After buying stocks 'with both hands' on Tuesday, investors went with a distinctly one-handed approach as stock indices ended mixed on even lighter volume. It is far too early to be deeply concerned about the lack of volume, but...it's not too early to be a little concerned. Volume the first two trading days of 2012 is down 25% from the first two trading days of 2011, which itself was the lowest total in at least 5-10 years.

To be sure, there is little new information to warrant a shift of position in the new year if you were happy with your position in the old year. And the indices are still at the top of the ranges of the last five months, so perhaps investors are waiting for resolution before jumping on board. The more sinister interpretation is that Volcker rule restrictions are continuing to erode market makers' ability to provide liquidity, as many of us have warned is a likely consequence of limiting market makers' ability to 'intermediate temporally' by taking a position.

However, I suspect the quiescence is at least partly for the former reason. Website hits for my comment are down as well from the same period a year ago, which suggests fewer people are tuned in so far this year.

Commodities markets have enjoyed the beginning to 2012. Energy markets and industrial metals rallied today. Crude was only up a little, although there was a development that threatens to change the calculus for Iran. In Brussels, EU members agreed in principle on economic sanctions against Iran, crucially including an embargo on importing oil from that nation. If enacted, this significantly changes the balance of risks for Iran associated with closing the Straits of Hormuz. If they are not going to be exporting through the Straits, then there is much less economic cost to Iran to close the Straits. If they aren't selling much oil anyway, then the actual act of closing the Straits carries only military risks - and perhaps not even that, if the regime doubts the determination of the White House. The EU still hasn't put an embargo into place, and it may be implemented 'gradually,' but in my mind the probability of a conflict just went up meaningfully.

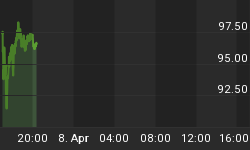

But again, it wasn't just energy markets that rallied. And today, the dollar was stronger rather than weaker. Nominal interest rates rose again (10-year Treasuries now yield 1.99%), but TIPS rallied and inflation swaps increased as well. Moreover, it wasn't just short-term inflation swaps, as would be the case if the market was pricing in a potential oil spike. 10-year inflation swaps are up about 10bps over 2 days to 2.365%. That's still terribly low in the grand scheme of things, as the chart below (Source: Bloomberg) shows. Indeed, Fed officials cannot be blind to the fact that 10-year inflation expectations have only been appreciably lower in the 2008 crisis and in 2010 right before QE2 was 'announced' by Chairman Bernanke.

10y CPI swaps are much lower than average

It is incredible to me that with monetary conditions as accommodative, globally, as they have been in decades, inflation swaps are still nearly as cheap as they have ever been. That's truly striking. What is the 10-year downside to a long inflation position from these levels? One-half percent per annum? Seventy-five basis points per annum? How low can inflation be over the next 10 years, especially with central banks apparently willing (and even anxious) to produce as much liquidity as is needed?

On Thursday, the ADP report (Consensus: 178k from 206k) for December is the keynote release. Initial Claims (Consensus: 375k vs 381k) makes it a rare labor-market double, but Claims for the last week of the year isn't a particularly useful figure and should be ignored. The Non-Manufacturing ISM (Consensus: -46.0 vs -47.5) rounds out the pre-Employment data. Of these, ADP is clearly the most important, but traders will prefer to be conservative in interpretation of any outlier points. This is partly because there is some evidence that ADP suffers seasonal-adjustment problems in December and partly because just last month ADP significantly exceeded estimates and Employment was right on target. In still-thin trading conditions, and only one day to wait to get the 'real' data, traders will prefer to avoid making bets on ADP.

.

I have a favor to ask readers. Would you be so kind as to take a single-question anonymous poll, about your interest and/or willingness to buy certain kinds of "different" inflation-linked bonds? It will take no more than two or three minutes. This is the link to the poll. Thanks in advance!