Generation rent is showing no signs of changing its ways.

According to RentCafe's year-end rent report for 2019, the national average rent capped off another year of strong growth by leveling off in December. But all evidence suggests that the average national rent will continue moving higher - despite all official gauges of inflation reflecting little or no inflation - as popular sun-belt cities like Phoenix and Las Vegas take over from Brooklyn and California as the biggest drivers of higher rents.

This comes as more Americans are leaving places like California and New York for the sun belt, where rents are relatively inexpensive, jobs are plentiful and the weather is far more temperate.

Nationally, the average apartment rent climbed to $1,474 in December, a 3 percent YoY increase (the slowest in 17 months). Dollar-for-dollar, renters are currently paying, on average, $43 a more per month than they were at the end of 2019. By comparison, the average rent increased by $45 between 2017 and 2018. After years of torrid growth, it's no surprise the pace of rising rents has slowed: with wages still stagnant, many renters are reaching the upper bounds of what they can afford.

That rents are still climbing is remarkable, in part because developers building rental-focused buildings added 2.4 million apartments to the national inventory over the last decade. This, despite a shortage of single-family homes, as homeownership rates among millennials remain ten percentage points lower than Gen X, or even more. Related: The Modern History Of Financial Entropy

As we mentioned above, rents in the sunbelt saw the biggest gains last year, led by Phoenix ($1,123), where rents increased by 9.6 percent, or $98. Second was Las Vegas ($1,107), which notched a 6 percent gain. In third place came Austin ($1,436), where rents tacked on another 5 percent, or roughly $68.

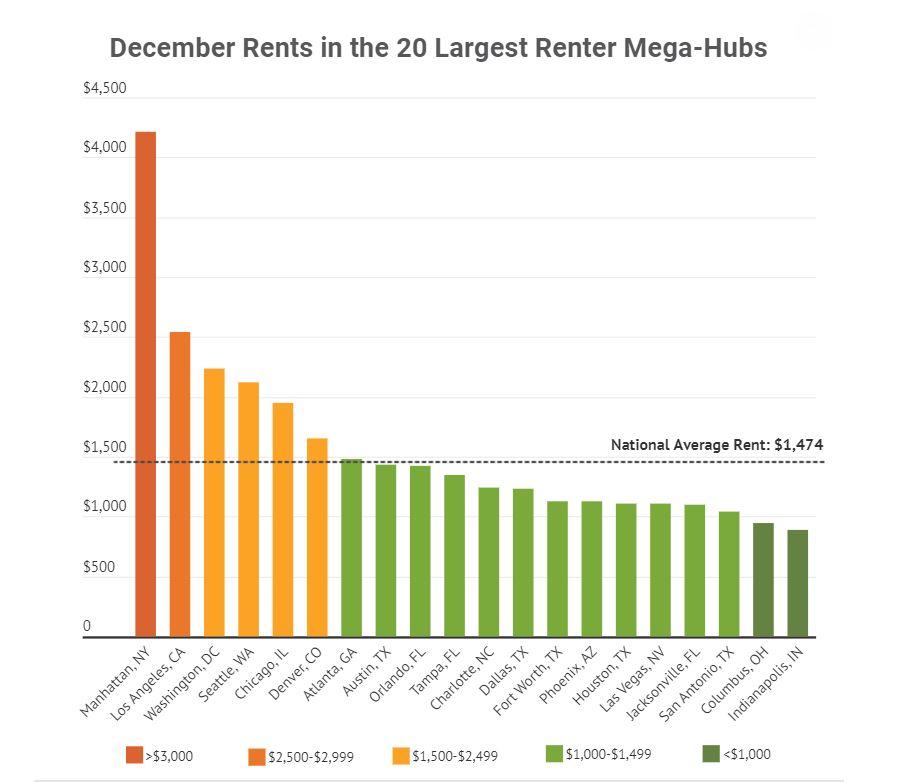

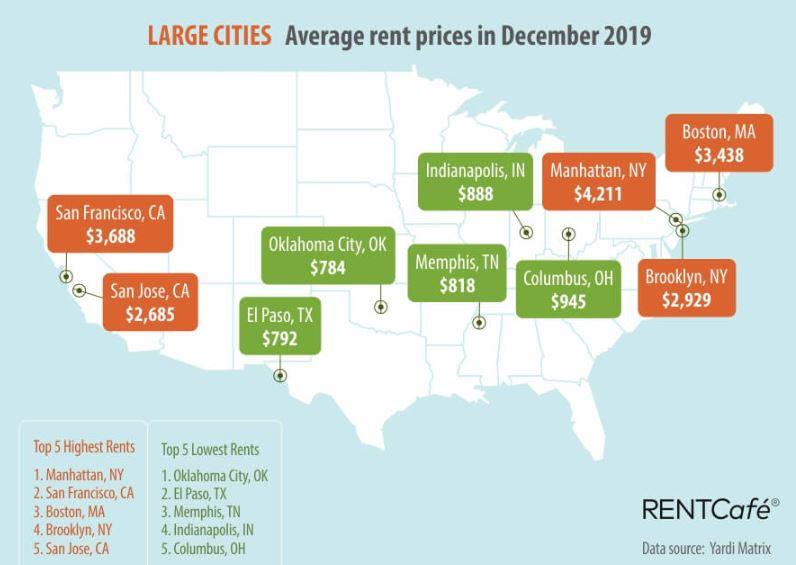

Unsurprisingly, Manhattan remained the priciest rental market in the country in 2019, with an average rent at year-end of $4,211. San Francisco came in second at $3,688 and Boston third at $3,438.

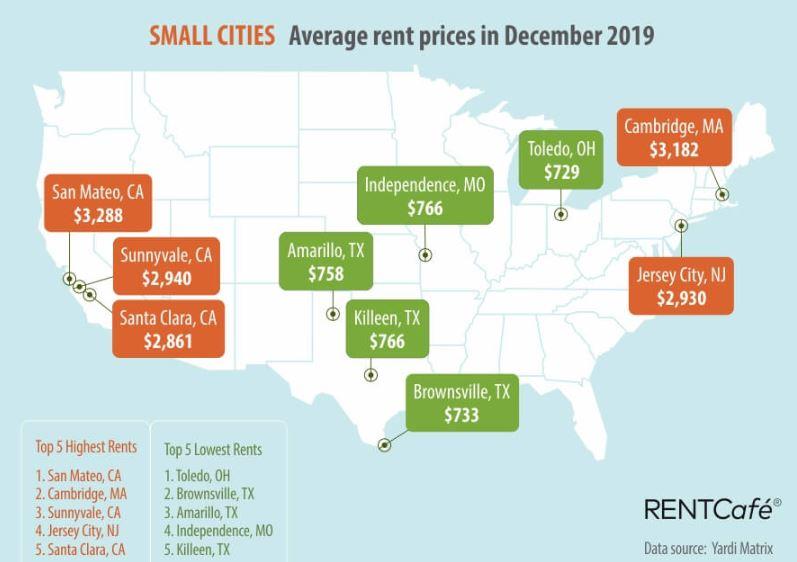

On the other end of the spectrum, Toledo, Ohio, displaced Brownsville, Texas, as the most affordable small city for renters. Average rent in Toledo is just $729 a month.

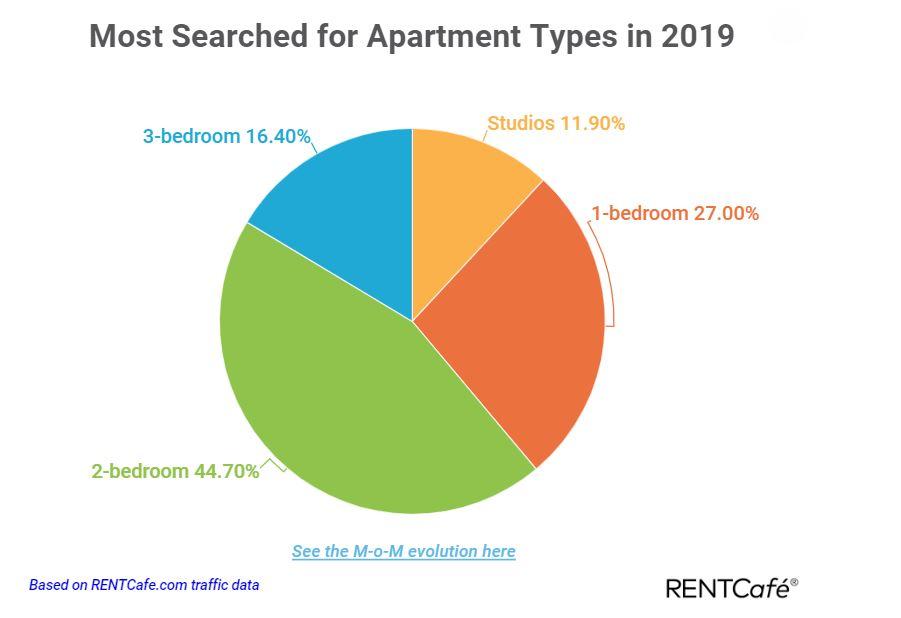

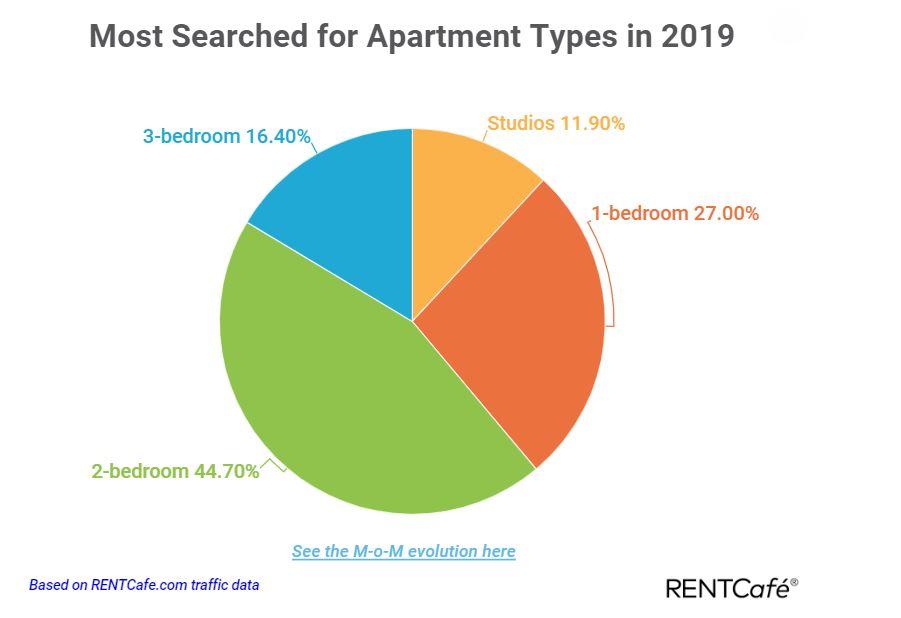

A plurality of renters last year searched for a 2-bedroom apartment, as many millennials remain unmarried and childless heading into their 30s.

If you're curious to see what the average rent was last year in your city, RentCafe maintains an average price interactive on its site.

By Zerohedge.com

More Top Reads From Safehaven.com:

{kind=link}

{kind=link}

{kind=link}

{kind=link}