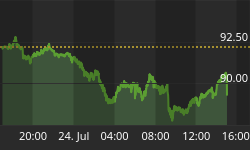

Emerging markets have been red-hot in the Jan 2016-Jan 2018 period, as evidenced by the large emerging markets-tracking ETF EEM, which managed to nearly double over that time span. But these days, investors are no longer so besotted. EEM has plunged more than 10 percent in the year-to-date, in sharp contrast to many developed markets, including the U.S. and Europe, which continue to soar.

(Click to enlarge)

Source: CNN Money

For years, the U.S. dollar has been used as a global carry currency that traders could borrow due to its low interest rate and use the funds to buy other currencies paying higher rates. Emerging markets with a currency peg gradually became a welcome destination for U.S. investors starved of decent yields—not to mention a welcome source of yield differential pick up.

But that lucrative trade came crashing down when the Chinese started devaluing the yuan in 2015 thus sending the U.S. dollar surging and slamming EM currencies.

The unfortunate trend has continued in the current year with the dollar strengthening even further as geopolitical turmoil and instability in EM markets in China, Turkey, Argentina, North Korea, Iran and Russia helped reinforce its safe-haven status.

Many pundits have called for calm, saying that a spillover into the developed markets is unlikely. But Morgan Stanley isn’t buying it. The real pain, they say, is still coming.

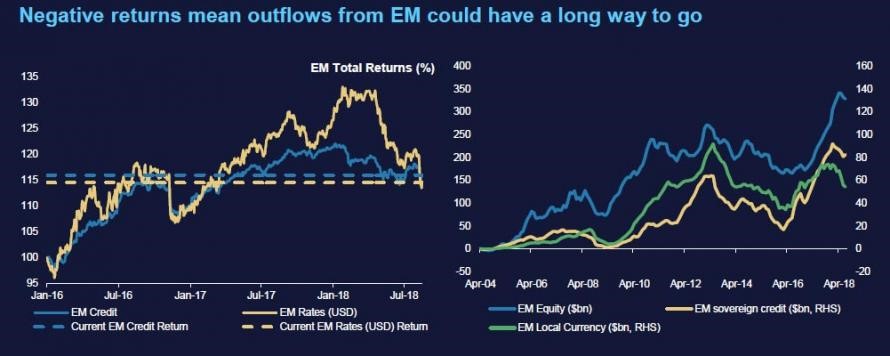

Despite the disappointing EM returns, capital outflows have a long way to fall before catching down to recent returns:

(Click to enlarge)

The same case applies to EM stocks, which have some distance to fall before catching down to EM bonds as depicted in the Templeton EM Bond Fund chart below:

(Click to enlarge)

Slowing Capital Inflows Pose Major Risk

A more salient point is that slowing capital inflows pose a big risk to EMs in general. Consider that a huge influx of foreign capital has been largely responsible for the outperformance by EMs. But we are now observing a trend where less and less money is flowing into developing markets.

Global flows of foreign direct investment (FDI) plunged 16 percent in 2017 to about $1.52 trillion, with a slowdown in FDI flows to developed economies emerging as a worrying trend. Related: Citigroup Is Betting Big On This Sci-Fi Technology

So, what happens when capital inflows to EMs stop--or worse, completely reverses? Things could get pretty dicey.

Morgan Stanley uses a proprietary metric gauge which EM countries are at highest risk of suffering a meltdown due to a catastrophic drying up of foreign investments, as ZeroHedge reports.

Morgan Stanley’s “external coverage ratio” divides a country’s total reserves by its external funding needs (the sum of current account, short-term debt and next 12-months long-term debt amortizations). The countries with the lowest ratios are at the highest risk of running out of funding, with those with ratios less than one in particularly precarious positions.

(Click to enlarge)

The U.S. on Safe Ground

On the other side of the coin, many developed markets are expected to continue seeing healthy FDI inflows.

Developed economies account for 72 percent of the spots on the A.T. Kearney FDI Confidence Index, with the United States topping the chart for the fifth year in a row.

The U.S. accounted for the lion’s share of 2017 global FDI inflows at $331 billion. The enduring attractiveness of the giant market is mainly due to its relatively open regulatory environment that makes it ideal for foreign investments.

This trend is expected to continue in the foreseeable future, though increasing protectionism could threaten it.

Other highly ranked countries for foreign investments are Germany, China, United Kingdom, Canada, Japan, France, India, Australia and Singapore--in that order.

By Charles Benavidez for Safehaven.com

More Top Reads From Safehaven.com