If all goes well for nine more months, the post-financial crisis economic expansion will become the longest economic expansion in recent U.S. history. The U.S. stock markets are also on a tear, having just become the longest bull market since World War II. Regardless of your views about these trends continuing, the fact of the matter is that they are both much closer to ending than a beginning. Ray Dalio recently quantified this continuum, declaring that the economy is in the 7th inning, implying another one to three years of continuation.

While the markets can certainly keep motoring ahead, as Dalio and many others expect, there are some factors supporting the bullish case that investors should contemplate.

While this list is not by any means exhaustive, it does offer many of the most important assumptions supporting the market and some details to provide context and clarity.

1. Corporate managers have become so adept at their jobs that profit margins and equity valuations will remain at, or rise from current nearly unprecedented levels.

Market Cap : GDP – 99% historical percentile according to Goldman Sachs Investment Research (GS)

Enterprise Value-to-Sales – 97% historical percentile (GS)

Shiller’s CAPE 10 – 90% historical percentile (GS)

Price-to-Book Value – 89% historical percentile (GS)

John Hussman’s margin-adjusted CAPE – Record high including 1929 and 1999.

Expected 10 year S&P 500 return as depicted in our article Allocating on Blind Faith is negative

GMO 7-Year real return forecast -4.90% for U.S. large cap, -2.30% for U.S. small cap and -3.80% for U.S. high quality

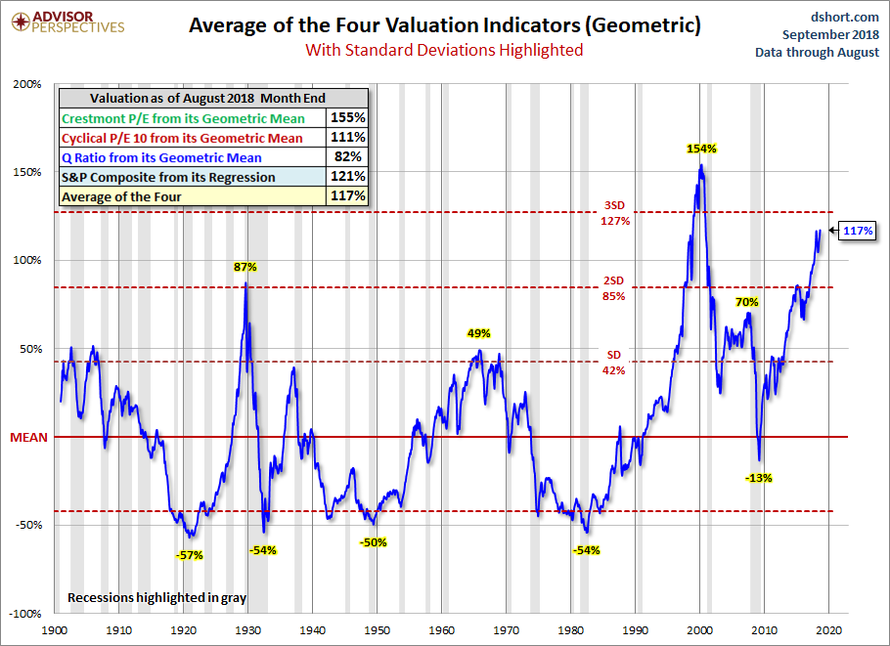

Doug Short’s (Advisor Perspectives) Average of the Four Valuation Indicators is 117% overvalued as shown below and nearly 3 standard deviations from the mean

Related: Hacks, Bugs And Exploits: Growing Pains For The $4 Billion Blockchain

(Click to enlarge)

2. Bond yields will remain historically low and the 30-year downward trend will not reverse

The 10-year U.S Treasury yield is slightly above a key 30-year resistance line at 3.11%

The 30- and 10-year U.S. Treasury yields are testing multi-year highs of 3.23% and 3.12% respectively

Since the lows of 0.70% in November 2016, the 2-year U.S. Treasury yield has risen 300% to 2.80%

3-month LIBOR, a key global interest rate for floating rate financing, has risen 282% from 0.62% in June 2016 to the current level of 2.37%

Implied volatility on Treasury note futures is at historically low levels indicating extreme complacency

GMO’s 7-Year real return forecast is -0.20% for US bonds

3. Future Fed rate hikes and possible yield curve inversion will not cause economic contraction

The Federal Reserve (Fed) currently expects to hike rates an additional 1.50% bringing the Fed Funds rate to 3.50%, by the end of 2019

The 2s/10s U.S. Treasury yield curve stands at 26 basis points and has flattened 110 bps since December 2016

The Fed appears increasingly comfortable with inverting the yield curve “Over the next year or two, barring unexpected developments, continued gradual increases in the federal funds rate are likely to be appropriate to sustain full employment and inflation near its objective.” – Lael Brainard – Fed Governor

The last five recessions going back to 1976 were all preceded by a 2s/10s yield curve inversion

All six recessions going back to 1971 were preceded by Fed interest rate hikes. Two exceptions where rates hike did not lead to recession were in 1983-84 and 1994-95

4. Weakness in interest rate sensitive sectors will not have a dampening effect on the economy or markets

Total automotive vehicle sales have declined 7.8% since the Fed started raising rates

New and existing home sale have steadily declined since November 2017 as mortgage rates risen by over 0.50% over the this period

5. Wage growth will not accelerate further thus stoking inflationary pressures

Employees gaining leverage over employers as jobless claims and the unemployment rate both stand near 50-year lows

Wage growth is at a 9-year high

Spike in the “quit rate” to 18-year high suggests more wage growth pressure coming

6. Annual fiscal deficits over $1 trillion will power economic growth with no consequences

Current deficit equals 4.4% of GDP and is projected to rise to 5.5% in 2019 ($1.2T)

Recent projections of budget deficits have been revised aggressively higher

Interest expense rose 10% this past fiscal year and now accounts for $500 billion spending. To put that in context, the defense budget for 2019 is $717 billion.

7. Domestic political turmoil will not roil markets or inhibit consumer and corporate spending habits

Mueller’s findings

Mid-term elections

The potential for the Democrats to take a majority in the House and/or Senate and advance calls for Trump impeachment as well as impede further tax reform and possibly other corporate-friendly legislation

8. Possible additional U.S. dollar appreciation and the resulting financial crises engulfing many emerging markets will not cause financial contagion or economic slowdown to spread to developed nations or to the world’s largest banks

9. Geopolitical turmoil will not roil markets or stunt global growth and trade

Brexit

Italy

Iran

Russia

Syria

Turkey

Brazil

Argentina

Venezuela

South Africa

Related: Markets Uneasy As Tariffs Take Effect

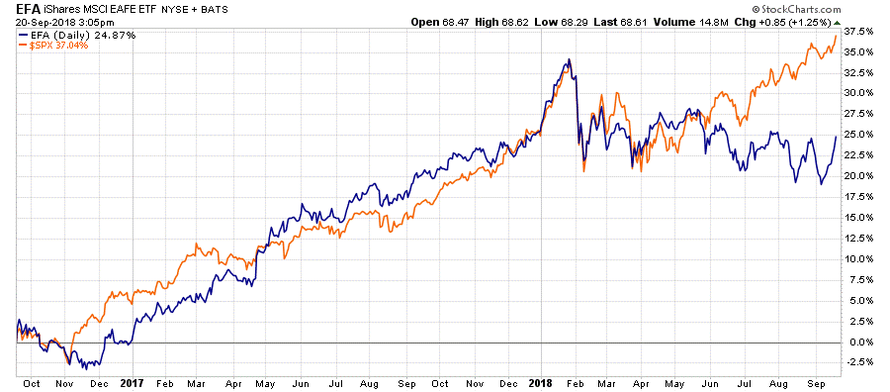

10. The performance of U.S. stocks can diverge from the rest of the world

The following developed markets are all negative year to date and have a 50-day moving average below its 200-day moving average

United Kingdom -5%

Japan -3%

Hong Kong -9%

South Korea -6%

Germany -6%

World Index EFA (blue) vs. S&P 500 (orange) (Graph below courtesy Stockcharts.com)

(Click to enlarge)

11. Trade wars and increasing tariffs benefit the economy and global markets

China

Canada

Mexico

Europe

Japan

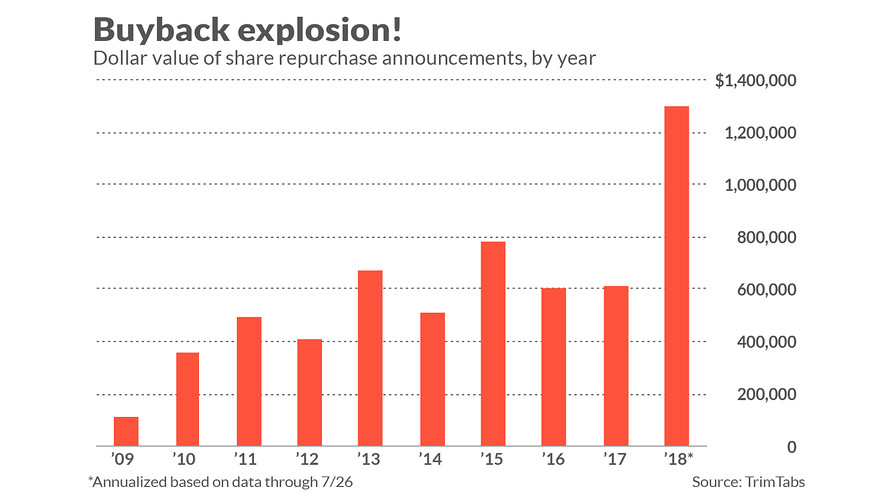

12. Corporations, via stock buybacks, will continue to be the predominant purchaser of U.S. stocks

Buybacks will reach a record high in 2018 (Graph below courtesy Trim Tabs)

Corporate debt can continue to rise to fund buybacks despite rising interest rates and risk of credit downgrades

Corporate debt as a percentage of GDP is now the highest on record

(Click to enlarge)

13. Liquidity in the markets will remain plentiful

14. Central Banks can permanently prop up asset prices if they are to fall

And…The most important factor long-term bulls must assume to be true:

15. This time is different

By Michael Lebowitz via Zerohedge

More Top Reads From Safehaven.com: