Last week, we discussed the fundamental flaw in GDP. GDP is a perfect tool for central planning tools. But for measuring the economy, not so much. This is because it looks only at cash revenues. It does not look at the balance sheet. It does not take into account capital consumption or debt accumulation. Any Keynesian fool can add to GDP by borrowing to spend. But that is not economic growth.

Borrowing to Consume

Today, let’s look at another problem with GDP. To understand it, let’s walk through a plausible scenario. It begins with Johnny Fastlane. Johnny borrows $10,000 on his credit card to (yes, our favorite example) go on a gambling vacation in Las Vegas. An airline carries away some of his cash. A hotel lodges some. A few restaurants eat it. And of course, the casinos roll in his dough.

These businesses make their money (well, irredeemable currency), in exchange for provided services to Mr. Fastlane. They do not know that Fastlane borrowed it. They do not have any way to know it, and they do not care. Cash is cash. They book it as revenues. Fastlane may be leveraged, but they are not—yet.

These businesses pay employees to provide their services. And the employees go home and spend it on food, entertainment, health care, etc. And for their own shelter and transportation, they borrow to pay for houses and cars. Fastlane’s leverage makes possible the leverage of several others. And of course the automaker, realtor, and building contractor have employees whose paychecks come from the revenues generated by the employees of the businesses that serve Johnny Fastlane.

Borrowing to Serve More Who Borrow to Consume

And wait, there’s more. We said the airlines, hotels, restaurants, and casinos aren’t leveraged yet. But they do borrow. Not to overtly consume, as does Johnny their customer. To provide better, more decadent services to win more of his business (and the business of Johnny’s friends Bob Bigshot, Charlie Cashloose, Henry Hedonist, and Pedro Prodigal). They borrow to expand. And they borrow to upgrade.

It’s a falling-interest-rates environment, so credit is plentiful and cheap to any business that has the revenues to service more debt. The airline borrows to buy more spiffy new planes to accommodate the growing demand for travel to Vegas. The hotel borrows to build a more opulent palace, and so on. Those borrowed funds pay yet other businesses, and hire workers. Who borrow to grow also.

This may sound similar to the so-called money multiplier. But looked at objectively, as we have above, we can see that it is utterly unsustainable. There is no theory that can claim this is sustainable, or leads to anything sustainable. The same way that no theory can claim that your month of birth determines your personality, your marriage, and your fate.

Consumption of borrowed wealth is unsustainable. It’s a dead-end, not to mention it leads to other problems such as: how do you repay the debt? The businesses and individuals who receive borrowed capital as revenues do not build sustainable—i.e. wealth-creating—businesses. They may be profitable, but that must be understood in the context that profit means the revenues from Fastlane’s fast consumption of wealth.

A False Profit

For example, if the Bacchus Feast restaurant takes in $1,000,000 of wealth accumulated over centuries by Fastlane’s and Bigshot’s and Cashloose’s families, but it spends only $900,000 catering to their whims, it has $100,000 left over. But what, exactly, is left over? Some of that wealth. This $100,000 represents a bit of Fastlane’s family’s wealth un-consumed. It is not wealth created by Bacchus.

As an aside, yes, some of this may be invested and the entrepreneurs who receive it may create real wealth. This is not proof that the model of incentivizing consumption is sustainable. It means that the process of seeking out capital to consume and destroy was imperfect—it missed some.

Of course, Johnny cannot keep borrowing. What happens when his name is changed to Nocash? And his buddies become Messrs. Bigdebt, Cashtight, Homeless, and Wastrel. When they stop spending like drunken sailors and Prodigal Sons, then the revenues to the airlines, the hotels, restaurants, and casinos dry up.

They must lay off employees. They buy less from their suppliers, who also must lay off employees. Worse yet, they have the debt they incurred when revenues seemed bountiful. That debt will be a burden for a long time to come (even conceding that debt can be extinguished). Related: Americans Are On A Crash-Course With Credit Card Debt

Notice in this scenario, two things have occurred. One, Johnny and his buddies have borrowed and consumed a lot of accumulated wealth. Two, Bacchus and other businesses have borrowed to build capacity that, it turns out, is not needed. The additional capacity is not productive. For both Johnny and Bacchus, the debt lingers long past the fun phase, the consumption of wealth phase. This is phase one.

The Bust

Phase two is the not-so-fun phase. In phase one, we consumed more than we produced (the difference coming from the balance sheet, retained earnings, aka accumulated wealth). Phase two is consuming less, in order to repay debt. So GDP necessarily must drop. At the least, this puts the now-unemployed people under stress for their car loans. And the businesses like Bacchus for their debt to finance capacity they don’t need.

But it gets worse. There is no extinguisher of debt. Debt, on net, cannot be paid off. The dollar is a credit instrument. When debt is paid with an I.O.U., it does not go out of existence. It is merely shifted to another party. So the total debt remains, though the orgy of feasting is long depleted.

So how do you get out of this? And by “you”, we mean the central planners who enabled Johnny to borrow to consume in the first place, with twin policies of first too-low interest and too-loose credit, and second falling interest rates. How are the central banks to fix this problem?

Lower the interest rate again. Rinse, repeat.

Then GDP will go up, and the good times will come again.

Anyways, it is not really our focus today to make yet another argument for why interest rates must fall. Our point was that there is a positive feedback loop in GDP. Johnny’s wealth consumption provides revenues to Bacchus, which borrows to build a soon-to-be-unneeded expansion. And it provides salaries to Bacchus employees who borrow to buy homes and cars, and charge their own vacations to credit cards.

It would be extremely difficult to trace all of this economic activity fueled by Johnny’s and his cohorts’ vacations.

More Positive Feedback

Let’s consider one more feedback loop.

The same uber-loose credit condition that enables people to borrow to consume, also allows businesses to borrow to consume. We don’t mean indirectly, as in Bacchus which has revenues that are apparently (i.e. temporarily) robust. We mean companies who don’t have sufficient profits to pay the interest expense on their debts.

The Bank for International Settlements has a term for such companies where profit < interest expense: zombie corporations. According to their report from September 2018, over 12% of listed nonfinancial firms is zombie.

These are companies which are obviously destroying wealth—they are reporting it openly in their financial statements! Yet investors keep feeding them more capital. There are a variety of reasons why any particular investor would be willing to do this, but they all redound to the central banks.

Consider Vampire Novelty Gift Shoppe. Business is slow, and revenues do not quite cover expenses. But it’s OK, because Vampire can suck more cash out of the bond market, to pay its payroll and rent. The capital it drinks goes to pay its employees as income, their landlords as rent, and their vendors as revenues.

Heck, Johnny Fastlane may even be one of their employees. His Vampire salary may support his credit card (or, at least, convince the credit card companies to extend credit to him). So in this tangle of feedback loops, do we say that Johnny’s capital consumption enables the Vampire? Or that the Vampire’s borrowing enables Johnny’s?

Either way, both contribute to the other. It is a positive feedback loop. While it lasts.

The presence of positive feedback loops—in which unsustainable wealth-consuming activities that add to GDP fuel other unsustainable wealth-consuming activities which also add to GDP—is another reason why GDP is a perfectly terrible way to measure the economy. Of course there is no good way to centrally plan the economy. And this one is a no-good way also. Related: The Stock Market Bulls Still Have Room To Run

Right now, there is an idea promoted by some leading otherwise-free-marketers to centrally plan the economy by having the central bank target GDP growth at the right rate. If any are reading this, our question to you is: what is the right rate for Vampire to borrow to pay Johnny and for Johnny to borrow to go on vacations?

If our economic writings don’t show the world why interest rates cannot be centrally planned, maybe our gold leasing and gold bond markets will (the interest rate is set by the market). We can hope!

Supply and Demand Fundamentals

The price of gold went up another $11, but the price of silver dropped 4 cents.

The gold-silver ratio hit another new high, up another point, though down from Tuesday’s high water mark.

This obviously was not the week that wage-earners increased their money holdings or that institutions expressed a preference for the bargain of silver.

This coming week may be a week that brings news of a trade deal between America and China. If so, one would expect the stock market to rally. And therefore the prices of the metals, gold more than silver in this case, to drop a bit. That raises the question why.

Notwithstanding the paperbug argument that gold is a terrible investment, and notwithstanding the goldbug argument that gold will be a great investment—gold is not an investment. It is money. And silver too.

One holds money if one expects investments to have a negative return.

So, when the stock market and property market turns (when, not if) this is a likely driver for people in general to turn to the monetary metals as a safe haven. Arguably they have, already, which is why gold is $1,400. But while there is near-ubiquitous faith in the stock market, there may not be aggressive pursuit of gold.

When, not if.

Monetary Metals is excited to be bringing the first gold bond to market. Please contact us if you are interested in investing.

(Click to enlarge)

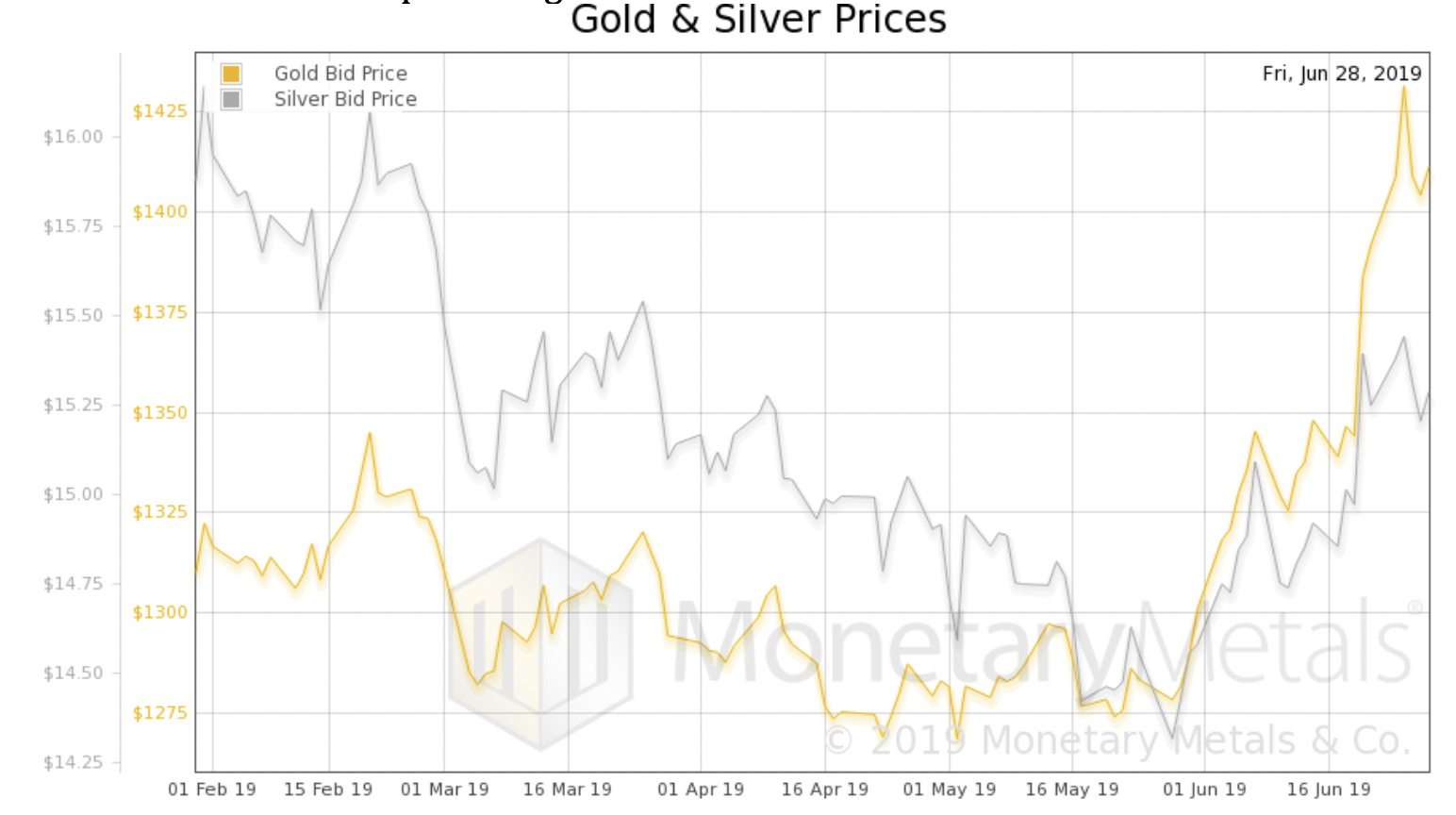

Now let’s look at the only true picture of supply and demand for gold and silver. But, first, here is the chart of the prices of gold and silver.

(Click to enlarge)

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio). The ratio rose further.

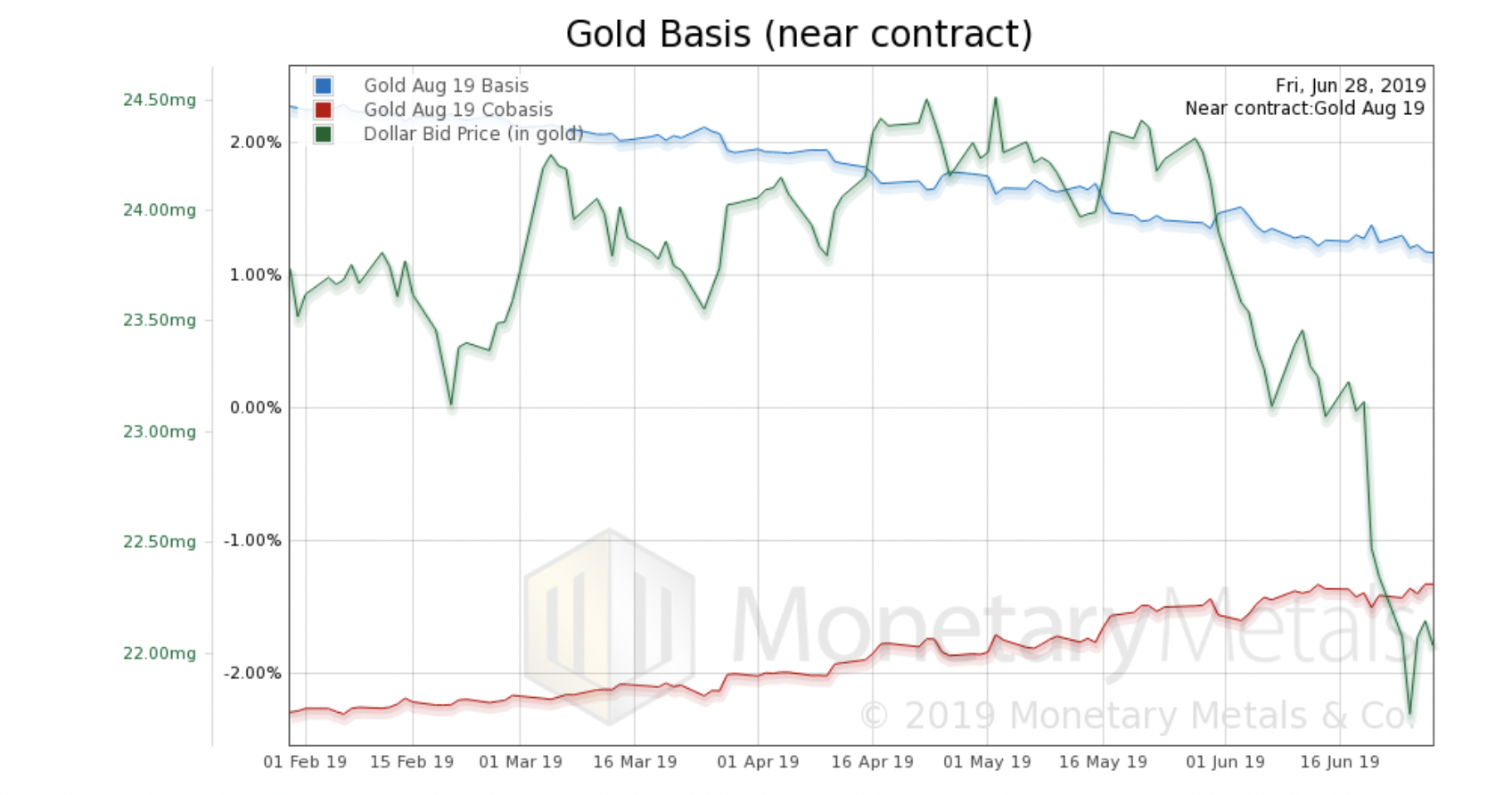

Here is the gold graph showing gold basis, cobasis and the price of the dollar in terms of gold price.

(Click to enlarge)

In light of the continued drop in the dollar (i.e. rise in the price of gold in dollar terms), the drop in gold’s scarcity (i.e. cobasis) looks modest indeed.

The Monetary Metals Gold Fundamental Price rose another $22 to $1,462.

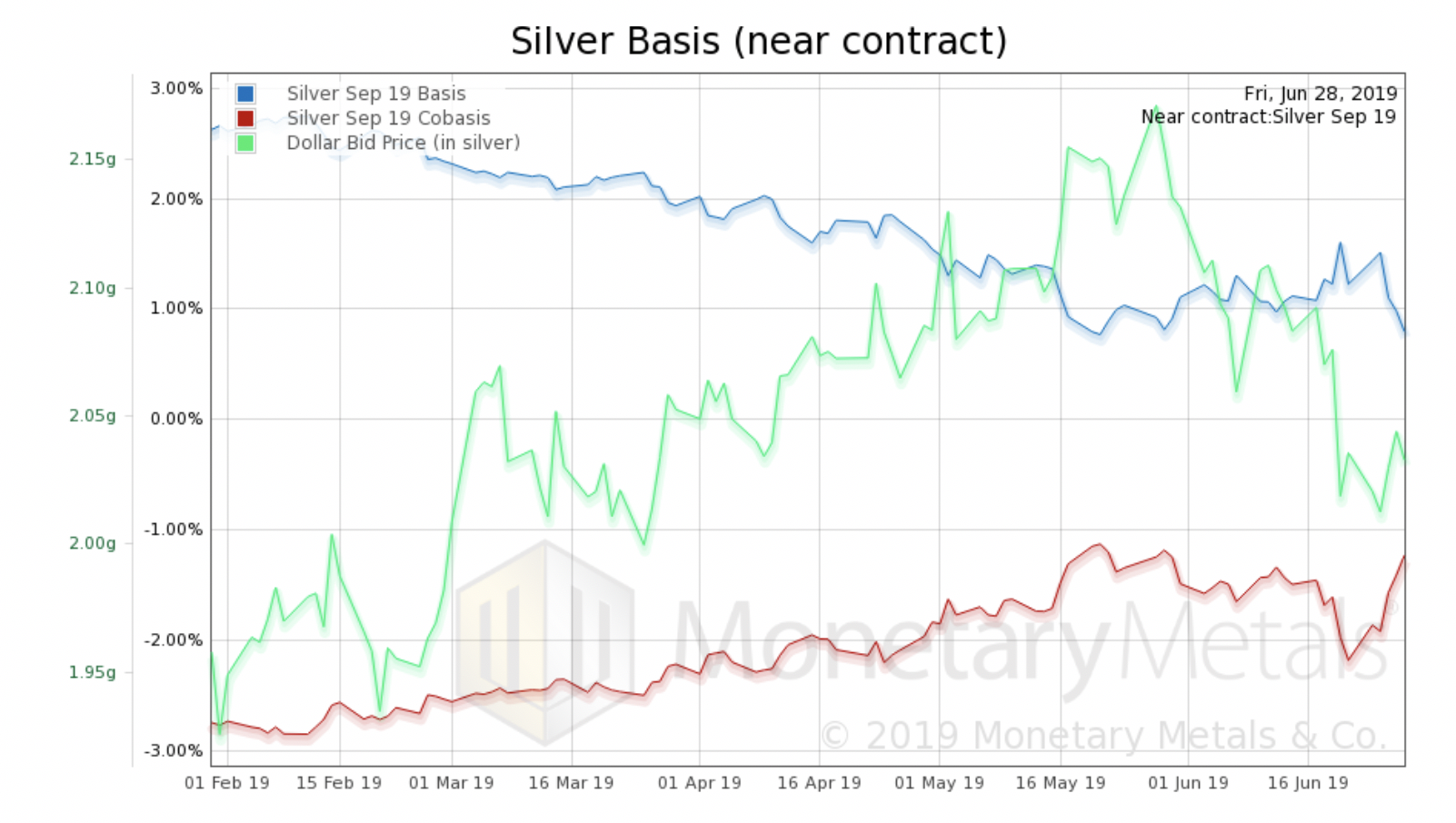

Now let’s look at silver.

(Click to enlarge)

With silver, we can see the scarcity following the dollar price. That is, silver becomes scarcer when it sells, and more abundant when it is bid up.

The Monetary Metals Silver Fundamental Price rose 23 cents to $15.74.

Although the market gold-silver ratio rose, the Monetary Metals calculated gold-silver ratio barely budged.

By Keith Weiner

More Top Reads From Safehaven.com: