Happy Halloween to those readers to whom this holiday has relevance.

Happy Halloween to those readers to whom this holiday has relevance.

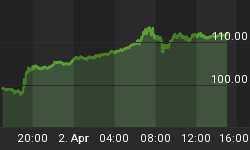

October is ending and is on the verge of debunking the gurus and crystal ball readers (you know who they are) who went on crash-o-matic simply because of the season, or because the Fed has brought the credit markets to a point in the cycle that traditionally signals some bad juju or simply because of that rising wedge (which we kept a close eye on here at Biiwii.com) or a host of other reasons. Here is a news flash; the only thing that happened is the price of world's most visible index frustrated everybody except the "stocks for the long-term" crowd. It frustrated me as well. But one thing I did do in personal accounts and in analysis here was realize that events were going counter to my best laid plans and adjusted, with help from the Dow-Gold Ratio among other indicators. Here is a look at our plump and content Dow, propelled to new (nominal USD) all time highs on the backs of those who doubted it all the way through the hyped Wall St. "witching season" of September and October, which fortuitously represents the entire duration of this letter in its current format.

I wish I could proclaim that all market doubters would have been right but for the the PPT shamelessly flying the markets by remote control, putting the fix in to the crude oil market, waving a magic wand over the bond herd (and their inflation expectations) and couching the coming election in the best possible terms. But I cannot do that. Yes, I do think manipulation of markets exists, and in some cases on a grand scale. After all, what does the Fed do but manipulate "money" rates in an effort to control inflation expectations? Do Bernanke, Paulson, certain Wall Street higher-ups and members of the administration meet, confer and attempt to massage the markets? I would think so. Every time a Fed member makes a speech and his or her words get plastered all over the mainstream financial media, we have attempted manipulation of markets. So what? That is the reality and it is not going to change. Therefore, investors must operate within the given system and try to resist the urge to control the markets in their own minds. This is vital and it is also the basis of the name of our website, but it is what it is. The alternative is to "opt out", which we suggest in the form of eliminating/reducing debt and owning things (hard assets) of value first. Then one may enter the casino where all things paper are traded.

But this being Halloween, I think I will put on an old grey wig and head scarf and look into the crystal ball. What I see there is oil making headlines (this time to the downside), the stock market making headlines (the public will fret about missing the run), consumers in the US and much of the rest of the industrialized world gluttonously moving ever further out on the precipice of debt-for-consumption which is becoming structural. There are contradictory and stagflationary signs in the economy; the housing market is coming down as everybody knows yet commercial real estate booms, certain industrial sectors are hitting soft patches (see recent manufacturing data) yet the machine tool industry ($100,000 to $400,000 machines) has never been hotter, some industrial metals' prices are in correction/consolidation mode while others continue to boom, global geopolitical and local (US) political and social strife is registering at extremes and many many charts appear headed for resolution post-witching season. The chart above is one. Here is a chart of a market that has been eerily and sleepily meandering along, under the radar. The symmetrical triangle is going to break. "Which way?" is still an open question although sentiment in the gold market and much of the commodity universe is anything but frothy and that is bullish. Resistance was hit yesterday, support remains near 575.

You will never find this letter promoting or cheering any asset, even one with no liabilities (in a financial world where debt dwarfs productive surplus) assigned to it. After all, gold proved to be over-valued vs. stocks in 1980. But since 2000, secular changes have taken hold in the precious metals, commodity and stock markets. This is the "big" picture as our often referred to Dow-Gold ratio chart shows stocks continuing in their bear market measured in gold. In the short term, snap-back or corrective limits are being tested. The charts show us that short term trends (out-performance by stocks and bonds) will either revert to their ongoing secular modes or transform themselves into new secular trends. I do not see stocks, from an over-bought extreme with public sentiment and greed dynamics changing and bearish sentiment on the wane, reasserting secular dominance. In USD terms, the "market" can indeed continue higher. It also has untenable risk built in at these levels. We continue to hold a healthy cash position, buying the precious metals and resource sectors on weakness and daily go through the exercise of controlling greed, fear and the tendency to run with convention (herd).

As noted, I have been adding a crude oil proxy in the form of the US Oil fund (USO) and have some copper and uranium positions. These resources largely depend on economic growth or at least the avoidance of economic melt-down, unlike gold, which could actually favor economic contraction (and resulting Central Bank dovishness), contrary to what the mainstream "inflation trade" might preach. Changes are coming. They always do. But they may simply represent a change back to the secular trend in force since 2000. We will simply have to watch, wait and see which way the winds of change blow.

ETF's and stocks relevant to this analysis include DIA, GLD, USO, NEM, GG, PD, SXR.TO