In yet another unprecedented COVID historic first, insurance companies are actually turning away Americans who want to purchase a life insurance policy.

Who would have ever thought insurers would turn you away flat out? But the unthinkable is happening, details The Wall Street Journal:

The driving force behind the action: a collapse in interest rates tied to the spread of the new coronavirus and an expectation from insurers that rates won’t rebound significantly anytime soon.

Life insurers earn much of their profit by investing customers’ premiums in bonds until claims come due. In simplest terms, when they price policies, they make assumptions about how much interest income they will earn investing these premiums years into the future. The less they earn, the more they may need to collect in premium or fees to turn a profit.

The report includes stories of Americans being advised to act fast ahead of looming premium hikes.

“In 33 years, I have never seen more changes come more quickly to the life-insurance products we sell,” head of the Akron, Ohio-based ValMark Financial Group said. “It is unprecedented how fast and widespread — it is across lots of carriers.”

Another was quoted as saying: “It is difficult for consumers to have a lot of empathy for the life-insurance companies, but I can imagine they’re really getting squeezed by low rates.”

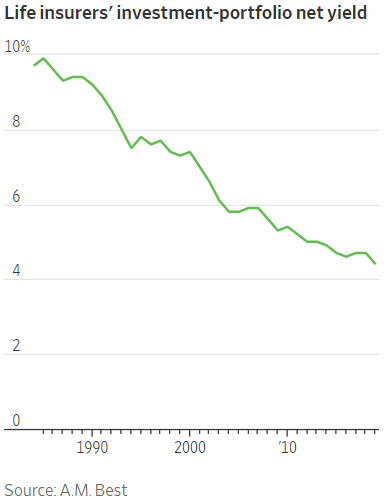

Via WSJ/A.M. Best:

WSJ summarizes:

Typically, life insurers hold about 70% of their general investment account in long-term bonds. In general, the yields on these holdings, many of them corporate securities, follow the 10-year U.S. Treasury. Its annual yield has been mostly declining since the 1980s, when it peaked at nearly 16%.

The yield dove after the 2008-09 financial crisis and was as low as 1.366% in 2016 before rebounding to about 3% in 2018. In March, it plummeted again as coronavirus sparked a rush to safer assets and investors feared interest-rate cuts from the Federal Reserve.

The yield on Friday: 0.679%.

Corporate-bond yields have held up better than the 10-year of late, but the overall trend has been tough on life insurers. Life insurers’ net portfolio yield averaged 4.4% last year, down from 9.9% in the mid-1980s, according to ratings firm A.M. Best Co.

In some cases insurers are reacting directly to the trend of coronavirus' more devastating impact on the elderly:

Penn Mutual Life Insurance Co., among others, has temporarily halted life-insurance sales to people 70 and older and who are in poor health. Insurance-industry executives say that analysis shows older people with underlying medical problems are dying at much higher rates from Covid-19 than younger people.

In a memo to brokers, Penn Mutual said it expects “to revisit these and other changes as we gain better insight into the impact of the Covid-19 pandemic.”

But in other cases even the type of 30-year “term-life” policies most often popular with young families are being temporarily suspended.

More specifically, Prudential halted sales of 30-year “term-life” policies, while Penn Mutual has ceased selling policies to people over 70 and in poor health.

And further, Nationwide Mutual and AIG have capped the size of guaranteed universal-life policies. No doubt this list is set to grow amid the extended COVID-19 crisis uncertainty.

By Zerohedge.com

More Top Reads From Safehaven.com:

{kind=link}

{kind=link}