Here is another smattering of news from the weekend past, as well as our take on it and a decent dose of realistic analysis to cast a light on the real issues at hand...

Beijing Reports a Trade Deficit: BusinessWeek

- China reported its first trade deficit in over 70 months as the prices of raw materials imports climbed

- Analysts are stating that a stronger Yuan is needed to deter increasing domestic inflation

- China has the impossible task of balancing an ever increasing asset price bubble with US demands for a revalued Yuan in order to fuel President Obama's manufacturing jobs utopia

- Subscribers should reference

China Macro Discussion 2-4-10 (Global Macro, Trades & Strategy)

China Macro Discussion 2-4-10 (Global Macro, Trades & Strategy)

And speaking of Beijing,,, China's Economic Growth Accelerates to 11.9%, May Prompt End of Yuan Peg - The Overheating has arrived???

- China's economic growth accelerated to the fastest pace in almost three years in the first quarter, highlighting overheating risks that may prompt the government to scrap the yuan's peg to the dollar.

- Growth was more than the median 11.7 percent estimate in a Bloomberg News survey of 24 economists.

- A lower-than-estimated gain in consumer prices complicates a debate in Beijing on when to raise interest rates, cut in 2008 to counter the financial crisis. Australia and India have already moved and Singapore yesterday allowed a one-time revaluation of its currency as the region winds back stimulus policies to limit asset-bubble and inflation risks.

-

Investment contributed 6.9 percentage points to growth, consumption accounted for 6.2 points and net exports deducted 1.2 points, the statistics bureau said today. China may post more trade deficits in the first half after the first shortfall in six years in March, the commerce ministry said today. Urban fixed-asset investment increased 26.4 percent in the first quarter from a year earlier, the statistics bureau said today. Producer prices rose a less-than-estimated 5.9 percent in March, after climbing 5.4 percent in February. While China doesn't yet release quarter-on-quarter figures, Royal Bank of Scotland estimated 14.5 percent economic growth on that basis. The median of seven economists' estimates was 11.2 percent.

- Residential and commercial real-estate prices in 70 cities climbed 11.7 percent in March from a year earlier, the most since data began in 2005. Guangzhou-based Evergrande Real Estate Group Ltd. said sales jumped 175 percent in the first quarter.

Double, Bubble, Toil and Troube! You guys know my opinion on this - Bubblicious, all the way! See:

- Can China Control the "Side-Effects" of its Stimulus-Led Growth? Let's Look at the Facts

- What Are the Odds That China Will Follow 1920's US and 1980's Japan?

- Some Light Shown on My Developing China Thesis

- It Doesn't Take a Genius to Figure Out How This Will End

- Signs of a China Credit and Real Asset Bubble Are Now Unmistakable!

- China's Most Expensive Export: Price Inflation

- He Who Bloweth the Bubble With Wet Lips Should Stand Back Lest Spittle and Saliva Spray Upon Ye Face

This Chanos interview helps bring my perspective into focus: http://www.charlierose.com/view/interview/10960#

Trichet Interviews with Italian Press II Sole 24: ECB

- Some countries will need to accept deflation as a return to normalization

- Trichet is very confident in Greece's "austerity measures", and does not expect a bailout to be necessary

- "Countries seeking EMU membership will have to abide by Maastricht Treaty" (why are Greece, Italy, and Spain at the very least even in the EMU? Maastricht is a piece of paper with no legislative bite, no more, no less)

- Is deflation already here? European Retail Sales Fall Most in Nine Months

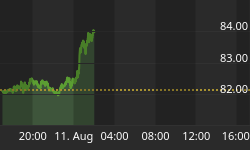

Oil oversupply & under demand: Wall Street Journal

- Oil inventories are at 10 week highs, and gasoline storage is at a 17 year high going into the summer

- Oil has risen to $84, breaking its multi-month $70-$80 range, on increasing anticipation of a US recovery

- With oil reaching the $90 area, unemployment at nearly 10%, and a growing Chinese asset price bubble, Stagflation looms

Consumers Deleverage: Reuters

- Consumer credit unexpectedly took a sharp turn lower, and revolving credit fell at a 13% annual rate

- Consumers are throwing away credit cards, yet retail sales data continues to rise, watch pending homes data on Monday for further development.

- This is an interesting development, for unemployment (real unemployment that is) is still rampant. See Are the Effects of Unemployment About To Shoot Through the Roof?

...The Bureau of Labor Statistics reported the total number of unemployed at 15.6 million and the unemployment rate at 10% in Dec 2010. With serious doubts being raised about the reported figures of the insured unemployed that forms a substantial portion of total unemployed (nearly 69% in Dec 2010, based on reported figures), the total unemployment figures reported by the government is most likely severely understated.

The grave unemployment situation not only undermines the economic health and recovery hopes, but is also acting as a major source of financial strain on the Fed's books. The Fed has been spending huge amounts of money in the form of UI (unemployment insurance) benefits. In 2009, the government paid about $139 billion in UI benefits. Based on the figures for total unemployed by Bureau of Labor statistics and total insured unemployed by DOL, the total insured unemployed which are being supported by the government under the various state and federal programs have risen to 69.0% of the total unemployed as of Dec 2009 from just 29.0% in Sep 2007. Further it is observed that the Fed has been taking in huge deficits on its books because of UI programs. The total UI withdrawals on Fed books in 2009 were $139 billion against deposits of just $31 billion received from states for unemployment. While the withdrawals in 2009 have increased by 320% when compared with withdrawals in 2007, the deposits have declined by 6.6%. The deficit has increased to nearly $107 billion from nearly no deficit, two years ago.

The increased pressure on the Fed books can be largely explained when we look into UI programs that are currently being administered by the government. There are two major UI programs - Regular state programs and Emergency Unemployment Compensation (EUC). While the former has to be funded through tax collection by the state (with any deficit financed by the Fed through loans), the latter is 100% funded by the Fed. EUC is a Federal, temporary extension of unemployment compensation for unemployed individuals who have already collected all regular state benefits for which they were eligible. The program was started in June 2008 and was due to expire in December, 2009. The claims under the program have risen at a phenomenal rate and now accounts for nearly 50% of the total insured unemployed claims. Thus, the Fed has been financing the extension of UI benefits of those which are no longer covered under the regular state programs. As per the last reported figures as of Dec 19, 2009, while the claims under the regular state programs have come down due to the expiration of claims, the same was more than offset by the massive jump in insured unemployed under the federal EUC program. The claims under the regular state programs were down 4.3% (y-o-y) while the claims under EUC were up nearly 200% which led to a nearly 51% increase in total insured unemployed. Insured unemployed are not able to get jobs and with claims expiring under the regular state programs, they are increasingly applying to the Federal's EUC program for extended benefits.

Looking at the initial job claims under the regular state programs, while the markets rejoiced the decline in seasonally adjusted figure, the non-seasonally adjusted figures (which are the actual claims) continue to inch up. For the week ended Jan 02, 2010, the initial jobless claims (NSA) increased 88,000 (w-o-w) to reach 645,571. Looking at the two year trend of the seasonal adjustment does call into question the validity and accuracy of the adjustments, no?

With the total number of insured unemployed (under the state and federal programs combined) continuing to increase as well as no respite coming from the initial jobless claims (looking at the real figures which are not seasonally adjusted), the unemployment situation is far from improving. Further, with serious questions being raised about the validity of the reported number of insured unemployed, the gravity of the situation is definitely underrated. The Fed is pumping in enormous sums of money to underpin the problem - an amount that may rival the TARP. However, with claims expiring under the regular UI state programs and the temporary aid provided by EUC expected to taper in the coming months, unemployment is going to increasingly weigh on aggregate demand and further delay the economic recovery.