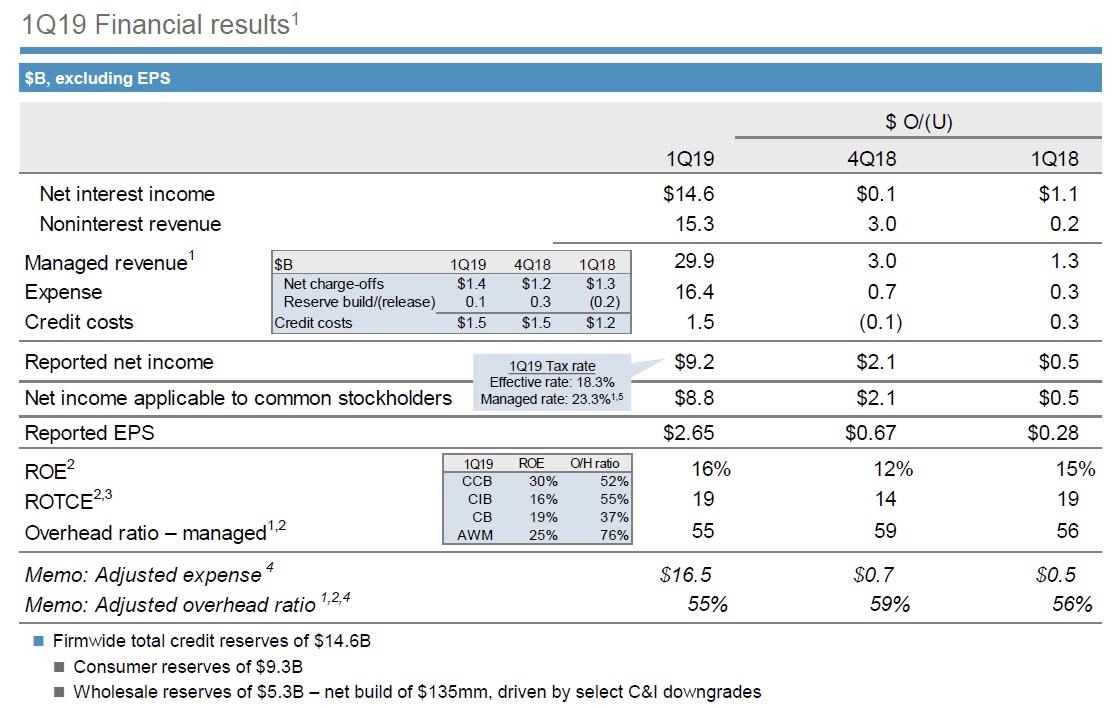

The biggest US bank reported record GAAP revenue of $29.1 billion and "managed revenue" of $29.9 billion, beating expectations of $28.36 billion. This translated into Q1 EPS of $2.65 (and adjusted EPS of $2.60), also handily beating the $2.35 estimate.

Commenting on the results, CEO Jamie Dimon said that "in the first quarter of 2019, we had record revenue and net income, strong performance across each of our major businesses and a more constructive environment. Even amid some global geopolitical uncertainty, the U.S. economy continues to grow, employment and wages are going up, inflation is moderate, financial markets are healthy and consumer and business confidence remains strong."

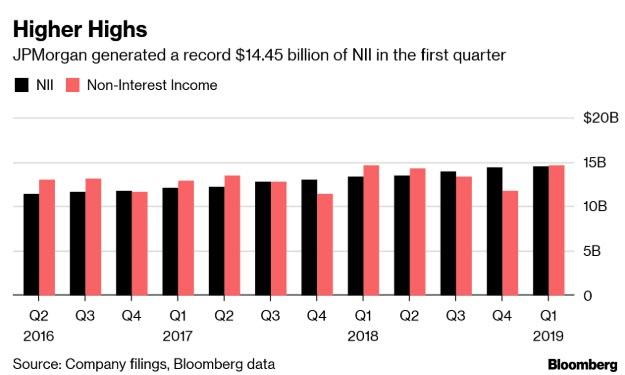

While some were expecting net interest income to drop as a result of the collapse in the yield curve, this did not happen, and in fact, NII rose $100MM from Q4 and $1.1 billion from Q1 2018 to a record (!) $14.6 billion. Again, this comes at a time when the yield curve inverted, which will prompt questions just what is driving JPM's interest income if it's not the shape of the yield curve.

(Click to enlarge)

As JPM wrote, "net interest income was $14.6 billion, up 8 percent, predominantly driven by the impact of higher rates, as well as balance sheet growth and mix." Don't expect this to sustain, however, with the yield curve collapsing and inverting in March and barely rebounding in recent days. Meanwhile, non-interest revenue also increased by an impressive $0.2BN from last year, rising to $15.3 billion.

(Click to enlarge)

Of note, JPM recorded a provision for credit losses of $1.495 billion, just above the $1.487 billion analysts were expecting, and up $330MM from a year ago. JPM blamed the jump in the provision for credit losses on "a net reserve build of $135 million on select commercial & Industrial client downgrades" So look for this question during the earnings call: which clients, as the answer will signal where JPMorgan is seeing stress. Related: Hong Kong Stock Market Surges Past Japan

Looking at the big picture, the bank said its overhead ratio which measures how much it costs to produce a dollar of revenue, dropped to 56 percent, compared with 60 percent in the fourth quarter. JPMorgan said in February it's hoping to get that metric down to 55 percent this year.

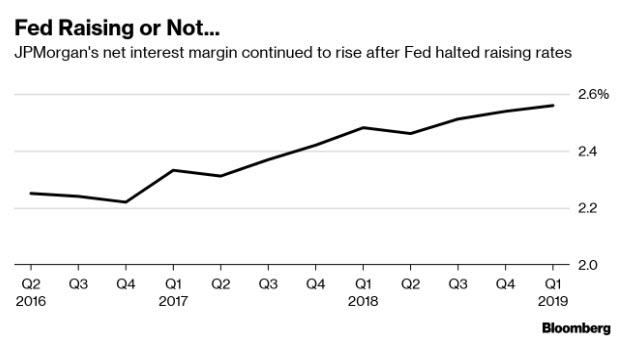

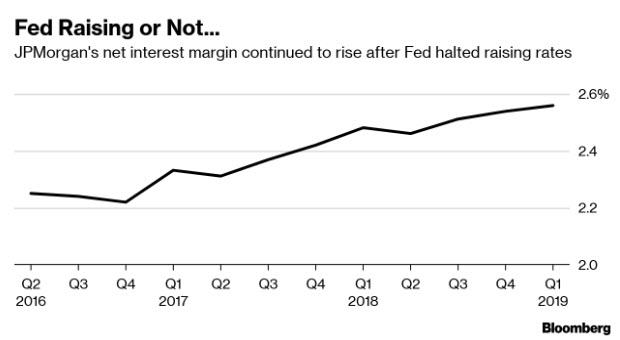

It is also worth noting that JPM's net interest margin climbed for the ninth consecutive quarter to 2.56 percent even as the yield curve inverted, which will likely prompt more questions how the bank managed to offset this move in the bond market.

(Click to enlarge)

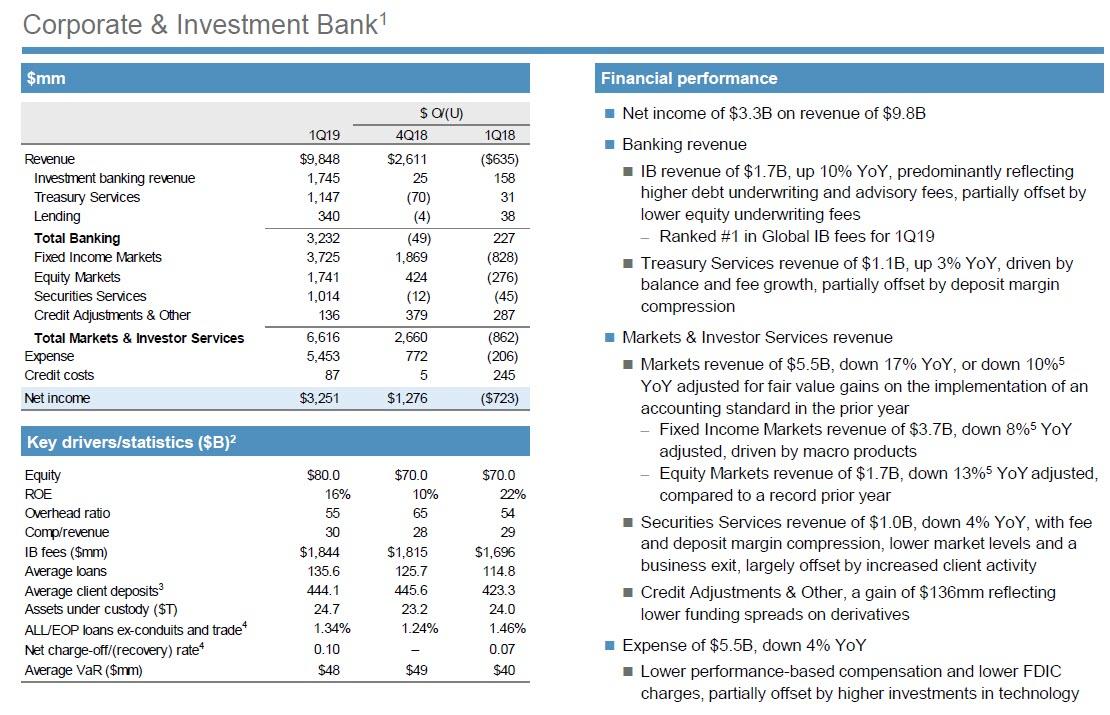

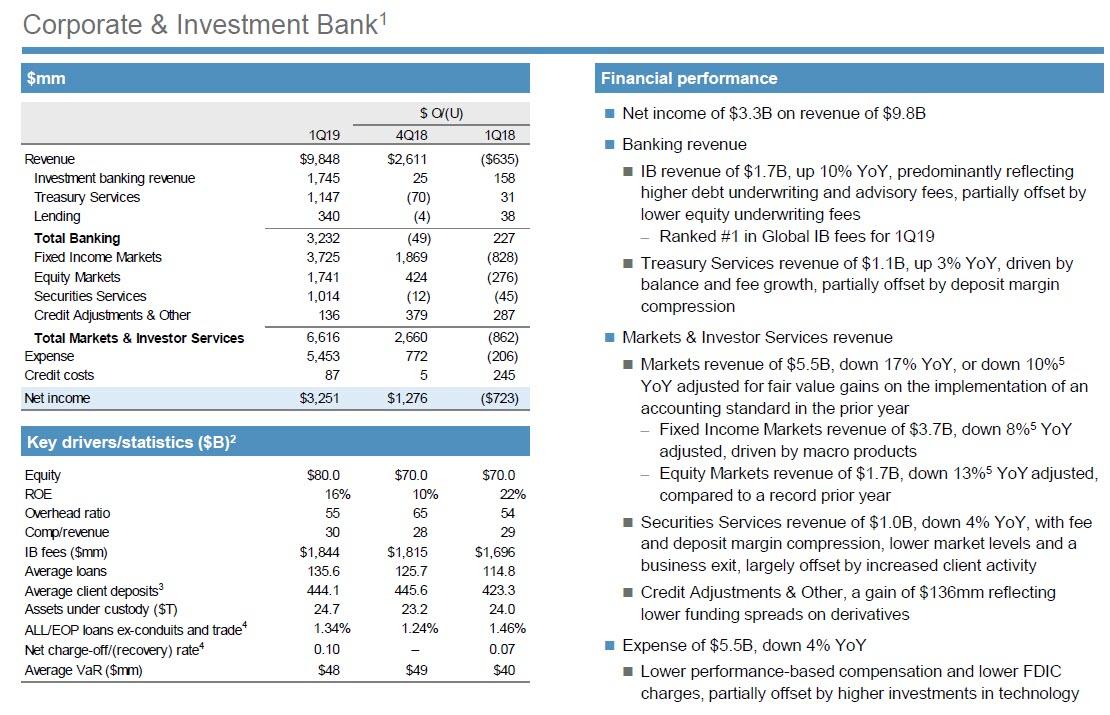

Breaking down the bank's impressive revenue number, analysts immediately honed in on the Investment Banking revenue, which hit $1.75BN in Q1, up 10 percent from a year ago, and roundly beating expectations of $1.63 billion. The jump reflected "higher debt underwriting and advisory fees, partially offset by lower equity underwriting fees."

Also closely watched was the $3.73 billion print in Q1 FICC revenues, which also beat estimates of $3.67 billion. Equity trading did well as well, reporting a solid $1.74 billion, just above the $1.73 billion expected. Still, overall markets revenue of $5.5B, was down 17 percent YoY, or down 10 percent YoY adjusted for fair value gains on the implementation of an accounting standard in the prior year. Overall, despite beating expectations, trading revenues were well below the same period last year, as Fixed Income Markets revenue of $3.7B, was down 8 percentYoY. According to JPM, "fixed Income Markets revenue of $3.7 billion reflected lower revenue in Currencies & Emerging Markets and Rates, driven by lower client activity compared to the prior year, which benefited from a strong performance. This decline was partially offset by improved performance in Credit Trading and Commodities from higher client flows. "

Related: Behind The IMF’s Market-Jolting Doom And Gloom

Equity Markets revenue of $1.7B, was down 13 percent YoY which in turn "reflected lower client activity, predominantly in derivatives. Securities Services revenue was $1.0 billion, down 4 percent, predominantly driven by fee and deposit margin compression, lower market levels and the impact of a business exit, largely offset by increased client activity."

(Click to enlarge)

Commenting on the Investment Banking group, Dimon said "as the environment stabilized, the Markets business performed solidly, although down from a particularly strong prior-year quarter. And Asset & Wealth Management grew AUM 4 percent with continued net longterm inflows."

Turning to expenses, costs rose 2 percent to $16.4 billion, in line with what analysts were expecting. The bank says the increase was driven by investments in technology, marketing, real estate, and front-office hires. Within investment banking, expenses were $5.5 billion, down 4 percent Y/Y due to "lower performance-based compensation and lower FDIC charges, partially offset by higher investments in technology."

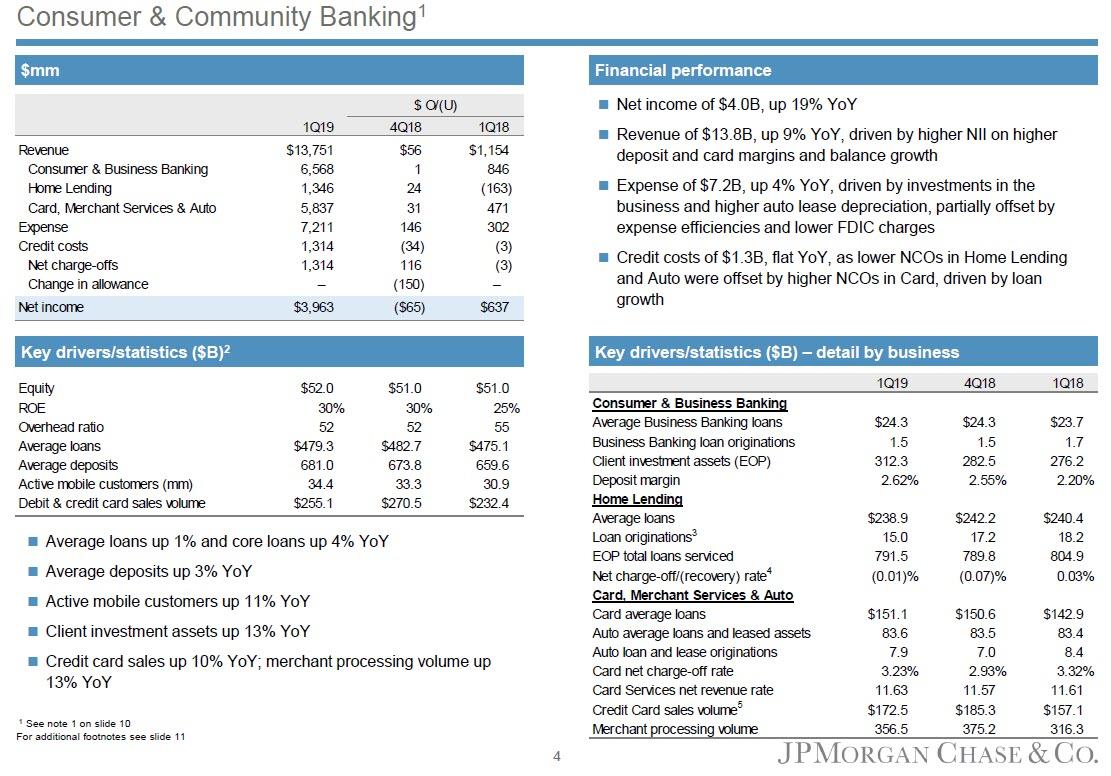

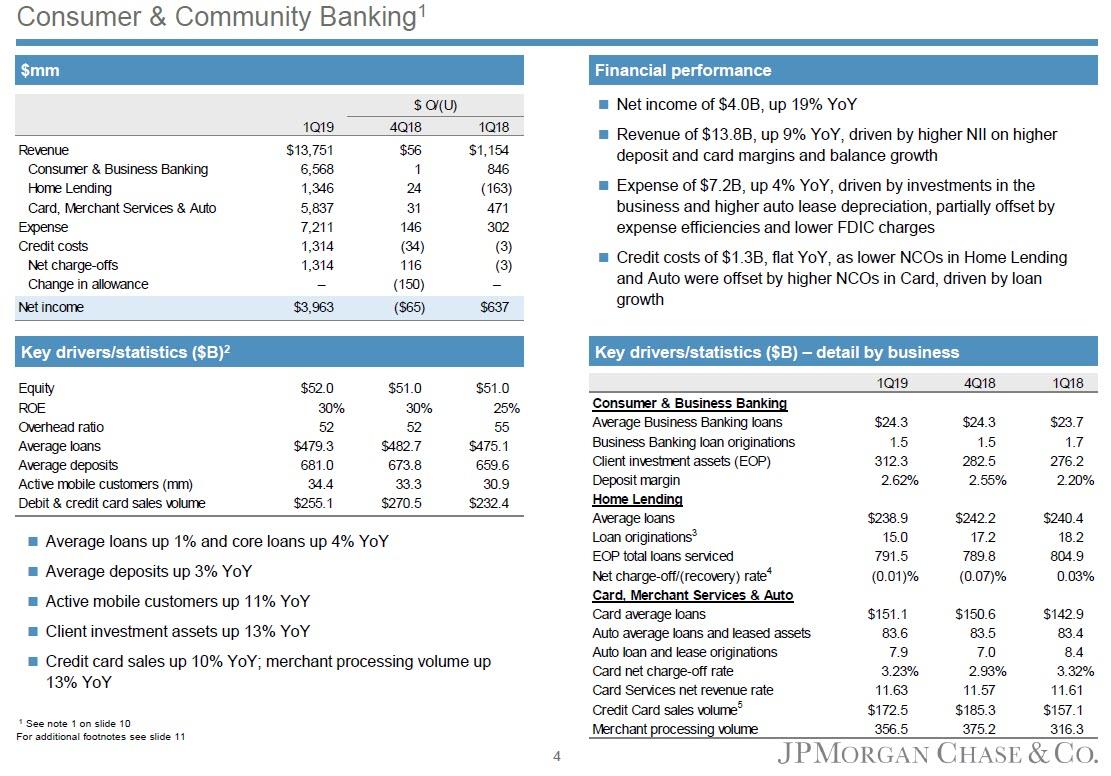

Looking at the bank's core consumer banking group, revenue of $13.8B soared 9 percent YoY, driven by higher NII on higher deposit and card margins and balanced growth. Looking at just consumer and business banking, revenue also jumped a whopping 15 percent to $6.6 billion in the quarter, as average loans increased 1 percent and core loans up 4 percent YoY; at the same time average deposits rose 3 percent YoY. The "card, merchant services, and auto" revenuesweres up 9 percent and the bank attributes that to higher net interest income from its card business and higher auto lease volumes. Home lending was the only disappointment, as revenues dipped $136 million, or 11 percent, from a year ago to $1.346 billion which the bank says is due to lower net servicing revenue.

As revenues rose, so did expenses, which increased 4 percent to $7.2BN, "driven by investments in the business and higher auto lease depreciation, partially offset by expense efficiencies and lower FDIC charges." Charge-offs also increased in the bank's card portfolio, which JPM attributed to growth in the business. That was offset by lower net charge-offs in its home and auto loan portfolios.

Of note here, the bank said that the average it pays on interest-bearing deposits climbed modestly during the quarter to 0.8 percent, compared with 0.72 percent in the fourth quarter and 0.41 percent in the year-ago period. Curiously, the bank said it's still not feeling any pressure to raise the rates it provides on deposits held with the bank. The firm's net interest income rose during the quarter "as a result of higher deposit margins and balance growth."

(Click to enlarge)

Addressing this business, Dimon said that "in Consumer & Community Banking, client investment assets topped $300 billion, with record new money driven by our physical and digital channels. Consumer spending remains robust with credit card sales and merchant processing volume up double digits. We continued to execute on our expansion plans, announcing 90 branches this year in new markets, and creating tremendous opportunities for each of our businesses to better serve our clients.”

Finally, looking ahead, the company provided its brief forecast, noting that it continues to expect net interest income to be above $58 billion for the year, which some noted is a little light. According to Bloomberg, "loan growth coming in on the lighter side and that’s probably a good thing. If we are thinking about being closer to a recession, and late in the cycle, that’s what you would like to see." JPM also expects adjusted expenses below $66BN in 2019, and less than $5.5BN in charge offs.

Not surprisingly, in light of these impressive results, JPM's stock is up 2.5 percent premarket.

(Click to enlarge)

By Zerohedge

More Top Reads From Safehaven.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}