For markets of May 24th

| CLOSES | INDICATIVE LEASE RATES Based upon 30 day maturities | ||

| JUNE GOLD | $384.90 | GOLD | .00/.50% |

| JULY SILVER | $ 5.87 | SILVER | .50/2.00% |

| JULY PLATINUM | $817.10 | PLAT | 3.00/8.00% |

| JUNE PALLADIUM | $249.50 | ||

General Comments:

After the blindingly vicious decline of the precious metals markets over the past month or so, last week saw a welcomed return to some sort of normalcy, with these markets responding to fundamental demand/supply considerations and the movement of the USD rather than the hysteria and dementia fomented by the speculative crowd. The wild-eyed speculative crowd burst into the party, largely uninvited, to propel commodity prices to thoroughly unrealistic price levels only to disgorge their long positions upon just the first signs that the hour was late, and the party was just about ended. It was most exciting watching hundreds of millions of Dollars being whipped around in completely random fashion as wagers were being placed by seemingly deaf, dumb, and blind traders taking what seemed to be ever more foolish bets that the prices of the precious metals could forever defy gravity. It was fun, and most dangerous to trade, while they were at the casino tables, but now we return to markets that are more sensible, more easily predicted and forecast, and much more easily successfully traded.

As the USD declined last week, with the Dollar Index down about 2%, the precious metals, still in a needed convalescence after their drunken orgies of the past month, rose moderately in response. Gold was up almost $8 for the week, silver up some 14 cents, while platinum scurried $23.40 higher in price. Even palladium, still reeling from its recent 33% decline from its highs seen just about 6 weeks ago, managed to rise by $6.70. Please note the closer correlations between the USD and these markets as three of the four precious metals rose by roughly an equivalent amount to the fall in the USD.

In a thoroughly unprecedented move, The CFTC, on their website, answered the angry emails generated by thousands of investors urging this governmental agency to investigate their highly dubious allegations of market manipulation in silver. I STRONGLY urge all those interested to carefully read the response by the CFTC , as the letter is extremely well crafted, displays a most delicate understanding of the basic fundamentals of this market, and takes a deft scalpel to the fanciful and ludicrous claims of those analysts who played the Pied Piper luring thousands of investors to financial losses on the belief that the silver market was going to completely explode due to the demise of some international cartel which has heretofore been conspiring to dampen the silver price. Many months ago, I cautioned investors to completely investigate all such claims as I cautioned that the then current price levels of above $7 were totally unsustainable. Again, those interested in the excoriation of those analysts who were mega-bulls in silver, along with those with more than a passing interest in the markets, should definitely read the article.

Most of the bullish rhetoric in silver has been centered on the claim by several of the leading analysts in the industry that we have experienced a supply/demand deficit for some 15 years running. The bulls take this argument per se, and proclaim that the day of reckoning is soon upon us as diminishing supplies will force silver prices higher. The bears brush away such fundamental considerations trumpeting that above ground inventories are in the billions of ounces, enough to forestall any price rises for decades, if not forever. My opinion is much more plebian, a great deal more pragmatic. I believe that markets are efficient; I contend that it is implausible that a deficit in the supply/demand fundamentals could not have existed for 15 years without a rise in the silver price. Yes, perhaps markets can be inefficient for a day, perhaps a week or a month, but not for a decade and a half. Ergo, there is no deficit. There is a theorem in logic called Occam's razor, which states that the easiest answer is most often correct, and I think it applies here elegantly.

Recently, GFMS's survey reported that a two-year decline in silver fabrication demand ended in 2003, with demand increasing by over 13 million ounces to 859.2 million ounces. Industrial demand came in at 351.2 million, jewelry demand at 276.7, and photographic demand fell slightly to 196.1 million ounces. With mine production at 585.2 million ounces, and scrap recovery at 191.6 million, GFMS sees a supply deficit of 72 million ounces for 2003.

The latest Johnson Matthey report on platinum, expects that platinum supply and demand will be more or less in balance in 2004, ending 5 years of supply deficits (please note that these deficits at least tripled the price of this commodity during this period). World demand for platinum edged up about 1% to 6.52 million ounces, of which about HALF was bought by automobile companies for catalytic converter systems. Global demand for jewelry fell by 13% to 2.44 million ounces as high prices discouraged buyers. This prestigious firm expects jewelry demand to fall again in 2004 and forecasts prices between $780 and $920 per ounce based largely upon the whims and caprices of the speculative crowd.

Its sister palladium enjoys no such favor, as the surplus widened to 1.19 million ounces, as supply totaled 6.45 million ounces while demand improved by 9% to 5.26 million ounces. J-M sees the price at $200-$340 over the next 6 months, and again subject to speculative interests.

The Chicago Board of Trade may be preparing to compete directly with the Nymex for futures business in the precious metals. For many years, The CBOT has had "mini" gold and silver contracts, which hardly interested anyone in the markets. Volumes were pathetically tiny, and the CBOT actually used the closing settlements for the markets in New York as their benchmarks, knowing that their markets were too insignificant to matter. Well, with the recent interest in the metals, and sharply increasing volumes in these "mini" sized contracts (although from extremely low levels), now the Chicago Board of Trade may be considering full size contracts traded electronically in direct competition with the New York markets. While I believe the competition is wonderful, and may force Comex to update their electronic overnight markets, I don't give the CBOT much chance. In fact, let me change that. I give them no chance.

Central Bankers around the world continue to sell gold, declaring that it no longer useful as a reserve. The latest was the announcement by Portugal that they have sold 35 tons, for delivery in May. It would also appear that Lebanon was a seller of perhaps over 10 tons. While the European Central Banks recently re-signed the Washington Accord, agreeing to limit their sales of gold and the use of derivatives for the next 5 years, despite their assertion to the contrary, the signal they are sending is quite clear. They don't believe in gold as a crucial core reserve asset. But the good news is that historically they have been sellers at the bottom and buyers at the top of the market.

On to the Commitment of Trader's reports, as of May 18th, for both futures and options:

GOLD| Long Speculative | Short Speculative | Long Commercial | Short Commercial | Small Long Spec | Small Short Spec |

| 83,503 | 49,247 | 155,077 | 225,300 | 65,969 | 30,002 |

| -3,861 | +5,299 | +3,929 | -6,604 | -126 | +1,246 |

The gold market was fractionally lower during the reporting period as open interest rose moderately. Over the past weeks, spec shorts have entered this market turning the current ratio of speculative longs to shorts to 1.89 to 1, down most dramatically from a high of 7.5 to 1. Notice something interesting? The specs had their biggest position at the recent highs, and now that we have fallen some $50 in value, currently trading in the $370's, NOW they are beginning to get short. The last few months instructs us that OVERALL the specs are wrong, and taking the opposite side, although worrisome to some, usually works.

My general view of the gold market here is that we are still convalescing from the recent painful illness of the past few weeks, and that only time will heal the wounds. I look for further consolidation and range trading between the $373-$375 price level at the lows, and perhaps $385-$388 at the highs. The USD should continue to be the prime driver. Markets like this are much easier to trade with volatilities lessening. Recommendations to follow.

SILVER| Long Speculative | Short Speculative | Long Commercial | Short Commercial | Small Long Spec | Small Short Spec |

| 36,103 | 7,670 | 20,635 | 80,182 | 41,152 | 10,038 |

| +394 | +2,025 | -1,073 | +3,343 | -408 | +231 |

The silver market was up 16 cents during the relevant time frame as open interest was stable. On a net basis, speculators were adding to their short positions as commercials were the buyers. This is relatively bullish; of course, because as short commercials cover their positions, it portrays actual physical demand for the underlying commodity, something that we did not see when silver was over $6.50. While the specs may come and go, at the end of the day silver is a commodity, and actual physical demand is the best "floor" for the price.

While the ratio of speculative longs versus speculative shorts is still quite high at 4 to 1, I would imagine that this market has been totally cleaned out of any weak hands on the long side. Like gold, I look for a technical consolidation, with prices ranging from the low $5.60's to the high $5.90's. I would have no problem being long near the bottom of the range and no difficulty being short at the top. Due to recent markets, option premiums are still very "tasty", and selling out of the money puts looks right. I would also be a seller of covered calls. Call our offices for specific discussion in light of your risk/reward profile.

GOLD RECOMMENDATIONS:

Expected trading range: $374 to $388

As mentioned, I see this market as a trading range, where the movements of the USD will continue to exert the greatest influence. Trade the range, and don't be afraid to either be long at the lows, or slightly short at the highs. Selling out of the money puts at the $370 level seems rather lucrative here, as well as selling covered calls against long futures. I would NOT be seller of naked calls, especially those of longer duration, as gold remains in a primary bull market.

SILVER RECOMMENDATIONS:

Expected trading range: $5.60 to $6.00

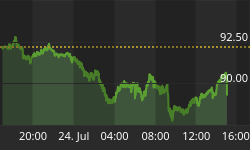

The chart above demonstrates the complete devastation of this market, where 5 months of gains were lost in just 18 trading days. It is only natural and normal that we now rest, that this market attempts to find a bottom. I believe that we have found it, but that any further rallies of any size are perhaps a long time off. Again, look for range trading, with gold and the Dollar moving this market. Option premiums are still enormous, and well capitalized accounts should be aggressive sellers of puts in the $5.00 to $5.25 range. This market is still dangerous, so continue to be careful.

PLATINUM RECOMMENDATIONS:

Expected trading range: $780 to $830

Again, perhaps we have found the lows in the market. Yes, prices did dip into the $760's for a bit, but in retrospect, that was way too cheap. I would be a buyer in the high $790's or low $800's, looking for a "quick flip" should prices get above $820 or so. The short side of this market looks unappealing.