Weekly Trader Alert #89

1/30/2007 9:17:36 AM

Overview

With earnings season in full swing (about one third of S&P-500 companies reported last week), the focus is generally on earnings reports and guidance. At this time, it appears that companies will report, on average, a bit more than 10% growth, year over year. That is about a half percent higher than expected. In recent quarters, companies have exceeded expectations by 3-5%, so from this perspective companies are underperforming, even though growth will still be double digits, for the 14th quarter in a row!

Housing, undeniably the weakest sector in the economy, is showing some signs of improvement. While clearly a drag on the overall economy, home inventories are slowly being worked off and there are signs that housing is recovering. Recall that a week ago, building permits and housing starts both came in higher than expected.

New home sales rose by 4.8% in December, registering a fall of 17.3% on the year with 1.0631 million units sold in 2006, the largest drop in 16 years. Note that to sell these homes, an average of $47K in incentives was included. Also, unit sales are reported at contract signing, so these numbers do not include contracts broken where delivery was not taken by the buyers. Existing home sales fell by the largest amount in 17 years, with 6.48 million units sold for 2006, which is down 8.4% year over year.

With rising interest rates, it appears that home buyers are retreating a bit more, with mortgage activity declining 8.4% for the week ended January 19th.

Leading economic indicators inched higher by 0.3% in December. A Fed favorite metric, this indicates a modestly expanding economy. Durable goods orders rose 3.1% in December, which was weaker than the expected 3.5% rise. For the year, durable goods orders rose 7.0% versus 2005's 8.6% gain.

With crude inventories rising modestly (by 700K barrels) and gasoline inventories also rising, you would think that price would fall. Rather, oil prices rose nearly $3.50 a barrel to $55.42 with natural gas prices rising to $7.175 per MBTU. The unseasonable warm weather has defied expectations and moderated use of fuel allowing oil to fall more than $20 from its peak close of nearly $77 in the summer of '06.

Next Tuesday and Wednesday is another Fed meeting with the dutiful policy statement issued on January 31st that is widely expected to hold rates unchanged. With the latest sentiment expecting no change in interest rates for 2007, this policy statement will be more closely watched than most. As of last week, expectations were for a likely 0.50% rate drop by June. With the economy strengthening, Fed watchers expect no change and even fear a possible rate hike, so will be watching to see if inflation hawks win out in Fed debates over policy.

To understand more about our view on the markets, we will have to look at the charts.

Market Climate

The market is exhibiting signs of wandering. Whether moving higher or lower, volatility is increasing as one day's large move is reversed the next day. We saw a bull trap in the markets as a two day advance on Tuesday and Wednesday was reversed on Thursday.

The mood of investors has clearly grown wary. With investors fretting more over whether the Fed may retain current interest rates for 2007 versus enjoying better than expected earnings, the pendulum appears to have moved to the negative side. Complacency is certainly not the way to describe investor activity as put/call ratios continue at relatively high levels.

Once again, we will remind readers that while the ETFs continue to hang in there, investors are continuing to react more strongly to negative news than positive news. The NASDAQ continues to show signs of distribution. The Dow and S&P-500 only began to show distribution from Thursday. This would have to be confirmed with a continued slide in the coming week to amount to anything.

We believe it is a time to be cautious and to protect profits.

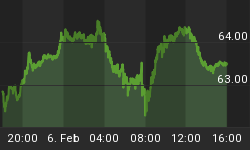

The U.S. stock market composite chart:

Resistance continues to be seen for the U.S. market overall. Friday's doji reflects indecision, but the shallow uptrend hasn't yet failed. The markets appear to be climbing a wall of worry.

Examining both RSI and MACD, both are clearly positive suggesting a continued move higher. Most of the move upward has been powered by a rise in small cap stocks. There is often a pronounced move into higher risk (small cap) issues just prior to a market top.

Fundamental Trends

Only two of the five leaders remain from last week, but the new entries are particularly surprising, as they have either been recent leaders or were mentioned as being in the top screen.

Fertilizers dropped to ninth place and Real Estate Management is just above that. Airlines, however, dropped off the top screen (top 31 industries) altogether as some have reported earnings, and they were somewhat disappointing. There also appears to be less enthusiasm for M&A in the industry than anticipated. Basic Steel is also found in the top screen and has been moving up of late.

Two retail industries (drug stores, and jewelry stores) while four more are in the second screen. There are five building industries (Cement, Wood Products, Tools, Painting Products, and Heavy Construction). There is even another just off the first screen (Misc building products). Residential/Commercial building dropped off quite a bit below that.

Healthcare now has Nursing Homes in the top screen while Outpatient care dropped far into the second screen.

Foreign Banks have remained in the top screen for months. So have telephone utilities and the auto/truck tire industry is actually in sixth place.

The Industry leaders (ranked 1st-5th out of 190) are:

Two new laggards have entered, with the drillers and consumer electronics now sharing cellar dweller status.

The plastics industry has begun its rebound and we are looking to enter a long trade.

The Industry laggards (ranked 186th-190th out of 190) are:

Trade Recommendations

We didn't get our cement industry entry to Texas Industries (NYSE:TXI) as it never reached our buy point. We are looking at several other candidates in the industry, including, EXP, FRK, VMC, MLM, and CX. Of course, TXI is also on the list, but we didn't get the entry we wanted.

We didn't get our entry to Diamond Offshore (NYSE:DO) a week ago, but we may get another chance at a driller if we see a further pull back. Some of the drillers appear to have put in a local top and should continue to pull back. We will monitor this.

We are also looking at long trades in the forest products industry, but there are only three candidates to choose from.

We are also exploring the builders and other areas and will be making trade recommendations as we find them intraweek.

Current Portfolio

We are still in a short trade on the QQQQs. The QQQQs did move lower from a week ago, but are showing signs that this down move is coming to an end. We are looking for an exit for this position this week.

FDG has broken above resistance. If it is able to maintain price above $21.65, it should continue to move higher. It continues to pay out a large quarterly dividend amounting to annual gains of 15-20% of its price.

* Initial stop prices are set to cause us to exit our positions if they close below these levels. You will note they are generally kept pretty tightly the opposite side of the trades we initiate. Historic volatility would imply that intraday price action may trade outside of these values, so that condition is insufficient to cause an exit from an existing position. On significant movement beyond our stop prices, we may issue an intraday message to exit the position or to maintain the position. You may chose to implement an absolute stop below these suggested stop values, but that stop should be wide enough to take care of the daily volatility for the stock in question. You can examine the candlesticks for an idea of intraday price fluctuations.

Entry prices are adjusted to account for dividends paid. The stock price was adjusted by your broker, to reflect the dividend taken out. The non-adjusted entry price reflects the actual entry price, without the adjustment for dividend values.

LVPB Concept: The concept is a Light Volume Pull Back, where a stock's price will pull back to a support level on light volume. Obviously, heavy selling is a sign of weakness, and we would not want to buy on a heavy volume pullback. However, we will occasionally place stocks on the LVPB (Light Volume Pullback List) to indicate a "re-entry" buying opportunity, when we have already entered a position. This should be used to add to existing positions, or to enter a position if you missed the initial entry.

LVPB Portfolio Stocks:

Conclusions

As stated last week, earnings season moves the market. If we continue to see companies taking down forward guidance, we believe a negative mood will persist and the market is vulnerable to a sell-off. With companies beating expectations by a modest average 0.5%, versus recent quarter 3-5% beats, we believe the market is vulnerable to a sell-off.

At this time, we believe that the market is overdue for a correction of some sort, and is more vulnerable to downside action, than it is poised for significant gains. We believe investors should take precautions to protect profits from long positions and should consider shorting the market as conditions warrant.

The problem with our belief, that the market is overdue for a correction, is that it is now a commonly held belief. With the eight month virtually unchecked run-up in stocks, it seems everyone is concerned about a pull back. This sort of run-up hasn't been seen in more than ten years, so investors/traders are nervous. It could turn out to be just the sort of wall of worry that allows stocks to continue to rise. Probably the biggest factors now are how the Fed reacts to a strengthening economy, and how the market reacts to the Fed.

For those of you who have enjoyed your subscriptions to the Fundamental Trader and who would like to get additional savings off the price of your subscription, you may consider an annual subscription to the service. You can save nearly 20% off of the monthly rate by selecting the annual subscription price. Just click on the link below:

http://www.stockbarometer.com/pagesMFT/learnmore.aspx

Regards and Good Trading,