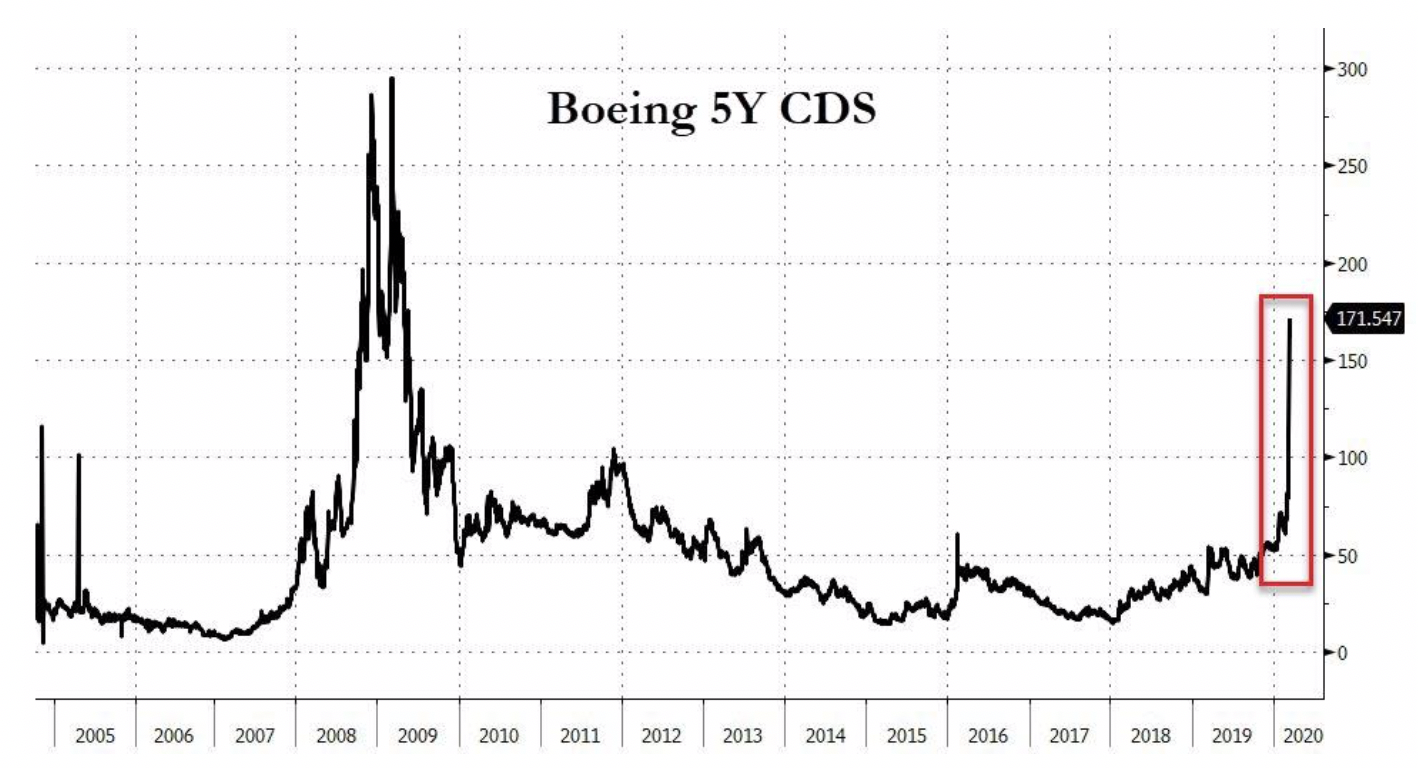

Earlier today, Zerohedge reported that Boeing shocked the investing community when it announced that due to "market turmoil", it would immediately draw down on its full $13.825 revolving credit facility, an unprecedented move for a company Boeing's size and valuation, and one which was some took as an indication of how frail Boeing's liquidity state was, ostensibly confirmed by Boeing's surging default odds measured by its 5Y CDS.

(Click to enlarge)

We disagreed: after all, why would Boeing rush to draw attention to its own funding challenges by fully drawing on its revolver when it knew full well that it had access to the money, safe and sound, located at its syndicate banks... unless of course Boeing was in fact worried about the viability of said banks. AS a result, we said that the real reason Boeing did what it did was simple, especially to those who recall what happened in 2008 all too well: Boeing is worried that banks will pull their committed funding, which in turn means that Boeing appears to be worried that a 2008-style financial crisis is imminent, and is shoring up all the liquidity it can, so as not to remain at the mercy of its banks which may refuse to extend it credit at any one moment if their own liquidity is threatened.

Which is why we also concluded that now that Boeing, "one of America's most valuable companies, has shown which way the wind blows, expect thousands of less creditworthy companies to follow suit as they scramble to cash in on every dollar in available revolver funding before the banks pull it."

We had to wait just a few hours for this prediction to come true, because later on Wednesday, Bloomberg reported that two of the world's biggest PE firms, Blackstone and Carlyle, have told their portfolio companies to immediately do what Boeing did earlier in the day: "Do whatever it takes to stave off a credit crunch", which as in the case of Boeing, is a polite way of saying: your banks may pull their liquidity (i.e., fail), so get whatever cash you can now when you can, and not when you have to. Related: How One Country Saved Itself From The Oil Price Plunge

According to the report, the dozens if not hundreds of businesses - all smaller than Boeing of course - controlled by the PE titans are joining a growing wave of corporations drawing down bank credit lines to help prevent any liquidity shortfalls amid signs of mounting stress in markets. At Blackstone, which has weathered a variety of crises in its 35 years, the focus is on sectors hurt by the coronavirus, such as the hospitality industry, as well as energy firms facing a slump in oil prices.

At Carlyle the measures aren’t quite as widespread yet, although the firm has been having broad discussions with management teams at portfolio companies and recommended drawing credit lines in certain instances, with the "decisions are based on industries, regions and other factors."

Besides Boeing, Blackstone and Carlyle, other companies that announced plans to drawdown on their full revolver were Hilton Worldwide and Wynn Resorts, all reflecting the uncertainty coursing through corporate America as the US economy hurtles into recession.

Think of it, as companies lining up at their favorite ATM machine to pull all the money that is in the account. It works until suddenly it doesn't.

And here is Bloomberg confirming, through clenched teeth, what we said earlier: "A sudden and sustained increase in companies tapping credit lines could eventually strain banks if conditions become so dire that borrowers won’t be able to meet their obligations."

See, it's not market conditions, but a loss of faith in the banking sector, and the reason why it was so difficult for Bloomberg to admit it is that while toilet paper runs do not lead to a collapse of the financial system, fiat paper runs to, and all that would take for those to begin is a loss of faith in the US banking system.... just like that exhibited by Boeing and some of the smartest financial professionals in the world. Related: Millennials Are Killing The McMansion

The big irony, of course, is that by pulling down on revolvers en masse, US companies can trigger just the liquidity crunch they are seeking to protect themselves again, because as we noted earlier, liquidity in the US financial sector is already dismal and getting worse with every passing day, hence today's latest expansion to the Fed's repo capabilities among a surging FRA/OIS spread.

As Bloomberg explains, "lenders offer revolving credit lines to strengthen relationships with companies and don’t typically intend for them to be drawn upon en masse."

In normal times, revolvers serve as the corporate equivalent of credit cards, giving companies room to borrow as needed and repay when shortfalls ease. Under normal circumstances, the lines are seldom maxed out. Extensive use can be seen as a harbinger of distress."

The fact that everyone is drawing down on their revolver, however, shows three things:

- these are not normal circumstances

- the US financial situation is on the verge of distress, and

- they remember what happened in 2008, when one bank after another collapsed the availability on their revolver to troubled companies and sectors, and this time it will be the banks left with holding the short stick.

That said, oil and natural gas companies are under particular focus as they tend to suffer a spike in funding stress when prices fall, because their credit lines are periodically updated based on market prices, motivating companies to tap them early.

But why Boeing? The company's cash flow is one of the most stable in the world... except of course when a global viral pandemic and its ongoing 737 MAX fiasco has sent its cash flow plunging to the most negative levels in decades.

Meanwhile, Blackstone’s private equity operation is the firm’s largest business by assets, at $183 billion, of which energy accounts for almost 10% of the total portfolio.

Blackstone won't be the last as rival private equity firms - many of which have purchased shale companies in recent years funded with staggering levels of junk debt - also are weighing similar actions.

"From an economic perspective, the virus has created dislocation in the market and fear among the people," Blackstone co-founder Stephen Schwarzman said in an interview in Mumbai last week. “Once that starts, one has to find the impact of negative consequences. But the turbulence can also have an upside for firms with a war chest, he said.

"It creates a substantial opportunity to buy assets and give credit." Or, in the case of Blackstone's portfolio companies, to take it.

By Zerohedge.com

More Top Reads From Safehaven.com: