If you feel as if this comment has become a little less regular over recent days, it is because it has. Partly, that is because business has been increasingly busy. Institutions are increasingly interested in exploring inflation-related exposures that they may have and developing ways (process-related or investment-related) to mitigate those risks. Investment managers who don't currently have a product offering are interested in developing something or potentially subcontracting out the product management. And individuals of course are always trolling for strategies that provide inflation protection, offer a superior rate of return, are highly liquid, and can be implemented easily and inexpensively. In other words, business is improving for inflation experts, and today's upward surprise in the Eurozone CPI estimate doesn't hurt either. That's good news (well, for me).

But that isn't the only reason the comment has become more sporadic. I freely admit to being somewhat befuddled by the market's behavior. Yes, of course markets can deviate for long periods of time from fair value or rational behavior. In those times, a disciplined approach is incredibly difficult but will produce the best long-term results. Well, my discipline hasn't changed much in the last fifteen years, which is why I have been underweight equities - and at times, completely out - since the end of 1998. There is always the chance that the market has passed me by, and that the "new ordinary" multiples are sustainable. If that is the case, I will miss the run-up of the S&P from 1300 to 10,000 in the same way I have largely missed the run-up from 10,500 or so (I still hold some defensive stocks, but am only about 15% in equities overall).

Missing run-ups doesn't bother me very much at all. I have great confidence in the discipline that has produced excellent long-run returns. It really is the character of the run-up that is disturbing. Since the local bottom on March 16th, the S&P has rallied in 10 of 13 sessions. The 10y note contract fell for nine consecutive sessions from March 16th through March 29th, and 11 of 13 overall. Those are remarkable numbers especially when you consider that really, nothing has changed except the regime in Portugal. The economic data hasn't been getting rosier; in fact, it has been surprising less on the upside than it had been (see Chart below).

The Citi Economic Surprise index. Lower numbers mean fewer upside and more downside surprises.

This rally in stocks/selloff in bonds has occurred on decreasing volume (quarter-end aside), with today's session the slowest of the year on the NYSE, which should be a concern but so far hasn't been. To me it feels more like investors who know they shouldn't be buying, but are 'throwing in the towel,' but that might be just my ego trying to make me feel better. But the optimists (some might say the Pollyannas) are winning. By the way, good for them if they can also turn the economic tables - pushing the market higher doesn't really change anything except the price I have to pay.

I look askance at several things that should be worrying us more. The continuing debacle in Japan seems to have temporarily receded to the back pages, but that may change once post-earthquake economic data begins to be released. Last month, predictably, vehicle sales plunged some -37% year-on-year, the worst performance ever. Machine Tool Orders are due out tonight. We still have another week or two before numbers such as Bankruptcies and the "Economy Watchers Survey" (April 8), Bank Lending (April 11), Consumer Confidence (April 19), Trade figures (April 24) and the Employment report (April 27) are released. I'm not a Japanese scholar so I can't tell you which of these are market-moving data, but I can tell you that until now we have seen almost no post-earthquake data. The economic news is likely to be pretty grim, and I wonder if it will make investors sit up and take notice. Probably not.

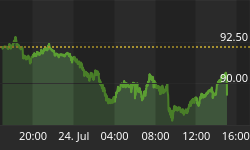

Energy prices are not following the usual pattern we see in markets after a spike. Since front Crude rallied to and surpassed the $100/bbl mark in late February, the market hasn't ebbed. Instead, it is crawling slowly higher ($108 today). See the Chart below. I can't tell you what this means on a daily chart, but I can tell you that when the bond market spikes intraday on a payrolls day, it usually settles and trades sideways and often gives back some of the gain. However, on occasion it 'extends the range' later in the day, and when you see that - and it looks much like this daily chart - it is a clear buying signal because you often get a melt-up from the folks who had sold into the first spike. Again, I'm not sure if this translates to the dailies.

Front Crude is not fading from the spike, but extending therange higher.

Already, slow wage growth combined with quickening price increases on non-discretionary food and energy purchases is pressuring discretionary spending. There is enough good news right now that consumers seem to be opening up a little more, but this isn't a trend that is sustainable long-term.

So how do you write a daily comment if none of the daily occurrences seem to have anything except long-term consequences? Let me assure you, it is a struggle. All I can say is "trust me, it will matter. But probably not today," and that's not particularly helpful to the typical fast-twitch investor. To them, I apologize.

But for those readers who are striving like me to be disciplined investors, we must remember that paths which seem easy are probably false, and that investment success isn't a place but a process. "Before enlightenment, chop wood and carry water. After enlightenment, chop wood and carry water."

.

Tomorrow, while the non-manufacturing ISM (Consensus: 59.5 from 59.7) is released at 10ET, the important item is the 2:00ET release of the FOMC minutes from the March meeting. Be very careful of the headlines, which will almost certainly be taken out of context. There is no doubt that the FOMC discussed the improving data, and no doubt that they considered whether to stop the QE program early. The early headlines will be taken from these sensational points, but it is the context that matters. Frankly, I am more interested in the reasoning given to the really bad decision to let Bernanke hold a press conference after four FOMC meetings per year. As long as it is "to enhance the overall goal of making communications more transparent," then it is misguided but shouldn't have any direct market implications. But beware if there is anything suggesting that the bully pulpit is specifically considered to be useful for guiding the market to recognize policy changes and to understand the Fed's exit strategy as it develops. I don't think they are seriously considering an exit strategy, but rather trying to convince the market that they are doing so...but if the market gets a whiff from the official communications, rather than from one-off cowboy comments by the likes of Kocherlakota and Hoenig, that the Fed is thinking about how quickly they can drain the bathtub, then both stocks and bonds are likely to get hurt.

Fed buying or not, I am getting increasingly bearish on fixed-income although bonds are still in a holding pattern for now. I'd start to get more actively bearish if 10-year yields rise above 3.60%.