Chicago Federal Reserve Bank President Charles Evans was interviewed on CNBC on Monday, and he indicated that he was in favor of continuing asset purchases at a rate of $85 billion per month all the way through 2013. If approved by the rest of the Fed, this would have the effect of about doubling the size of "QE3", or Quantitative Easing Three, the massive Federal Reserve monetary creation and market intervention program announced only three weeks ago.

QE3 combines mortgage security purchases of $40 billion per month until the labor market substantially improves, while continuing "Operation Twist", with the Federal Reserve switching another $45 billion a month out of short term Treasuries and into long term Treasury bonds through December. There is a total of $85 billion per month in asset purchases, of which $40 billion a month is to be financed by creating new money out of thin air. Importantly, the amount of market interventions is scheduled to drop in half at the end of 2012.

If the Federal Reserve follows through with what Evans proposes, it will mean that the pace of $85 billion a month won't slow, and that an additional $540 billion will be created out of thin air over the course of 2013, which will likely be directly injected into the economy without "sterilization". In other words, what Evans is proposing is that the government create and spend a little more than $5,500 per above-poverty-line household to manipulate the markets and to hold down pension and retirement investment returns.

Not too long ago, this would have been the most aggressive and irresponsible action in the history of the Federal Reserve. But at this stage with QE1, QE2, QE3, Twist 1, Twist 2, along with assorted trillions of dollars in loans and purchases with unnamed parties under secret terms, a mere proposal by a (currently) non-voting member of the Fed's policy-making Open Market Committee (FOMC) to increase the size of an already staggering program to an even more staggering amount might not seem like that big of deal to the small slice of the public that pays attention to this sort of thing.

So why did Charlie Evans do it? And why did Ben Bernanke likely authorize the nationally televised interview?

Let me suggest that it is only when we answer those questions that we can find out what the Fed is really up to - which is playing a quite different game than what is being put out in the press releases.

Implausible Explanations - Conventional

We'll start with the conventional perspective. The Federal Reserve and Ben Bernanke are already taking a great deal of heat over the recently announced massive and open-ended QE3 program. There is loud and public skepticism about whether QE3 will actually make any difference to the economy, given that both QE1 & QE2 failed in their stated goals of restarting the economy and housing market.

Given the size of QE3, even members of the Federal Reserve are starting to publicly express concern over the danger of causing increased rates of inflation, as shown by the recent comments from Richmond Federal Reserve Bank President Jeffrey Lacker in explaining his dissenting vote on QE3.

There is a presidential election next month, and Bernanke is already taking a great deal of heat for QE3. Why toss gasoline on the fire and have a non-voting board member talk about doubling down on the size of QE3? After all, there is no money being created and no solutions are actually implemented - there is just the risk of political damage for seemingly no benefit at all.

Why did a non-voting Fed member go on national TV to talk about his desire to increase the size of QE3 months down the road? Why risk the pain for no gain?

Implausible Explanations - Contrarian

If the conventional doesn't make sense, then maybe it is the usual contrarian perspective that will hold the answers. OK then, let's assume that what many are writing about is true, which is that the United States dollar is right on the brink of collapse, with destruction likely to occur in the fall of 2012, even as the Federal Reserve desperately tries to hold on.

Now, from that viewpoint, the Federal Reserve and the US dollar are on the verge of imminent annihilation because of the massive creation of fiat currency that is about to lead to a complete collapse in confidence. Viewed from that perspective, what Charles Evens just proposed was insanely stupid - as he just accelerated the loss of confidence and resulting destruction of the dollar for no gain whatsoever. There is no money being created and spent - he's merely talking about why he wants to do so.

Why would he do that? Why did Ben let him?

Again: why would a non-voting Fed member go on national TV to talk about his desire to increase the size of QE3 months down the road?

An Explanation That Is A Perfect Fit

The problem with both the conventional and contrarian perspectives is that Evans went on TV to talk some radical talk that risked bringing down the value of the dollar, but without being in any position to actually do anything about it for some time to come.

If there is a logical explanation to be found then, we should seek outcomes in which it is desirable for Bernanke to use a credible and substantive proxy to talk trash about the dollar and bring it down in value, without actually taking the accompanying concrete actions to go along with it. If he had such an objective, Bernanke would want to deploy someone important enough to command the full attention of the global professionals who watch the Federal Reserve - but at the same time be sufficiently obscure that the average US citizen or reporter would have never heard of him or her, making the proxy far less risky than Bernanke himself making the comments.

Consider the explanation below, published in my article: "'Unlimited QE3' Quick Analysis: Federal Reserve Attacks US Dollar, Risks Currency Warfare" (linked below):

http://danielamerman.com/articles/2012/QE3C.html

The Federal Reserve is indeed using QE3 to attack the problem of unemployment - but not through the method stated.

The cover story is that QE3 will be used to increase the money available for lending and to lower interest rates. It is a credit to Mr. Bernanke that he was able to read this statement with a straight face, for the assertion that the economy is being held down by too high of interest rates and tight money is ludicrous. Interest rates are already at historic lows, and banks are awash in available cash. Moreover, QE3 is likely to have very little effect when it comes to expanding corporate lending, just as QE2 had very little effect - because that was never the intended route to rebooting employment in the United States.

As described in detail in my article "Bullets In The Back: How Boomers & Retirees Will Become Bailout, Stimulus & Currency War Casualties" (linked below) the United States has a structural problem with unemployment that is essentially unsolvable so long as the dollar remains high in value relative to other global currencies.

This problem was exacerbated by the rise in the US dollar caused by the Euro crisis - and it is no coincidence that the unemployment crisis in the United States is now getting rapidly worse even as the dollar soared this past spring and summer.

http://danielamerman.com/articles/Bullets.htm

The Federal Reserve is, of course, well aware that the unemployment situation is far, far worse than what is being captured in the official headline unemployment rate of 8.1%. The government knows full well that the true unemployment rate, once workforce participation rate manipulations are netted out, is closer to 19% - and getting worse, as explored in detail in my article linked below, "Making 9 Million Jobless "Vanish": How The Government Manipulates Unemployment Statistics".

http://danielamerman.com/articles/2012/WorkC.html

This building crisis of a strengthening dollar and rising unemployment called for emergency action, and that is exactly what Bernanke is doing. He is effectively calling in a B-52 strike on the US dollar, monetizing for the world to see, and pledging to monetize for as long as it takes - until the US dollar is driven down to a level where American workers can once again be globally competitive.

If the rest of the world sits back and lets the United States drive down the value of the dollar, then US employment is indeed likely to rise - at the cost of falling employment elsewhere. But if the rest of the world is not willing to sit back and watch jobs flow to the US, then there is likelihood of counterstrikes, and even the danger of all-out currency warfare.

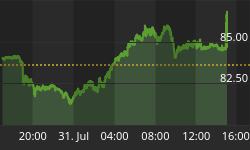

Now, let's look at the situation at the start of this week. The building anticipation and then finally the announcement of QE3 had been successful, having driven the dollar from a summer high of 1.206 dollars per Euro down to 1.31 dollars per Euro by mid-September. Then Spain starts to go south, the Euro looks like it is in trouble again, and the dollar starts rising again. The situation gets markedly worse in Spain over the weekend, and the dollar looks poised to rise again. Which, if allowed to happen, would make US workers that much less competitive around the world, and lead to job losses instead of job gains.

Until, that is, a non-voting member of the Federal Reserve Open Market Committee goes on national TV to talk about his desire to see the size of QE3 more than doubled in another few months.

And it looks like it has worked, as the dollar moved from a high of 1.280 dollars per euro on Monday, down to a price of 1.292 dollars per euro on Tuesday afternoon. Now, this may be fleeting if the Spanish situation continues to deteriorate. But nonetheless, the only price for the dollar moving the opposite way that a reserve currency should move during crisis, was a senior Fed official doing a little trash talk about the dollar on TV in a way that his own nation barely noticed - but the rest of the world did.

Suddenly, everything adds up perfectly. The "pain" is the gain, it is the objective and not the undesirable by-product. Whether what Evans proposes ever happens or not in 2013 is almost incidental during the first week of October 2012. What matters is that there is bad news out of Spain and a pre-emptive attempt at changing the psychology of the market must be made, before there is a repeat of the damage that occurred in the spring and summer as a result of the US dollar being the globe's reserve currency.

The point at which things go from not adding up at all to adding up perfectly is a good place for considering a paradigm shift, and then evaluating whether the Fed's real strategy is one of attempting to increase employment by waging undeclared currency warfare - with the myriad financial implications that follow.