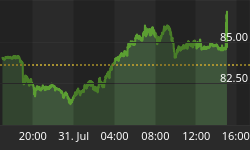

Since its last major low in 1998 at $ 12 (when the Economist published a very bearish piece about oil), crude oil prices have climbed to around $50 at present. The question, therefore, arises whether oil prices are headed for a sharp fall, as most analysts seem to think, or whether far higher prices could become reality in the years to come (see figure 1).

Over the last two years we have repeatedly explained how rising demand for oil in Asia would likely lead to higher prices - this especially because we took the view that the oil producing countries in the world were unlikely to be in a position to increase their production meaningfully. At $50, one might, however, be tempted to think that oil prices are substantially over-bought - certainly from a near term perspective - and ready to decline again. Therefore, I have noted that numerous market participants have been shorting oil futures in the hope of a sharp fall.

I do agree that near term oil prices might succumb to some profit taking. Bullish consensus runs above 80% and oil has become a popular topic of discussion in the media and at every investment conference I attend. Moreover, the US administration could decide to sell oil from its strategic reserve, which currently exceeds 630 million barrels. Thus to sell daily 2 million barrels into the market amounting in total to 120 million barrels over a two months period would be an option if prices continued to soar. Also, since Chinese oil imports were up so far in 2004 by more than 40%, I suspect that some inventory accumulation also occurred in the Middle Kingdom. Therefore, if the Chinese suddenly decided to curtail their oil imports the same way they stopped buying soybeans in March 2004 - an event which led to an almost 50% decline in prices - prices could come under some near term violent pressure! Still, I maintain the view that we may see sometime in future far higher prices than anybody envisions.

Figure 1: Crude Oil Future (Daily Chart)

Source: Credit Suisse Private Banking

First of all, if we look at oil prices in real terms - that is oil prices adjusted for inflation - the real prices is right now still about 50% lower than it was at its January 1980 peak (see figure 2). In fact, oil is now not much higher than it was in the early 1970s, when the last big oil bull market got underway.

Figure 2

Source: Gavekal Research

But, what is important to understand is that whereas the 1970 oil price increases were coming from a supply shock, which was driven by OPEC cutting its production all the while large production excess capacities existed, the current oil bull market is purely a function of increased demand coming principally from Asia at a time global oil production has practically no spare capacity which could lead to much higher production than the current 80 million barrels per day. So, whereas we can say that the 1970s oil shock was "event driven", today's oil price increase is structural in nature. Specifically the current demand driven oil bull market is fueled by the incremental demand coming from the industrialization of China and the rising standards of living around Asia, which increase the population of energy using consumer durables such as motorcycles, air-conditioners, and cars very rapidly. Just consider that China's car population has more than doubled since 2002 and that it is up tenfold since 1994! Thus, as mentioned above, oil imports of China have risen by 40% so far in 2004. And while I certainly do not believe that Chinese oil imports will rise every year by 40%, it is equally unlikely that oil imports into China will ever decline again meaningfully. In fact, if we look at what happened to per capita oil consumption during phases of industrialization in the US between 1900 and 1970, we see that per capita consumption rose from one barrel per year to around 28 barrels. In the case of Japan's industrialization between 1950 and 1970 and South-Korea's between 1965 and 1990, per capita oil consumption rose from one barrel to 17 barrels (see figure 3).

Figure 3: Oil demand in Phases of Industrialization

Source: Barry Bannister, Legg Mason

In the case of China, oil demand per capita is still only 1.7 barrels per year, and for India it has only reached 0.7 barrels. By comparison Mexico consumes annually about 7 barrels of oil per capita and the entire Latin American continent around 4.5 barrels. Therefore, starting from such a low base, oil consumption in Asia will, in my opinion, double in the next ten to 15 years from currently 20 million barrels per day to around 40 million barrels per day (see figure 4). Remember also, that if China's per capita oil consumption went to the level of Mexico's per capita consumption China would consume 24 million barrels of oil daily, which would be close to 30% of global production. And since it is most unlikely that current total global oil production of 80 million barrels per day can be increased much - in fact, it may begin to decline because no major oil field has been discovered since 1965 - I expect that prices will increase further in future - possibly far more than anyone is now expecting. I would, therefore, be very careful when shorting oil and would rather use any weakness, as a buying opportunity.

Figure 4: Crude Oil Demand in Asia

Lastly, I do concede that if oil prices tumbled to say USD $ 40 or possibly even $ 35, equities around the world might well rally temporary (in fact equities would rally in anticipation of such a decline). However, if I am right that in future oil prices could rise much further than is generally expected, geopolitical tension would likely increase dramatically, as countries such as the US and China would increasingly become concerned about adequate supplies. And, in the case that oil prices were to rise in real terms to their 1980s highs - well over US$ 100 (see figure 2) - then the foundation for World War Three would be laid and most certainly begin to weight heavily on equity prices for which I cannot share the prevailing widespread optimism anyway. Financial stocks have begun to weaken and this is an indication that something is not quite right!