By some calculations, our consumer debt right now has surpassed what it was in the 2008 financial crisis. If American consumers held $13 trillion in credit cards, car loans, mortgages and other debt in 2008, it will be shocking to learn that they may have topped $14 trillion this year. The $14 trillion calculation comes from Marquette Associates’ senior research analyst of fixed income, Ben Mohr, and it’s spreading like wildfire in the media for the drastic implications. After all, the last financial crisis hit when all those loans went bad, taking down the securities that were pegged to them.

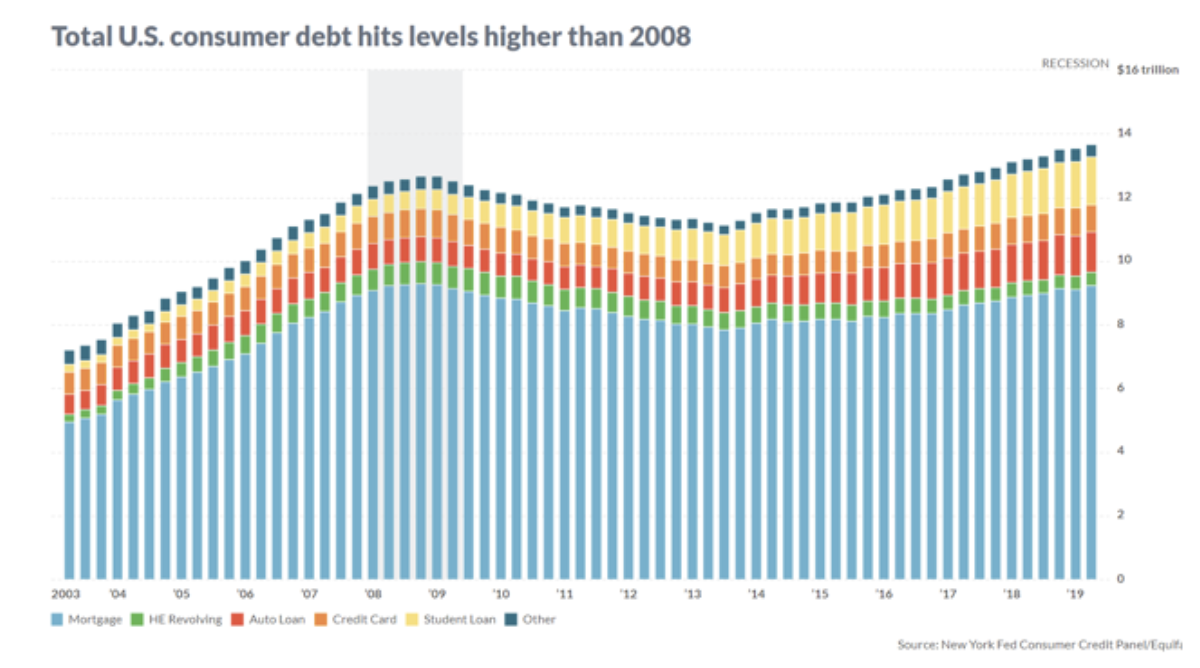

The big picture, in a chart, hits the point home further:

(Click to enlarge)

Source: MarketWatch

It’s not likely to ease up, either.

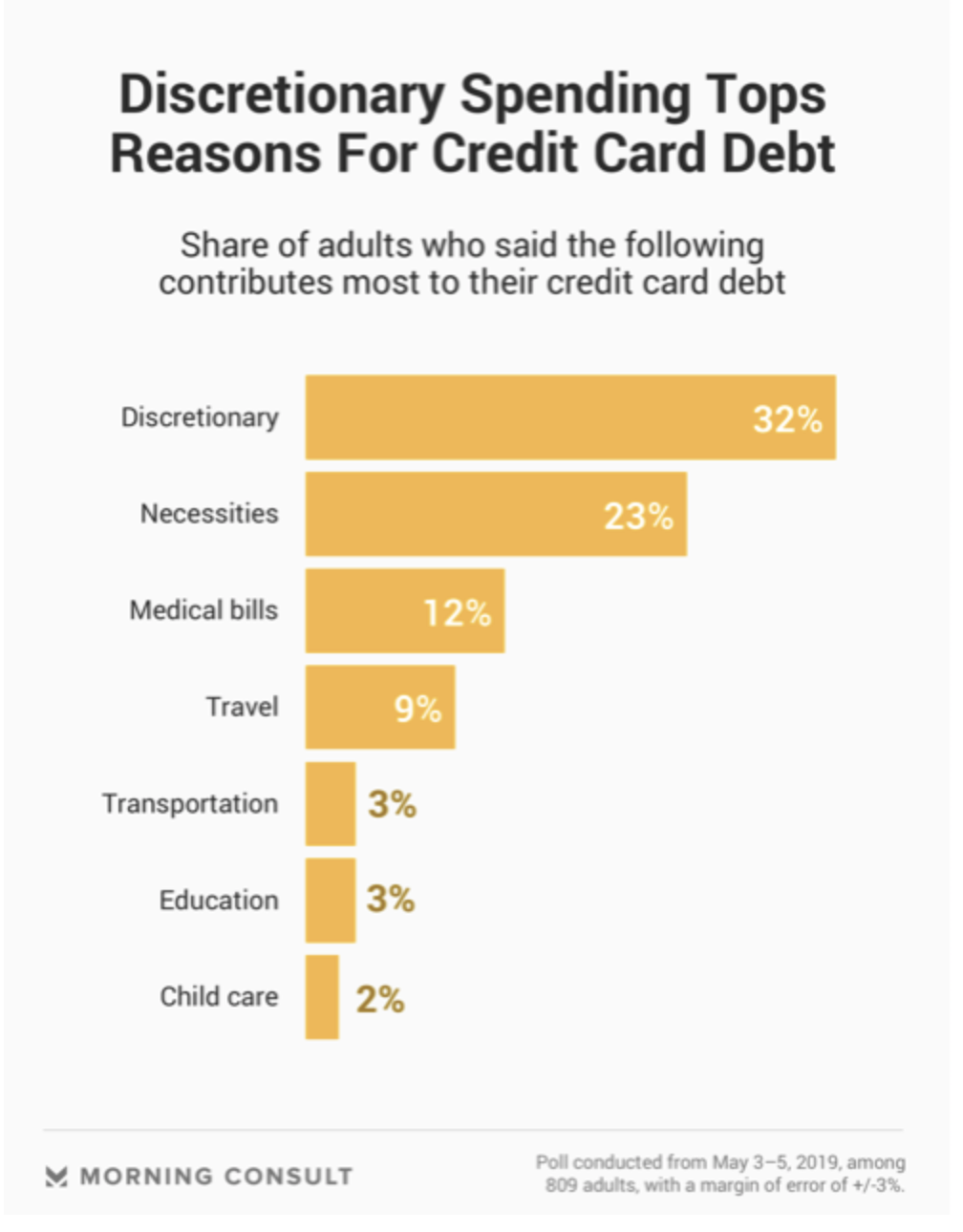

New polling data from a Morning Consult/CNBC survey supports Mohr’s thesis, showing that Americans have indeed taken on more credit card debt than ever before, including during the 2008 financial crisis.

Discretionary spending--spending on clothes, entertainment, etc--is responsible for a large share of that.

(Click to enlarge)

Source: Morning Consult

Credit card balances rose $33 billion in the first quarter of this year, compared to the first quarter of 2018, according to the Federal Reserve Bank of New York.

Credit card debt hit $13.67 trillion in Q1 2019, after seeing household debt rise for 19 straight quarters. And yes, as Bohr notes, that’s higher than the peak in the third quarter of 2008.

Speaking to MarketWatch, Mohr said that soaring student loan debt, which have hit nearly $1.5 trillion, remains a serious concern, pointing out that at the height of the 2008 crisis, student loan debt was far lower, at $611 billion.

Should we be worried. It would seem so, but the research team at Wells Fargo isn’t ready to sound the alarm bells on macro risks just yet. There are two sides to this story.

“Because the financial health of consumers has generally improved meaningfully in recent years, a downturn in the U.S. economy that is caused by financial stress in the household sector does not seem likely, at least not in the foreseeable future,” Wells Fargo notes.

Related: Gold Is In A Precarious Spot

There is, however, a “but” …

“...the rise in auto and student debt could have adverse effects, at least at the margin, on certain individuals and specific areas of consumer spending in coming years.”

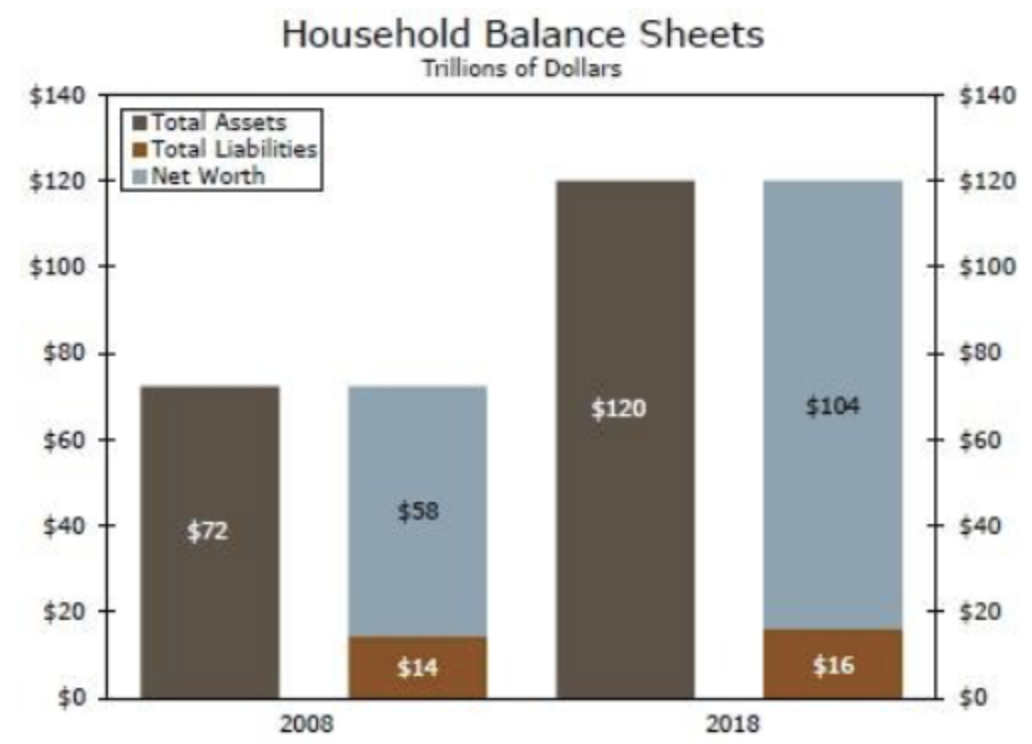

Wells Fargo researchers note that household liabilities have risen by $1.6 trillion on balance since the 2008 financial crisis. But it also notes that the value of household assets have “mushroomed by about $48 trillion” over the same period. That means that households have $104 trillion of net worth right now. In other words, we have more debt, but we’re worth more, too. More precisely, Wells Fargo says that net worth of household assets has increased by some 80 percent since 2008.

(Click to enlarge)

Nor is Wells Fargo particularly concerned about the prospect of the Fed raising interest rates significantly, when it comes to the consumer debt picture and macro implications.

“Even if the Federal Reserve were to raise interest rates significantly, which does not seem likely anytime soon, the debt profile of the household sector implies that the financial obligation ratio would not shoot higher, at least not for the foreseeable future,” the report notes.

By Michael Kern for Safehaven.com

More Top Reads From Safehaven.com: