When Congress enacted the U.S. tax reform at the beginning of the year, they hoped that it would encourage companies to bring back the trillions of dollars they had parked in offshore accounts and help stimulate the local economy. Unfortunately, U.S. companies are in no hurry to bring back those profits home.

New government data shows that companies repatriated only $218 billion net during the first half of the year, or just 5.5 percent of the estimated $4 trillion foreign profits stashed abroad.

An even more worrying trend is that the impact of tax reform on repatriation is rapidly fading. U.S. companies booked a net of $37 billion in overseas corporate earnings during the third quarter, effectively meaning that companies are beginning to bring back home less than they are making in offshore locations.

Source: MarketWatch

The sweeping tax cut legislation aimed to address the punitive taxes that U.S. companies faced whenever they repatriated their foreign profits by offering a lower one-time 15.5 percent tax rate on offshore cash compared to 35 percent previously. But it appears that most companies rather like the idea of having mountains of cash abroad since an earlier analysis by the Wall Street Journal found that two-thirds of repatriated cash during the first half of the year was from just two companies: Cisco Systems and drugmaker Gilead Sciences.

There is no consensus as to why companies are not jumping at this opportunity. The WSJ suggests that a good chunk of offshore funds could be held in illiquid investments making them harder to shift home. The Tax Cuts and Jobs Act (TCJA), however, offers an even more generous eight percent tax rate on non-cash assets thus providing an even bigger incentive to liquidate those assets.

Buybacks Trade Fizzles Out

Corporate apologists asserted that a lower tax rate would encourage companies to bring their offshore funds home, pay taxes and invest in workers and we’d all win.

None other than President Donald Trump had advocated for this portion of the law, predicting that all that cash coming into our country would turn “turn America into a magnet for new jobs.”

Related: Bad News Builds For Global Markets

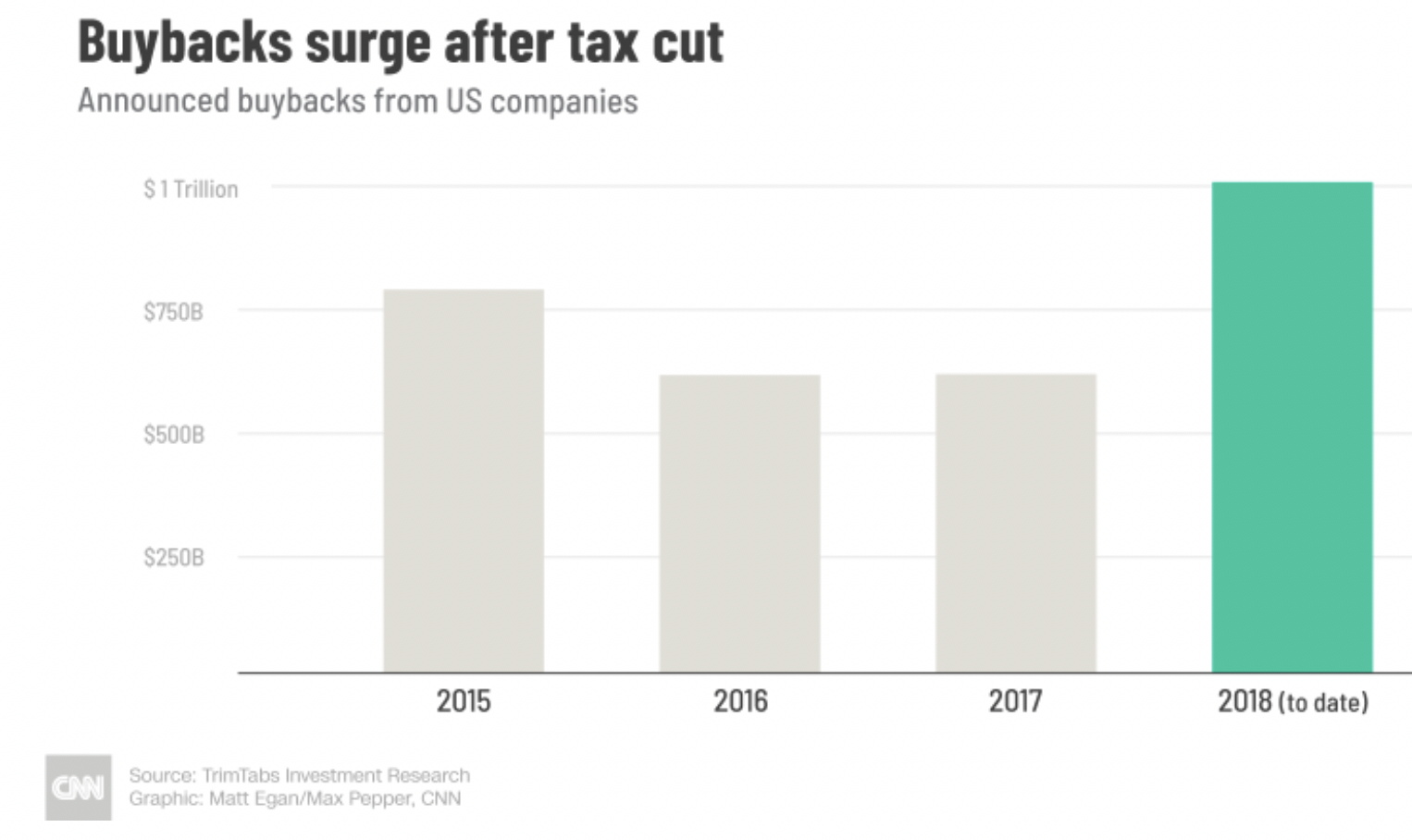

They were wrong. The evidence so far suggests that the vast majority of that cash has gone to fund stock buybacks with little discernible impact on investments. Perhaps it’s no coincidence that the generous tax cuts have coincided with record share repurchases that have hit the $1-trillion mark for the first time in U.S. corporate history.

Source: CNN

Companies usually return their excess cash to shareholders in the form of dividends or share buybacks. They, however, prefer the latter because it also helps to artificially inflate earnings thus making their stocks look cheaper for value oriented buyers. The pressure to report impressive earnings aka quarterly capitalism tends to override most other considerations.

Buybacks trade has continued to support the stocks market this year even when everything else seemed to pull it down. But the moment of reckoning appears to have finally arrived, with companies starting to slam the brakes on buybacks as valuations got out of whack. With no more buybacks to prop the markets, equities are sliding.

Perhaps Congress and Trump should have known better.

Critics of TCJA had argued that another repatriation holiday like the one of 2004 would only serve to provide a major windfall to corporations and enrich shareholders but accomplish little else. Before TCJA, the tax code allowed companies to defer paying taxes on offshore earnings until they actually repatriated them. This provided a huge incentive for companies to hoard their offshore cash indefinitely leading to a situation where Fortune 500 companies owed the taxman nearly $800 billion in unpaid taxes on offshore earnings by mid-2017.

Maybe a better solution would simply have been to end the tax deferral on those earnings and let the hundreds of billions flow into the taxman’s coffers. That way they certainly would have helped tame the ballooning U.S. current account deficit which stood at $124.8 billion at end of Q3 2018 from $101.2 billion in the second quarter.

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com