While economists, having finally taken the threat of trade war seriously, are trying to calculate whether a worst case scenario in the Chinese trade war would be deflationary, inflationary or, as Goldman and Nomura warn, stagflationary, they are now scrambling to catch up what every new additional front in the global trade war means for risk assets.

Naturally, the big question is what Trump's latest threat of hiking Mexican export tariffs will mean for both economies, and for the US stock market in particular. Commenting on this eventuality, Goldman's economists write that a trade war with Mexico, which accounted for 14% of US goods imports in 2018, poses a risk to both corporate profit margins and the health of the US consumer, who will likely absorb the majority of the tariffs via higher prices.

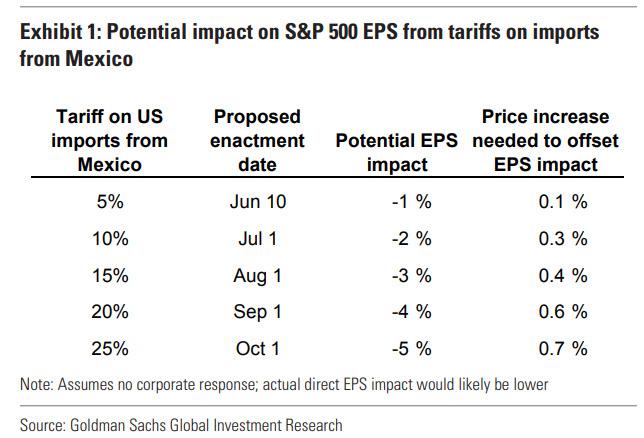

Specifically, Goldman's political economists believe that at least the first 5% tariff on imports from Mexico (out of a total of 25%) planned for June 10 will be implemented. They also highlight the categories of goods that account for the highest share of imports from Mexico, China, and the two countries together. Notably, they show that the combination of proposed tariffs on China and Mexico imports would result in roughly 80% of some US imported products being subjected to tariffs, including toys, cell phones, and other consumer electronics.

That's in theory, what about in practice?

According to Goldman's Ben Snider, while the proposed tariffs pose only a small direct risk to total US corporate earnings, the downstream effects could be jarring, and he estimates that each incremental 5% tariff on all imports from Mexico could lower S&P 500 EPS by approximately 1%, or slightly less than $2, if companies absorb the entire increase in input costs. That said, from a price offset standpoint, the fallout would be manageable as firms would have to raise prices by less than 1% to offset even a full 25% tariff on all imports from Mexico. Similarly, Goldman expects that higher prices and restructured supply chains would offset much of the direct potential risk to S&P 500 profit margins from tariffs on imports from China.

However, the danger is that the earnings risk to companies directly exposed to trade with China and Mexico is much larger, according to Goldman.

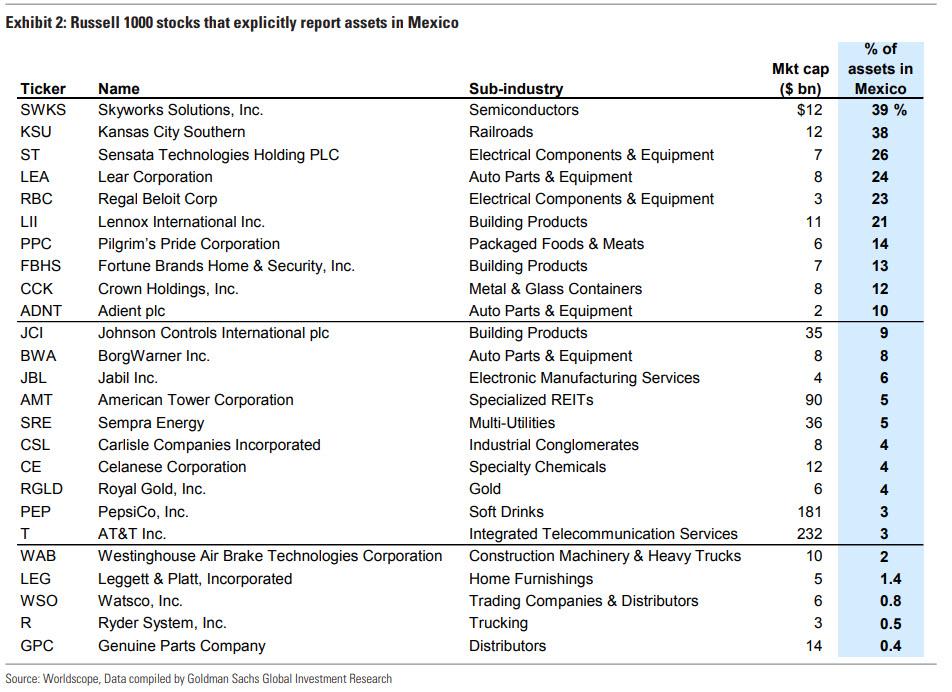

Predictably, investors were quick to whack markets after the Mexico tariff news. In an attempt to narrow down where the most pain could emerge, the chart below shows Russell 1000 stocks that explicitly report assets in Mexico. Here, Goldman clarifies that not all of these firms will be affected by the proposed tariffs, and many firms that do face risk from the tariffs – including those that do not explicitly report assets in Mexico – are absent from this screen. However, the average stock on the list lagged the broad Russell 1000 by 200 bp on Friday.

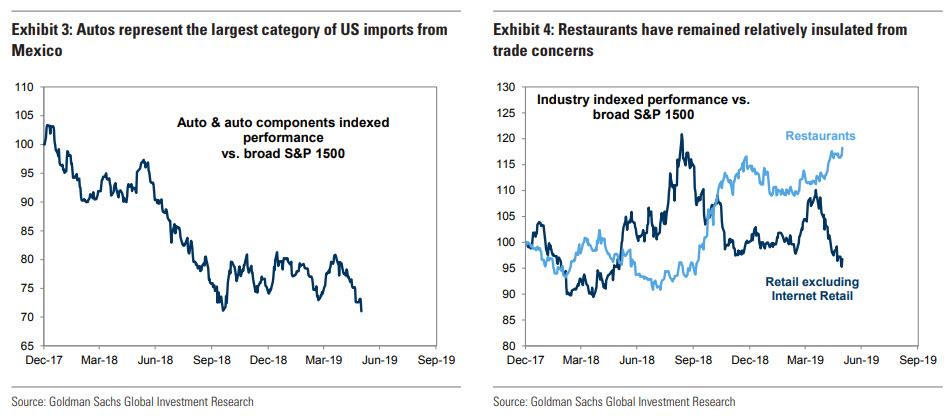

Meanwhile autos and auto components, which represent the largest US import from Mexico, have suffered even more, lagging the broad market by nearly 300 bp.

Related: Is Asia About To Create Its Own Common Currency?

In addition, Goldman sees the tariffs posing a risk to restaurants, although stock prices indicate a lack of investor concern:

"Restaurant stocks have been relatively insulated from trade conflict in recent weeks, particularly relative to retail firms, which are more directly exposed to goods subject to tariffs on China imports. Restaurants continued to outperform today. However, Mexico represents the largest source of US agriculture imports, adding direct risk to restaurants should the import tariffs be implemented. In addition, the broad impact of incremental import tariffs on the US consumer should affect spending on dining as well as goods like consumer electronics."

And since tariffs on imports from Mexico reduce the likelihood of USMCA passage, Goldman suggests that companies reliant on supply chains in Canada will also suffer. And speaking of USMCA, Goldman's economists believe the implementation of tariffs on Mexico "would cause both House Democratic leadership and Mexico to slow their consideration of USMCA, lowering the odds of enactment this year" as we reported a few days ago.

Unlike Goldman, Citi has a much more sanguine take on any potential trade war with the southern US neighbor for the simple reason that consequences of new U.S. tariffs on Mexican imports would be "so extreme that its implementation is unlikely." according to analysts Sergio Luna, Cesar Rojas, Adrian de la Garza and Ernesto Revilla.

According to Citi calculations, Mexican GDP losses could range from 0.9% with a 5% tariff to a whopping 4.6% with a 25% tariff, while retaliation would mean a far more modest 0.04% to 0.4% less growth in U.S. respectively. As a result, if adjustment takes place via prices, in the case of 5% tariffs, the MXN would need to depreciate between 8.3% and 8.6% with retaliation. Amazingly, if a 25% tariff is implemented, the MXN would need to fall between 42% and 59%. And, echoing Goldman, Citi expects that tariffs would have an inflationary impact both in the U.S. and Mexico.

A last point to consider is that the political considerations ahead of 2020 presidential election would lead Trump the administration to take a harder stance on trade - such a strategy may backfire as Mexican demand is relevant for Republican border states.

* * *

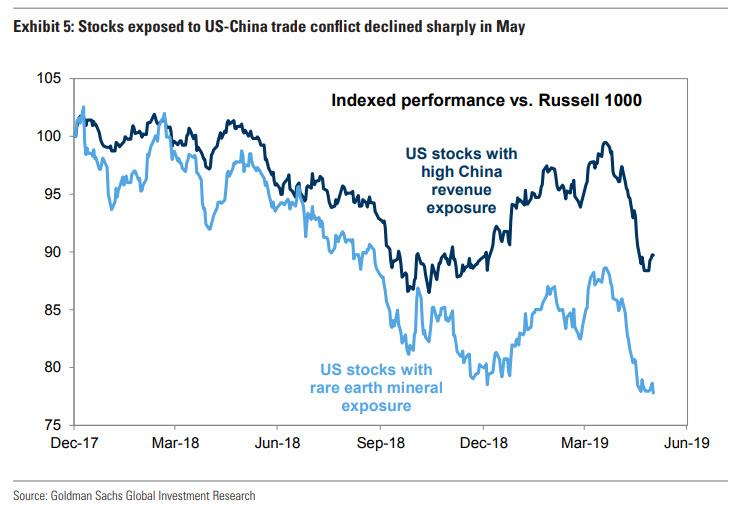

Finally, don't forget that as Trump seems intent on engaging in trade war with virtually any nation that presents an obstacle to the pursuit of Trump's presidential agenda, and while investor focus has turned to the Mexican front of the trade conflict, tensions with China continue to rise. As a result, large-cap stocks that have disclosed exposure to rare earth minerals as a risk within the last three years have sharply underperformed the market in recent weeks, as have US stocks with high reported revenue exposure to China.

By Zerohedge.com

More Top Reads From Safehaven.com: